|

市場調查報告書

商品編碼

1721427

獸醫骨移植和替代品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Veterinary Bone Grafts and Substitutes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

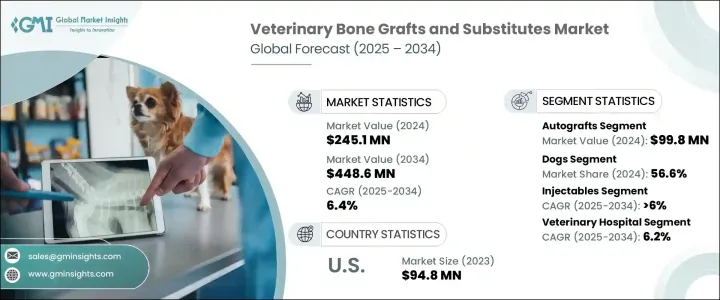

2024 年全球獸醫骨移植和替代品市場價值為 2.451 億美元,預計到 2034 年將以 6.4% 的複合年成長率成長至 4.486 億美元。業內專家表示,隨著全球寵物擁有量的增加以及對先進獸醫骨科治療的需求持續成長,市場正在穩步發展。伴侶動物和農場動物意外傷害、關節疾病和與年齡相關的骨骼問題的增加極大地導致了骨科干預的激增。專業人士指出,再生獸醫學的廣泛轉變為動物傷害的治療方式帶來了顯著的轉變。

獸醫擴大利用創新的移植技術,包括同種異體移植、異種移植和合成替代品,以確保更快的癒合和改善術後效果。人們對磷酸鈣和羥基磷灰石陶瓷等生物相容性材料的偏好迅速成長,獸醫認為它們能夠模仿天然骨骼結構、促進有機再生,同時減少術後併發症。分析師也強調,隨著對先進獸醫護理認知的不斷擴大,寵物主人和臨床醫生都傾向於提供更好的預後和恢復時間表的解決方案,從而推動了對下一代骨移植技術的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.451億美元 |

| 預測值 | 4.486億美元 |

| 複合年成長率 | 6.4% |

根據產品類型,專家確認自體移植領域在 2024 年創造了 9,980 萬美元的收入。獸醫將這種方法(移植物來自同一動物)描述為黃金標準,因為它具有卓越的整合能力。他們解釋說,自體移植透過支持成骨、骨誘導和骨傳導提供三重治療效果。由於這些特性,專業人士普遍傾向於在動物的牙科和骨科手術中使用自體移植,特別是在長期穩定性和生物相容性至關重要的情況下。

根據動物類型,分析師報告稱,到 2024 年,狗將佔據 56.6% 的主導市場。他們將這一優勢歸因於犬類陪伴日益成長的文化趨勢以及寵物醫療保健支出的持續成長。獸醫觀察到,骨骼損傷、骨折和退化性關節疾病在狗中特別常見,這導致移植手術的頻率更高。產業專家強調,越來越多的狗主人選擇複雜的外科手術治療,進一步推動了骨移植和骨替代品的採用。

2023年,美國獸醫骨移植和替代品市場規模達9,480萬美元。專業人士認為,這一成長得益於美國先進的獸醫醫療基礎設施和較高的寵物擁有率。手術中骨移植的常規使用以及完善的移植材料分銷網路的存在,幫助美國成為全球範圍內的主要收入來源。

全球獸醫骨移植和替代品市場的主要參與者包括 Lynch Biologics、Veteregen、Nutramax Laboratories Veterinary Sciences、TheraVet、BioChange、Movora (Vimian Group AB)、S-VETOSS、Rita Leibinger、Biomimetic Solutions、Wishbone、Biomendex。產業分析師觀察到,領先的公司正在透過建立策略性分銷聯盟、擴大產品供應以及大力投資再生獸醫研究來增強其市場佔有率。許多引進的先進骨移植材料可改善癒合動力和生物相容性。一些參與者專注於利基獸醫應用,而其他參與者則擴大其地理覆蓋範圍以進入新興市場。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 寵物擁有量和支出增加

- 動物骨科疾病盛行率不斷上升

- 獸醫再生醫學的進展

- 寵物保險覆蓋範圍不斷擴大

- 產業陷阱與挑戰

- 骨移植和骨替代品成本高昂

- 成長動力

- 成長潛力分析

- 監管格局

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 自體移植

- 同種異體移植

- 異種移植

- 其他產品類型

第6章:市場估計與預測:按動物,2021 - 2034 年

- 主要趨勢

- 狗

- 貓

- 馬匹

- 其他動物

第7章:市場估計與預測:依形式,2021 - 2034

- 主要趨勢

- 粉末

- 油灰

- 顆粒

- 注射劑

- 其他形式

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 骨科

- 牙科

- 其他應用

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 獸醫院

- 獸醫診所

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Biomendex

- BioChange

- Biomimetic Solutions

- Cavix

- Exabone

- Lynch Biologics

- Movora (Vimian Group AB)

- Nutramax Laboratories Veterinary Sciences

- Rita Leibinger

- S-VETOSS

- TheraVet

- Veteregen

- Wishbone

The Global Veterinary Bone Grafts and Substitutes Market was valued at USD 245.1 million in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 448.6 million by 2034. Industry experts stated that the market is witnessing steady traction as pet ownership rises globally and the demand for advanced veterinary orthopedic treatments continues to grow. The rise in accidental injuries, joint disorders, and age-related skeletal issues among companion and farm animals has significantly contributed to the surge in orthopedic interventions. Professionals noted that the widespread shift toward regenerative veterinary medicine has brought a notable transformation to how animal injuries are treated.

