|

市場調查報告書

商品編碼

1716721

蝶閥市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Butterfly Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

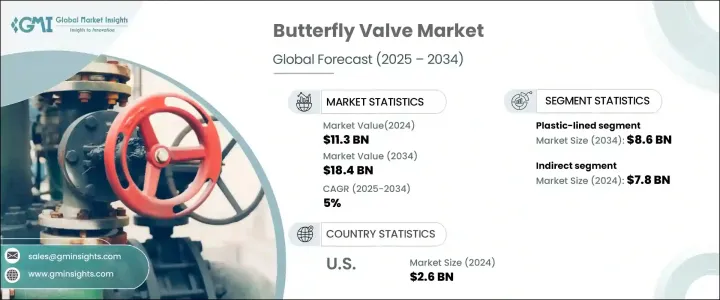

2024 年全球蝶閥市場規模達 113 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5%。這一成長主要得益於石油和天然氣、發電和水處理等產業工業自動化的快速發展。隨著各行各業越來越重視提高營運效率和減少人為干預,對自動化和遠端控制閥門的需求持續上升。蝶閥以其輕巧的設計、成本效益和快速操作而聞名,正在成為智慧流量控制系統的首選。它們的多功能性和可靠性使其成為各種工業應用中不可或缺的一部分,可確保流程的順利和高效。

全球越來越關注改善水和廢水管理基礎設施是推動蝶閥需求的另一個重要因素。尤其是發展中地區,正在經歷水處理廠建設的激增,以解決人們對水消耗日益成長的擔憂以及政府對廢水管理的嚴格規定。隨著工業和市政當局對先進水管理系統的投資,蝶閥因其能夠高效處理大量水且維護成本極低而成為理想的解決方案。它們的耐用性和成本效益使其成為大規模應用的可靠選擇,確保了水處理設施的長期運作效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 113億美元 |

| 預測值 | 184億美元 |

| 複合年成長率 | 5% |

蝶閥市場根據襯裡類型分為塑膠襯裡閥門、金屬襯裡閥門和橡膠襯裡閥門。由於塑膠內襯具有優異的耐腐蝕和耐化學性,該領域在 2024 年創造了 51 億美元的收入。這些閥門因其耐用性、低維護要求以及在處理腐蝕性流體方面的出色性能而受到化學加工和製藥等行業的青睞。隨著各行各業擴大採用耐腐蝕解決方案來延長設備的使用壽命,塑膠襯裡蝶閥的需求持續強勁。

從分銷通路來看,市場分為直接銷售和間接銷售。間接分銷通路的價值在 2024 年將達到 78 億美元,預計到 2034 年將以 4.8% 的複合年成長率成長。儘管直接分銷管道有所成長,但許多製造商仍依賴間接網路(包括代理商、批發商和零售商)來推廣和分銷其產品。這些中間商在擴大市場範圍方面發揮關鍵作用,特別是在工業領域,信任關係和建立的供應鏈對於推動銷售和確保產品供應至關重要。

美國蝶閥市場規模在 2024 年達到 26 億美元,預計在 2025 年至 2034 年期間的複合年成長率為 5.5%。美國擁有強大的基礎設施和先進的製造能力,尤其是在石油和天然氣、水管理和發電等行業,使美國成為北美市場的重要參與者。此外,嚴格的環境法規和工業流程自動化水準的提高繼續推動該地區對先進蝶閥的需求。隨著美國各行業採用創新技術來滿足法規遵循和營運效率,蝶閥市場將在未來幾年穩步成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 零售商

- 衝擊力

- 成長動力

- 工業自動化需求不斷成長

- 擴建水和廢水處理設施

- 石油天然氣和化學加工領域的投資不斷增加

- 產業陷阱與挑戰

- 原物料價格波動

- 替代流量控制技術的可用性

- 成長動力

- 成長潛力分析

- 原料分析

- 監管格局

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按襯裡類型,2021-2034

- 主要趨勢

- 橡膠內襯

- 塑膠內襯

- 金屬內襯

第6章:市場估計與預測:依材料,2021-2034

- 主要趨勢

- 碳鋼

- 不銹鋼

- 鐵

- 其他

第7章:市場估計與預測:按安裝類型,2021-2034

- 主要趨勢

- 晶圓

- 半凸耳

- 凸耳

- 雙法蘭

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 水和廢水

- 石油和天然氣

- 能源和電力

- 製藥

- 化學品

- 其他

第9章:市場估計與預測:按配銷通路,2021-2034

- 主要趨勢

- 直接的

- 間接

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第 11 章:公司簡介

- Alfa Laval

- AVK Group

- Bray International

- Crane

- Curtiss-Wright

- DeZURIK

- Emerson Electric

- Flowserve

- Grundfos

- Honeywell International

- Neles

- SPX FLOW

- Velan

- Weir Group

- Xylem

The Global Butterfly Valve Market generated USD 11.3 billion in 2024 and is projected to grow at a CAGR of 5% between 2025 and 2034. This growth is primarily driven by rapid advancements in industrial automation across industries such as oil & gas, power generation, and water treatment. As industries increasingly emphasize enhancing operational efficiency and minimizing human intervention, the demand for automated and remotely controlled valves continues to rise. Butterfly valves, known for their lightweight design, cost-effectiveness, and quick operation, are becoming the preferred choice for smart flow control systems. Their versatility and reliability make them indispensable in various industrial applications, ensuring smooth and efficient processes.

