|

市場調查報告書

商品編碼

1721421

照明手術牽開器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lighted Surgical Retractor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

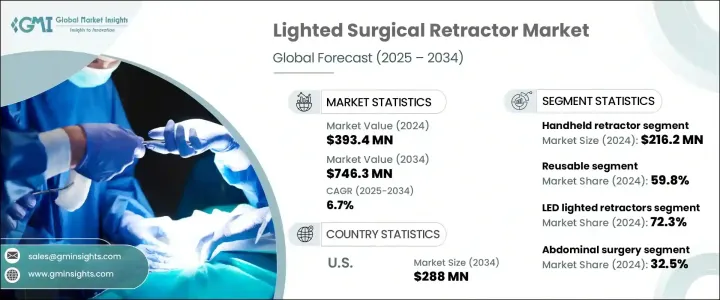

2024 年全球照明手術牽開器市場價值為 3.934 億美元,預計到 2034 年將以 6.7% 的複合年成長率成長,達到 7.463 億美元。隨著旨在改善手術結果和降低手術風險的先進手術工具的日益普及,市場正在獲得顯著發展勢頭。帶燈手術牽開器將組織牽開和照明功能集於一身,已成為現代手術室的必備工具。外科醫生越來越依賴這些創新設備來提高深部和微創手術中的可視度,從而實現更高的精度和更短的手術時間。

隨著手術過程的複雜性不斷增加以及對更高手術效率的需求不斷成長,全球的醫療保健提供者都在投資集功能性和易用性於一體的高性能手術器械。除了改善患者的治療效果外,這些牽開器還簡化了手術環境中的工作流程,使其成為當今醫學進步不可或缺的一部分。微創手術的日益普及以及需要手術干預的慢性病的日益普及進一步推動了市場擴張。技術創新、優惠的報銷結構以及對手術精準度的認知不斷提高,共同促進了醫院和門診手術中心廣泛採用帶燈牽開器。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.934億美元 |

| 預測值 | 7.463億美元 |

| 複合年成長率 | 6.7% |

市場分為手持式和自保持式牽開器。手持式牽開器市場價值 2.162 億美元,由於其輕量化設計、便攜性和成本效益,正在實現顯著成長。外科醫生更喜歡手持式手術,因為它們具有靈活性和增強的照明能力,適用於從一般手術到高度專業化的干涉等各種手術。這些牽開器易於操作且現場照明清晰,有助於提高準確性並減少併發症。

隨著醫療機構繼續優先考慮永續實踐,可重複使用部分在 2024 年佔據 59.8% 的佔有率。向可重複使用設備的轉變得益於減少醫療保健相關浪費(尤其是一次性塑膠)和降低長期營運成本的需求。作為更廣泛的綠色計劃的一部分,醫院和外科中心擴大投資可重複使用的發光牽開器,同時又不影響性能或安全性。

2024 年,美國照明手術牽開器市場佔據了 90.2% 的主導佔有率。這一優勢得益於技術的快速進步、對以患者為中心的護理的日益重視以及頂級公司和研究機構的持續支持。憑藉良好的監管框架和對醫療技術的持續投資,該國繼續引領尖端手術工具(包括帶燈牽引器)的開發和應用。

全球產業的主要參與者包括 Stryker、Medtronic、Millennium Surgical、Medline、Electro Surgical Instrument Company、Black & Black Surgical、Hayden Medical、Yasuico、Sunoptic Technologies、Carnegie Surgical 和 Cooper Surgical。這些公司專注於產品創新、研發以及與醫療保健提供者的策略合作夥伴關係,以提高績效、擴大市場範圍並滿足日益成長的臨床需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 微創手術的需求不斷增加

- 慢性病盛行率不斷上升

- 帶燈手術牽開器的技術進步

- 產業陷阱與挑戰

- 先進的帶燈手術牽開器成本高昂

- 與維護和滅菌相關的挑戰

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 手持式牽開器

- 自保持牽開器

第6章:市場估計與預測:按使用類型,2021 - 2034 年

- 一次性使用/拋棄式

- 可重複使用的

第7章:市場估計與預測:按光源,2021 - 2034 年

- 主要趨勢

- LED照明牽開器

- 光纖牽開器

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 腹部手術

- 骨科手術

- 整型手術

- 婦科

- 神經外科

- 其他應用

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 專科診所

- 醫院

- 學術和研究機構

- 門診手術中心

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Black and Black Surgical

- Carnegie Surgical

- Cooper Surgical

- Electro Surgical Instrument Company

- Hayden Medical

- June Medical

- Medline

- Medtronic

- Millennium Surgical

- Stryker

- Sunoptic Technologies

- Yasuico

The Global Lighted Surgical Retractor Market was valued at USD 393.4 million in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 746.3 million by 2034. The market is gaining significant momentum due to the rising adoption of advanced surgical tools designed to improve outcomes and reduce procedural risks. Lighted surgical retractors, which combine tissue retraction and illumination into a single device, have emerged as essential tools in modern operating rooms. Surgeons are increasingly relying on these innovative devices to enhance visibility during deep and minimally invasive procedures, allowing for greater precision and shorter operative times.

