|

市場調查報告書

商品編碼

1721406

加熱擋風玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Heated Windshield Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

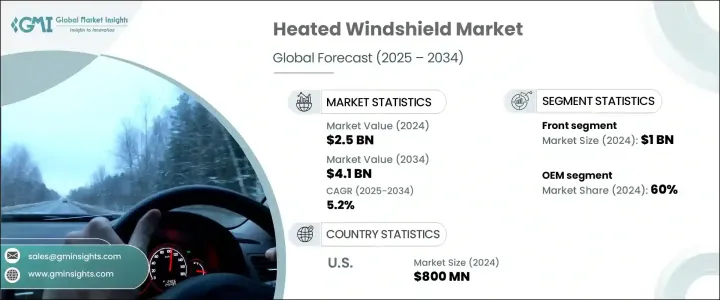

2024 年全球加熱擋風玻璃市場價值為 25 億美元,預計到 2034 年將以 5.2% 的複合年成長率成長至 41 億美元。這一成長主要得益於消費者對提高可視性、增強安全功能以及增強極端天氣條件下適應性的需求不斷成長。隨著天氣越來越難以預測,尤其是在寒冷地區,汽車購買者更加重視確保駕駛員安全和舒適的技術。加熱擋風玻璃尤其受到廣泛關注,因為它們能夠快速清除冰、霜和霧,而不會給 HVAC 系統帶來過重負擔。隨著汽車產業向電動和豪華汽車的強勁轉變,加熱擋風玻璃系統正在成為支援能源效率和先進駕駛輔助系統(ADAS) 的標準功能。

智慧功能的日益融合以及對更高車輛性能的追求促使汽車製造商投資更可靠、耐用和節能的擋風玻璃技術。此外,導電塗層和嵌入式加熱元件的進步正在重塑競爭格局,並影響OEM和售後市場管道的購買決策。製造商正在透過適應不斷變化的監管標準和消費者對安全性、效率和永續性的期望來做出回應,預計這將在整個預測期內進一步推動採用和技術創新。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 25億美元 |

| 預測值 | 41億美元 |

| 複合年成長率 | 5.2% |

加熱擋風玻璃經過專門設計,可消除霜、霧和冰的積聚,從而在惡劣天氣下提供清晰的視野,從而提高安全性。這些解決方案對於電動和高級汽車尤其重要,因為快速除霜不僅可以提高駕駛者的舒適度,還可以確保 ADAS 的無縫運作。嵌入式電線和透明導電層等先進加熱技術的結合,可以實現更快的除霧、更強的耐磨性,並減少對傳統氣候控制系統的依賴,使加熱擋風玻璃成為現代車輛的寶貴資產。

市場分為前擋風玻璃和後擋風玻璃,其中前擋風玻璃市場在 2024 年將創造 10 億美元。該市場的重要性主要歸功於其在保持駕駛員可視性和支持需要暢通視野的 ADAS 組件方面所發揮的作用。後加熱擋風玻璃的牽引力也在增加,特別是在車隊和商用車輛中,因為在倒車時後方可視性至關重要。然而,後擋風玻璃的採用率仍然落後於前擋風玻璃。

就銷售通路而言,市場分為原始設備製造商(OEM)和售後市場。 2024 年,原始設備製造商 (OEM) 佔據了 60% 的市場佔有率,這主要歸因於電動和高階汽車對工廠安裝解決方案的需求不斷成長。這些擋風玻璃與 ADAS 和自動駕駛系統無縫整合,即使在惡劣條件下也能確保頂級性能。

受電動和豪華汽車日益普及以及對先進安全技術的需求推動,美國加熱擋風玻璃市場規模到 2024 年將達到 8 億美元。美國汽車製造商正在積極實施加熱擋風玻璃系統,以滿足消費者對節能和卓越可視性的需求。這些系統透過降低 HVAC 負載並確保最佳除霜性能,在保持電動車電池效率方面發揮關鍵作用。

