|

市場調查報告書

商品編碼

1721411

邊緣人工智慧晶片市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Edge Artificial Intelligence Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

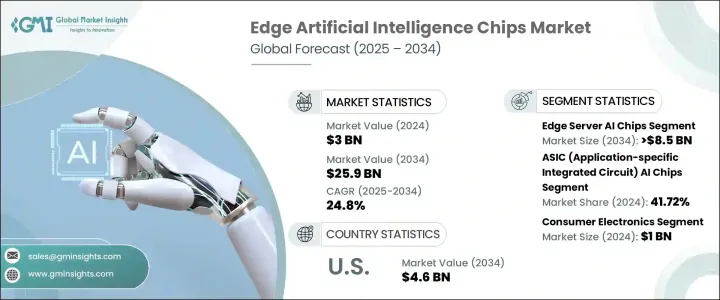

2024 年全球邊緣人工智慧晶片市場價值為 30 億美元,預計到 2034 年將以 24.8% 的複合年成長率成長,達到 259 億美元。這一顯著成長反映了計算範式的動態轉變,其中設備級的即時智慧正在迅速成為常態。隨著企業不斷實現營運數位化,對能夠在本地處理資料的高效能AI晶片組的需求正在激增。這種演變在自動駕駛、智慧製造和精準醫療等領域尤其明顯,這些領域必須立即做出決策,而不能依賴雲端延遲。邊緣 AI 晶片使智慧型裝置能夠在源頭處理、分析和處理資料,從而提供更快的回應時間並提高資料隱私性。

隨著人工智慧在消費性電子產品、工業系統和智慧基礎設施領域的深入滲透,對可擴展、節能的人工智慧硬體的需求日益加劇。此外,製造技術的進步、組件的小型化以及 5G 網路的日益普及正在加速全球邊緣 AI 解決方案的部署。越來越多的公司將邊緣人工智慧視為釋放機器人、擴增實境和智慧監控變革能力的關鍵。分散智慧和邊緣運算的結合正在重新定義資料的使用和保護方式,為晶片製造商和系統整合商提供了巨大的機會。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 30億美元 |

| 預測值 | 259億美元 |

| 複合年成長率 | 24.8% |

市場根據部署情況細分為設備上和邊緣伺服器 AI 晶片。隨著各行各業越來越重視低延遲 AI 操作和本地化資料處理,邊緣伺服器 AI 晶片預計到 2034 年將產生 85 億美元的產值。智慧城市中的即時交通監控、製造業中的預測性維護以及醫療保健中的高級診斷等用例正在推動對強大邊緣伺服器的需求。 5G 基礎設施的推出也增強了邊緣伺服器的可存取性和頻寬,使其更適合在靠近最終用戶的地方託管複雜的 AI 工作負載。

就晶片類型而言,專用積體電路 (ASIC) 佔據主導地位,到 2024 年將佔據 41.72% 的佔有率。這些晶片為目標 AI 應用提供了無與倫比的性能,使其成為語音識別、電腦視覺和 NLP 等功能的首選。它們的能源效率和處理速度繼續吸引那些需要可擴展、經濟高效的大規模部署解決方案的人工智慧硬體開發人員。

2024 年美國邊緣人工智慧晶片市場價值為 46 億美元,主要受自主系統、軍用級技術和智慧製造創新的推動。領先的科技公司正在大力投資人工智慧晶片研發,以開發醫療穿戴式裝置、自動化安全和工業機器人的先進功能。 《晶片法案》等政府措施透過資助半導體開發和確保關鍵人工智慧技術的供應鏈彈性,進一步促進了成長。

全球邊緣人工智慧晶片市場的領先公司包括高通技術公司、NVIDIA Corporation、Arm Limited、Advanced Micro Devices, Inc.、Broadcom Inc.、Apple、STMicroelectronics、德州儀器公司、聯發科技公司、萊迪思半導體公司、Mythic、Marvell、Synaptics Incorporated、BrainC, Inc.L.L.各公司積極投入研發,以降低晶片功耗並提高處理效率。許多公司正在擴大製造業務,以滿足物聯網、自動駕駛汽車和智慧基礎設施領域日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 半導體需求不斷成長