The increasing global focus on improving water and wastewater management infrastructure is another significant factor fueling the demand for butterfly valves. Developing regions, in particular, are experiencing a surge in the construction of water treatment plants to address growing concerns over water consumption and stringent government regulations on wastewater management. As industries and municipalities invest in advanced water management systems, butterfly valves emerge as the ideal solution due to their ability to handle large water volumes efficiently and with minimal maintenance. Their durability and cost-effectiveness make them a reliable choice for large-scale applications, ensuring long-term operational efficiency in water treatment facilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.3 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 5% |

The butterfly valve market is segmented by lining type into plastic-lined, metal-lined, and rubber-lined valves. The plastic-lined segment generated USD 5.1 billion in 2024, driven by its superior resistance to corrosion and chemicals. These valves are highly preferred in industries such as chemical processing and pharmaceuticals due to their durability, low maintenance requirements, and excellent performance in handling aggressive fluids. As industries increasingly adopt corrosion-resistant solutions to prolong the lifespan of their equipment, plastic-lined butterfly valves continue to witness strong demand.

In terms of distribution channels, the market is divided into direct and indirect sales. The indirect segment, valued at USD 7.8 billion in 2024, is expected to grow at a CAGR of 4.8% through 2034. Despite the growth of direct distribution channels, many manufacturers still rely on indirect networks, including agents, wholesalers, and retailers, to promote and distribute their products. These intermediaries play a critical role in expanding market reach, particularly in industrial sectors where trusted relationships and established supply chains are essential for driving sales and ensuring product availability.

The U.S. butterfly valve market reached USD 2.6 billion in 2024 and is projected to grow at a CAGR of 5.5% between 2025 and 2034. The country's robust infrastructure and advanced manufacturing capabilities, especially in industries such as oil and gas, water management, and power generation, position the U.S. as a key player in the North American market. Additionally, stringent environmental regulations and increasing levels of automation in industrial processes continue to drive the demand for advanced butterfly valves in the region. As industries in the U.S. adopt innovative technologies to meet regulatory compliance and operational efficiency, the butterfly valve market is poised for steady growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for industrial automation

- 3.2.1.2 Expansion of water and wastewater treatment facilities

- 3.2.1.3 Rising investments in oil & gas and chemical processing

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Availability of alternative flow control technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Raw Material analysis

- 3.5 Regulatory landscape

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Lining Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Rubber lined

- 5.3 Plastic lined

- 5.4 Metal lined

Chapter 6 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Carbon steel

- 6.3 Stainless steel

- 6.4 Iron

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Mounting Type, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Wafer

- 7.3 Semi lug

- 7.4 Lug

- 7.5 Double flanges

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Water and wastewater

- 8.3 Oil and gas

- 8.4 Energy and power

- 8.5 Pharmaceuticals

- 8.6 Chemicals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key Trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Alfa Laval

- 11.2 AVK Group

- 11.3 Bray International

- 11.4 Crane

- 11.5 Curtiss-Wright

- 11.6 DeZURIK

- 11.7 Emerson Electric

- 11.8 Flowserve

- 11.9 Grundfos

- 11.10 Honeywell International

- 11.11 Neles

- 11.12 SPX FLOW

- 11.13 Velan

- 11.14 Weir Group

- 11.15 Xylem

晶片式橡膠襯裡蝶閥市場:按端部連接類型、操作類型、閥門尺寸類別、額定壓力類別、襯裡材料類型和行業分類,全球預測,2026-2032年

晶片式橡膠襯裡蝶閥市場:按端部連接類型、操作類型、閥門尺寸類別、額定壓力類別、襯裡材料類型和行業分類,全球預測,2026-2032年 全球軟密封蝶閥市場規模、佔有率、趨勢及成長分析報告(2026-2034)

全球軟密封蝶閥市場規模、佔有率、趨勢及成長分析報告(2026-2034) 2026年全球蝶閥市場報告

2026年全球蝶閥市場報告 全球蝶閥市場,2026-2030年LED電蚊拍市場按產品類型、應用和分銷管道分類,全球預測(2026-2032年)全球桌面式電動滅蚊器市場(按產品類型、分銷管道、最終用戶和功耗分類)預測(2026-2032年)哈氏合金C-22市場依最終用途產業、形狀、製造流程和銷售管道-2026年至2032年全球預測紫外線電蚊拍市場:依產品類型、應用程式、銷售管道和最終用戶分類,全球預測(2026-2032年)

全球蝶閥市場,2026-2030年LED電蚊拍市場按產品類型、應用和分銷管道分類,全球預測(2026-2032年)全球桌面式電動滅蚊器市場(按產品類型、分銷管道、最終用戶和功耗分類)預測(2026-2032年)哈氏合金C-22市場依最終用途產業、形狀、製造流程和銷售管道-2026年至2032年全球預測紫外線電蚊拍市場:依產品類型、應用程式、銷售管道和最終用戶分類,全球預測(2026-2032年) 蝶閥市場規模、佔有率和成長分析(按閥門類型、驅動機構、材質、最終用途產業和地區分類)-2026-2033年產業預測

蝶閥市場規模、佔有率和成長分析(按閥門類型、驅動機構、材質、最終用途產業和地區分類)-2026-2033年產業預測 熱塑性閥門、配件和管道:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

熱塑性閥門、配件和管道:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)