Veterinary practitioners are increasingly leveraging innovative grafting techniques, including allografts, xenografts, and synthetic substitutes, to ensure faster healing and improved post-operative outcomes. The preference for biocompatible materials such as calcium phosphate and hydroxyapatite ceramics has grown rapidly, with veterinarians citing their ability to mimic natural bone structure and promote organic regeneration while reducing post-surgical complications. Analysts also highlighted that as awareness of advanced veterinary care expands, both pet owners and clinicians are leaning toward solutions that offer better prognosis and recovery timelines, fueling the demand for next-gen bone graft technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $245.1 Million |

| Forecast Value | $448.6 Million |

| CAGR | 6.4% |

Based on product types, experts confirmed that the autografts segment generated USD 99.8 million in 2024. Veterinary surgeons described this method-where the graft is sourced from the same animal-as the gold standard due to its superior integration capabilities. They explained that autografts offer a triple therapeutic effect by supporting osteogenesis, osteoinduction, and osteoconduction. Because of these attributes, professionals widely prefer autografts for both dental and orthopedic procedures in animals, particularly where long-term stability and biological compatibility are paramount.

By animal type, analysts reported that dogs accounted for a dominant 56.6% market share in 2024. They linked this stronghold to the growing cultural trend of canine companionship and the consistent rise in pet healthcare spending. Veterinarians observed that bone injuries, fractures, and degenerative joint diseases are particularly prevalent in dogs, which has led to a higher frequency of grafting procedures. Industry specialists emphasized that dog owners are increasingly opting for sophisticated surgical treatments, further boosting the adoption of bone grafts and substitutes.

The United States Veterinary Bone Grafts and Substitutes Market reached USD 94.8 million in 2023. According to professionals, this growth is underpinned by the country's advanced veterinary healthcare infrastructure and high rates of pet ownership. Routine use of bone grafting in surgeries and the presence of a well-established distribution network for graft materials have helped maintain the US as a key revenue generator within the global landscape.

Key players in the Global Veterinary Bone Grafts and Substitutes Market include Lynch Biologics, Veteregen, Nutramax Laboratories Veterinary Sciences, TheraVet, BioChange, Movora (Vimian Group AB), S-VETOSS, Rita Leibinger, Biomimetic Solutions, Wishbone, Biomendex, Exabone, and Cavix. Industry analysts observed that leading companies are enhancing their market presence by forging strategic distribution alliances, broadening their product offerings, and investing heavily in regenerative veterinary research. Many introduced advanced bone graft materials that offer improved healing dynamics and biocompatibility. While some players focused on niche veterinary applications, others expanded their geographical footprint to tap into emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing pet ownership and expenditure

- 3.2.1.2 Growing prevalence of orthopedic conditions in animals

- 3.2.1.3 Advancements in veterinary regenerative medicine

- 3.2.1.4 Growing pet insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of bone grafts and substitutes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Autografts

- 5.3 Allografts

- 5.4 Xenografts

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Animal, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Horses

- 6.5 Other animals

Chapter 7 Market Estimates and Forecast, By Form, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Powders

- 7.3 Putty

- 7.4 Granules

- 7.5 Injectables

- 7.6 Other forms

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedic

- 8.3 Dental

- 8.4 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals

- 9.3 Veterinary clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Biomendex

- 11.2 BioChange

- 11.3 Biomimetic Solutions

- 11.4 Cavix

- 11.5 Exabone

- 11.6 Lynch Biologics

- 11.7 Movora (Vimian Group AB)

- 11.8 Nutramax Laboratories Veterinary Sciences

- 11.9 Rita Leibinger

- 11.10 S-VETOSS

- 11.11 TheraVet

- 11.12 Veteregen

- 11.13 Wishbone

骨移植固定系統市場:按材料、器材、應用和最終用戶分類-2026-2032年全球市場預測

骨移植固定系統市場:按材料、器材、應用和最終用戶分類-2026-2032年全球市場預測 骨移植材料替代品市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類的洞察,以及 2026-2034 年的預測。

骨移植材料替代品市場規模、佔有率、成長和全球產業分析:按類型、應用和地區分類的洞察,以及 2026-2034 年的預測。 2026年全球骨移植固定系統市場報告

2026年全球骨移植固定系統市場報告 按產品類型、應用和地區分類的骨移植和骨替代材料市場骨癒合系統市場:依產品類型、技術、解剖結構、銷售管道、應用、最終用戶、患者年齡層和護理階段分類,全球預測,2026-2032年骨移植替代材料市場-2026年至2031年預測

按產品類型、應用和地區分類的骨移植和骨替代材料市場骨癒合系統市場:依產品類型、技術、解剖結構、銷售管道、應用、最終用戶、患者年齡層和護理階段分類,全球預測,2026-2032年骨移植替代材料市場-2026年至2031年預測 骨移植替代材料市場規模、佔有率和成長分析(按材料類型、應用、最終用戶和地區分類)—2026-2033年產業預測2025年骨移植和替代替代品全球市場報告

骨移植替代材料市場規模、佔有率和成長分析(按材料類型、應用、最終用戶和地區分類)—2026-2033年產業預測2025年骨移植和替代替代品全球市場報告 全球生物分解性骨移植聚合物市場

全球生物分解性骨移植聚合物市場 骨移植和替代品市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區和競爭細分,2020-2030 年預測

骨移植和替代品市場 - 全球產業規模、佔有率、趨勢、機會和預測,按材料類型、應用、地區和競爭細分,2020-2030 年預測