- 物聯網應用激增

- 對低延遲處理的需求不斷成長

- 5G網路的擴展

- 消費性電子產品對人工智慧的需求不斷成長

- 產業陷阱與挑戰

- 高功耗和熱管理

- 複雜的硬體和軟體整合

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按晶片類型,2021 - 2034

- 主要趨勢

- ASIC(專用積體電路)AI晶片

- GPU(圖形處理單元)AI晶片

- CPU(中央處理器)AI晶片

- FPGA(現場可程式閘陣列)AI晶片

- 神經形態人工智慧晶片

第6章:市場估計與預測:按部署,2021 - 2034 年

- 主要趨勢

- 裝置上的邊緣 AI 晶片

- 邊緣伺服器AI晶片

第7章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 消費性電子產品

- 汽車與運輸

- 醫療保健和醫療器械

- 零售與電子商務

- 製造和工業自動化

- 電信

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳新銀行

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Advanced Micro Devices, Inc.

- Apple

- Arm Limited

- BrainChip, Inc.

- Broadcom Inc.

- HAILO TECHNOLOGIES LTD

- Huawei Cloud Computing Technologies Co., Ltd

- Intel Corporation

- Lattice Semiconductor

- Marvell

- MediaTek Inc

- Mythic

- NVIDIA Corporation

- Qualcomm Technologies

- STMicroelectronics

- Synaptics Incorporated

- Texas Instruments Incorporated

The Global Edge Artificial Intelligence Chips Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 24.8% to reach USD 25.9 billion by 2034. This significant growth reflects a dynamic shift in computing paradigms, where real-time intelligence at the device level is rapidly becoming the norm. As enterprises continue to digitize operations, the demand for high-performance AI chipsets that can process data locally is surging. This evolution is particularly pronounced in sectors such as autonomous driving, smart manufacturing, and precision healthcare, where decisions must be made instantly without reliance on cloud latency. Edge AI chips enable smart devices to process, analyze, and act on data at the source, offering faster response times and improved data privacy.

With AI penetrating deeper into consumer electronics, industrial systems, and smart infrastructure, the demand for scalable, energy-efficient AI hardware is intensifying. Furthermore, advancements in fabrication technology, miniaturization of components, and growing access to 5G networks are accelerating the deployment of edge AI solutions worldwide. Companies are increasingly viewing edge AI as the key to unlocking transformative capabilities in robotics, augmented reality, and intelligent surveillance. The combination of decentralized intelligence and edge computing is redefining how data is used and secured, presenting a tremendous opportunity for chipmakers and system integrators alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 24.8% |

The market is segmented by deployment into on-device and edge server AI chips. Edge server AI chips are projected to generate USD 8.5 billion by 2034 as industries increasingly prioritize low-latency AI operations and localized data processing. Use cases like real-time traffic monitoring in smart cities, predictive maintenance in manufacturing, and advanced diagnostics in healthcare are pushing demand for robust edge servers. The rollout of 5G infrastructure is also enhancing edge server accessibility and bandwidth, making them more viable for hosting complex AI workloads close to end-users.

In terms of chip type, application-specific integrated circuits (ASICs) dominate the landscape, capturing a 41.72% share in 2024. These chips offer unmatched performance for targeted AI applications, making them a top choice for functions like speech recognition, computer vision, and NLP. Their energy efficiency and processing speed continue to attract AI hardware developers who need scalable, cost-effective solutions for mass deployment.

The U.S. Edge Artificial Intelligence Chips Market was valued at USD 4.6 billion in 2024, largely driven by innovation in autonomous systems, military-grade technology, and smart manufacturing. Leading tech firms are heavily investing in AI chip R&D to develop advanced capabilities for healthcare wearables, automated security, and industrial robotics. Government initiatives such as the CHIPS Act are further amplifying growth by funding semiconductor development and ensuring supply chain resilience for critical AI technologies.