全球加熱擋風玻璃領域的主要領導者包括日本板硝子、AGC、福耀玻璃、加迪安玻璃、大眾、皮爾金頓、麥格納、聖戈班安全玻璃、特斯拉和豐田汽車。這些參與者正在大力投資研發下一代加熱技術,並與原始設備製造商建立策略合作夥伴關係,以滿足豪華和高性能汽車領域日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 組件提供者

- 製造商

- 技術提供者

- 配銷通路分析

- 最終用途

- 利潤率分析

- 供應商格局

- 技術與創新格局

- 專利分析

- 監管格局

- 成本細分分析

- 重要新聞和舉措

- 衝擊力

- 成長動力

- 電動車的普及率不斷提高

- 智慧玻璃和導電塗層的進步

- 更嚴格的安全和能見度規定

- 商用車領域的擴張

- 產業陷阱與挑戰

- 製造和更換成本高

- 與 ADAS 和智慧功能的複雜整合

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依位置,2021 - 2034 年

- 主要趨勢

- 正面

- 後部

第6章:市場估計與預測:按玻璃,2021 - 2034 年

- 主要趨勢

- 層壓

- 導電鍍膜玻璃

- 經過調和

- 其他

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- 越野車

- 商用車

- 輕型商用車

- 平均血紅素 (MCV)

- 丙型肝炎病毒

第8章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- 售後市場

- OEM

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- AGC

- BMW

- Corning

- Ford Motor

- Fuyao Glass

- General Motors

- Guardian Glass

- Hyundai Motor

- Magna

- Mercedes-Benz

- Nippon Sheet Glass

- Pilkington

- Saint-Gobain Sekurit

- Stellantis

- Tesla

- Toyota

- Volkswagen

- Volvo

- Webasto

- Xinyi Glass

The Global Heated Windshield Market was valued at USD 2.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 4.1 billion by 2034. This growth is primarily driven by rising consumer demand for improved visibility, enhanced safety features, and increased adaptability in extreme weather conditions. As weather unpredictability intensifies, especially in colder regions, automotive buyers are placing greater importance on technologies that ensure driver safety and comfort. Heated windshields, in particular, are gaining significant attention due to their ability to rapidly clear ice, frost, and fog without overburdening the HVAC system. With the automotive industry witnessing a strong shift toward electric and luxury vehicles, heated windshield systems are becoming standard features that support energy efficiency and advanced driver assistance systems (ADAS).

The growing integration of smart features and the push for higher vehicle performance have prompted automakers to invest in more reliable, durable, and energy-efficient windshield technologies. Additionally, advancements in conductive coatings and embedded heating elements are reshaping the competitive landscape and influencing purchase decisions across both OEM and aftermarket channels. Manufacturers are responding by aligning with evolving regulatory standards and consumer expectations for safety, efficiency, and sustainability, which is expected to further drive adoption and technological innovation throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.2% |

Heated windshields are specifically designed to boost safety by eliminating the accumulation of frost, fog, and ice, thereby offering clear visibility in adverse weather. These solutions are especially important in electric and premium vehicles where fast defrosting supports not only driver comfort but also ensures the seamless functioning of ADAS. The incorporation of advanced heating technologies, such as embedded wires and transparent conductive layers, allows for faster defogging, greater resistance to wear, and reduced reliance on traditional climate control systems-making heated windshields a valuable asset in modern vehicles.

The market is categorized into front and rear windshields, with the front segment generating USD 1 billion in 2024. The prominence of this segment is largely attributed to its role in maintaining driver visibility and supporting ADAS components that require an unobstructed view. Rear heated windshields are also experiencing increased traction, especially in fleet and commercial vehicles, where rear visibility is critical during reversing. However, the adoption rate of rear windshields still trails that of the front segment.