With increasing procedural complexity and growing demand for better surgical efficiency, healthcare providers across the globe are investing in high-performance surgical instruments that integrate functionality and ease of use. In addition to improving patient outcomes, these retractors are also streamlining workflows in surgical settings, making them an integral part of today's medical advancements. The growing trend toward minimally invasive surgeries and the increasing prevalence of chronic diseases requiring surgical intervention are further propelling market expansion. Technological innovations, favorable reimbursement structures, and heightened awareness of surgical precision are collectively contributing to the widespread adoption of lighted retractors in hospitals and ambulatory surgery centers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $393.4 Million |

| Forecast Value | $746.3 Million |

| CAGR | 6.7% |

The market is divided into handheld and self-retaining retractors. The handheld retractor segment, valued at USD 216.2 million in 2024, is witnessing significant growth driven by its lightweight design, portability, and cost-efficiency. Surgeons prefer handheld options for their flexibility and enhanced lighting capabilities, making them suitable for a wide range of procedures, from general surgeries to highly specialized interventions. These retractors offer ease of maneuverability and clear site illumination, helping improve accuracy and reduce complications.

The reusable segment held a 59.8% share in 2024 as healthcare institutions continue prioritizing sustainable practices. The shift toward reusable devices is supported by the need to reduce healthcare-related waste, especially single-use plastics, and lower long-term operational costs. Hospitals and surgical centers are increasingly investing in reusable lighted retractors as a part of their broader green initiatives without compromising on performance or safety.

The U.S. Lighted Surgical Retractor Market accounted for a dominant 90.2% share in 2024. This stronghold is fueled by rapid technological progress, increased emphasis on patient-centric care, and consistent support from top-tier companies and research bodies. With favorable regulatory frameworks and ongoing investments in medical technology, the country continues to lead the development and adoption of cutting-edge surgical tools, including lighted retractors.

Key players in the global industry include Stryker, Medtronic, Millennium Surgical, Medline, Electro Surgical Instrument Company, Black & Black Surgical, Hayden Medical, Yasuico, Sunoptic Technologies, Carnegie Surgical, and Cooper Surgical. These companies are focusing on product innovation, research and development, and strategic partnerships with healthcare providers to enhance performance, expand market reach, and meet growing clinical demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgeries

- 3.2.1.2 Growing prevalence of chronic diseases

- 3.2.1.3 Technological advancements in lighted surgical retractors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced lighted surgical retractors

- 3.2.2.2 Challenges associated with maintenance and sterilization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Handheld retractors

- 5.3 Self-retaining retractors

Chapter 6 Market Estimates and Forecast, By Usage Type, 2021 - 2034 ($ Mn)

- 6.1 Single use / disposable

- 6.2 Reusable

Chapter 7 Market Estimates and Forecast, By Light Source, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 LED lighted retractors

- 7.3 Fiber optic retractors

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Abdominal surgery

- 8.2 Orthopedic surgery

- 8.3 Plastic surgery

- 8.4 Gynecology

- 8.5 Neurological surgery

- 8.6 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Specialty clinics

- 9.3 Hospitals

- 9.4 Academic and research institutes

- 9.5 Ambulatory surgical centers

- 9.6 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Black and Black Surgical

- 11.2 Carnegie Surgical

- 11.3 Cooper Surgical

- 11.4 Electro Surgical Instrument Company

- 11.5 Hayden Medical

- 11.6 June Medical

- 11.7 Medline

- 11.8 Medtronic

- 11.9 Millennium Surgical

- 11.10 Stryker

- 11.11 Sunoptic Technologies

- 11.12 Yasuico

外科牽開器市場:按產品類型、材料、銷售管道、應用和最終用戶分類-2026-2032年全球市場預測

外科牽開器市場:按產品類型、材料、銷售管道、應用和最終用戶分類-2026-2032年全球市場預測 牽開器市場報告:趨勢、預測與競爭分析(至2035年)乳房手術牽開器市場:2026-2032年全球市場預測(按產品類型、材料、應用、分銷管道和最終用戶分類)

牽開器市場報告:趨勢、預測與競爭分析(至2035年)乳房手術牽開器市場:2026-2032年全球市場預測(按產品類型、材料、應用、分銷管道和最終用戶分類) 外科固定器市場規模、佔有率和成長分析:按產品類型、材質、最終用戶、分銷管道和地區分類-2026-2033年產業預測

外科固定器市場規模、佔有率和成長分析:按產品類型、材質、最終用戶、分銷管道和地區分類-2026-2033年產業預測 2026年全球外科牽開器市場報告

2026年全球外科牽開器市場報告 全球外科牽開器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球外科牽開器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 外科牽開器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品、應用、地區和競爭格局分類,2021-2031年)

外科牽開器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按類型、產品、應用、地區和競爭格局分類,2021-2031年) 外科牽開器市場規模、佔有率、成長分析(按類型、產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測

外科牽開器市場規模、佔有率、成長分析(按類型、產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測 Deaver 牽開器的全球市場

Deaver 牽開器的全球市場 手術牽開器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

手術牽開器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測