Leading companies in the Global Edge Artificial Intelligence Chips Market include Qualcomm Technologies, NVIDIA Corporation, Arm Limited, Advanced Micro Devices, Inc., Broadcom Inc., Apple, STMicroelectronics, Texas Instruments Incorporated, MediaTek Inc., Lattice Semiconductor, Mythic, Marvell, Synaptics Incorporated, BrainChip, Inc., HAILO TECHNOLOGIES LTD, Huawei Cloud Computing Technologies Co., Ltd, and Intel Corporation. Companies are actively investing in R&D to reduce chip power consumption and enhance processing efficiency. Many are expanding manufacturing operations to meet escalating demands from the IoT, autonomous vehicle, and smart infrastructure sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for semiconductors

- 3.2.1.2 Surge in IoT adoption

- 3.2.1.3 Rising need for low-latency processing

- 3.2.1.4 Expansion of 5G networks

- 3.2.1.5 Growing demand for AI in consumer electronics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High power consumption and thermal management

- 3.2.2.2 Complex hardware and software integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Chip Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 ASIC (Application-Specific Integrated Circuit) AI Chips

- 5.3 GPU (Graphics Processing Unit) AI Chips

- 5.4 CPU (Central Processing Unit) AI Chips

- 5.5 FPGA (Field-Programmable Gate Array) AI Chips

- 5.6 Neuromorphic AI Chips

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 On-Device Edge AI Chips

- 6.3 Edge Server AI Chips

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.3 Automotive & transportation

- 7.4 Healthcare & medical devices

- 7.5 Retail & e-commerce

- 7.6 Manufacturing & industrial automation

- 7.7 Telecommunications

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Advanced Micro Devices, Inc.

- 9.2 Apple

- 9.3 Arm Limited

- 9.4 BrainChip, Inc.

- 9.5 Broadcom Inc.

- 9.6 HAILO TECHNOLOGIES LTD

- 9.7 Huawei Cloud Computing Technologies Co., Ltd

- 9.8 Intel Corporation

- 9.9 Lattice Semiconductor

- 9.10 Marvell

- 9.11 MediaTek Inc

- 9.12 Mythic

- 9.13 NVIDIA Corporation

- 9.14 Qualcomm Technologies

- 9.15 STMicroelectronics

- 9.16 Synaptics Incorporated

- 9.17 Texas Instruments Incorporated

2026年全球事件驅動型音訊邊緣晶片市場報告

2026年全球事件驅動型音訊邊緣晶片市場報告 低延遲音訊晶片市場報告:趨勢、預測和競爭分析(至2035年)

低延遲音訊晶片市場報告:趨勢、預測和競爭分析(至2035年) 邊緣人工智慧解決方案市場預測至2034年—按組件、設備類型、功能、部署模式、應用、最終用戶和地區分類的全球分析2026年全球邊緣人工智慧晶片市場報告

邊緣人工智慧解決方案市場預測至2034年—按組件、設備類型、功能、部署模式、應用、最終用戶和地區分類的全球分析2026年全球邊緣人工智慧晶片市場報告 邊緣人工智慧晶片:技術、市場及預測(2026-2036)

邊緣人工智慧晶片:技術、市場及預測(2026-2036) GaN射頻晶片市場按頻段、輸出功率、裝置類型、基板類型、應用和最終用戶產業分類,全球預測(2026-2032年)全球邊緣人工智慧晶片市場規模(按處理器、設備類型、功能、地區和預測)2030 年邊緣人工智慧晶片市場預測:按晶片類型、設備類型、應用、最終用戶和地區進行全球分析邊緣人工智慧晶片市場報告:2030 年趨勢、預測與競爭分析

GaN射頻晶片市場按頻段、輸出功率、裝置類型、基板類型、應用和最終用戶產業分類,全球預測(2026-2032年)全球邊緣人工智慧晶片市場規模(按處理器、設備類型、功能、地區和預測)2030 年邊緣人工智慧晶片市場預測:按晶片類型、設備類型、應用、最終用戶和地區進行全球分析邊緣人工智慧晶片市場報告:2030 年趨勢、預測與競爭分析