In terms of sales channels, the market is divided between original equipment manufacturers (OEMs) and the aftermarket. OEMs accounted for 60% of the market share in 2024, largely due to the rising demand for factory-installed solutions in electric and high-end vehicles. These windshields are seamlessly integrated with ADAS and self-driving systems, ensuring top-tier performance even in harsh conditions.

The U.S. Heated Windshield Market reached USD 800 million in 2024, propelled by the growing adoption of electric and luxury vehicles, along with the demand for advanced safety technologies. U.S. automakers are actively implementing heated windshield systems to address consumer needs for energy savings and superior visibility. These systems play a pivotal role in preserving battery efficiency in EVs by reducing the HVAC load and ensuring optimal defrosting performance.

Key companies leading the global heated windshield space include Nippon Sheet Glass, AGC, Fuyao Glass, Guardian Glass, Volkswagen, Pilkington, Magna, Saint-Gobain Sekurit, Tesla, and Toyota Motor. These players are heavily investing in R&D to develop next-generation heating technologies and are forging strategic partnerships with OEMs to cater to the rising demand in luxury and high-performance vehicle segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing adoption in electric vehicles

- 3.7.1.2 Advancements in smart glass & conductive coatings

- 3.7.1.3 Stricter safety & visibility regulations

- 3.7.1.4 Expansion in the commercial vehicle segment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High manufacturing & replacement costs

- 3.7.2.2 Complex integration with ADAS & smart features

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Position, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Front

- 5.3 Rear

Chapter 6 Market Estimates & Forecast, By Glass, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Laminated

- 6.3 Conductive coated glass

- 6.4 Tempered

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Aftermarket

- 8.3 OEM

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 UK

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AGC

- 10.2 BMW

- 10.3 Corning

- 10.4 Ford Motor

- 10.5 Fuyao Glass

- 10.6 General Motors

- 10.7 Guardian Glass

- 10.8 Hyundai Motor

- 10.9 Magna

- 10.10 Mercedes-Benz

- 10.11 Nippon Sheet Glass

- 10.12 Pilkington

- 10.13 Saint-Gobain Sekurit

- 10.14 Stellantis

- 10.15 Tesla

- 10.16 Toyota

- 10.17 Volkswagen

- 10.18 Volvo

- 10.19 Webasto

- 10.20 Xinyi Glass

汽車擋風玻璃市場:按玻璃類型、感測器整合、技術、車輛類型和銷售管道分類-2026-2032年全球市場預測

汽車擋風玻璃市場:按玻璃類型、感測器整合、技術、車輛類型和銷售管道分類-2026-2032年全球市場預測 2026-2034年全球汽車擋風玻璃市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球汽車擋風玻璃市場規模、佔有率、趨勢和成長分析報告 2026年全球汽車擋風玻璃市場報告2026年火箭飛行器熱控全球市場報告2026年全球汽車加熱擋風玻璃市場報告

2026年全球汽車擋風玻璃市場報告2026年火箭飛行器熱控全球市場報告2026年全球汽車加熱擋風玻璃市場報告 汽車擋風玻璃市場機會、成長要素、產業趨勢分析及2026年至2035年預測

汽車擋風玻璃市場機會、成長要素、產業趨勢分析及2026年至2035年預測 汽車擋風玻璃市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、玻璃類型、材料類型、地區和競爭格局分類,2021-2031年)

汽車擋風玻璃市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、玻璃類型、材料類型、地區和競爭格局分類,2021-2031年) 汽車擋風玻璃市場規模、佔有率和成長分析(按車輛類型、電動車類型、安裝位置、材質、玻璃類型和地區分類)-2026-2033年產業預測

汽車擋風玻璃市場規模、佔有率和成長分析(按車輛類型、電動車類型、安裝位置、材質、玻璃類型和地區分類)-2026-2033年產業預測 2024-2028年全球汽車擋風玻璃市場

2024-2028年全球汽車擋風玻璃市場