|

市場調查報告書

商品編碼

1716698

儲存區域網路交換器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Storage Area Network Switches Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

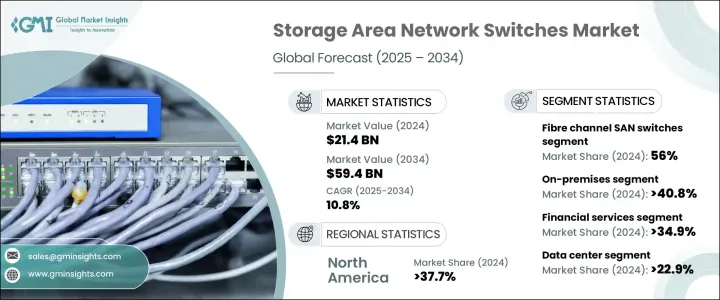

2024 年全球儲存區域網路交換器市場規模達到 214 億美元,預計 2025 年至 2034 年的複合年成長率為 10.8%。這一成長得益於全球高速 5G 網路的部署、高速光纖的廣泛採用以及資料中心和雲端運算日益成長的重要性。這些進步正在推動企業從傳統的 SAN 儲存系統轉向更複雜、高連接埠密度的交換互連。因此,SAN 交換器現在被認為是現代基礎架構的必需品,它提供可擴展的儲存解決方案,確保跨多個雲端平台的無縫資料移動。

SAN 交換器市場主要分為兩種:光纖通道 SAN 交換器和乙太網路SAN 交換器。 2024年,光纖通道SAN交換機將佔據市場主導地位,佔有56%的佔有率,預計成長速度最快,複合年成長率為12%。光纖通道 SAN 交換器越來越受到高效能環境的青睞,尤其是在需要低延遲和可靠儲存解決方案的行業,例如醫療保健和金融。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 214億美元 |

| 預測值 | 594億美元 |

| 複合年成長率 | 10.8% |

根據部署類型,市場分為內部部署、基於雲端和混合模型。 2024 年,內部部署部分將佔據最大的市場佔有率,超過 40.8%,而基於雲端的 SAN 交換器是成長最快的部分,預計複合年成長率為 12.4%。 2024 年本地儲存市場價值為 87 億美元,預計該市場將保持穩定成長,因為醫療保健和國防等產業的合規性規定非常嚴格,而安全、高效能的儲存對這些產業至關重要。

就應用而言,SAN 交換器市場分為資料儲存和備份、虛擬化、資料中心、企業網路、雲端運算等。資料中心佔據最大的市場佔有率,到2024年將占到總量的22.9%,預計成長最快,複合年成長率為12.6%。這一趨勢與超大規模資料中心對儲存解決方案不斷成長的需求有關,而這種需求是由對高效能和節能系統的需求所驅動的。

對於終端使用產業,金融服務引領市場,到 2024 年將佔總市場佔有率的 34.9%,預計成長最快,複合年成長率為 12.2%。隨著金融機構越來越依賴 SAN 交換器執行高頻交易和即時資料處理等任務,對這些技術的需求預計會持續上升。

從地理上看,北美是 SAN 交換器最大的市場,到 2024 年將佔全球佔有率的 37.7%。同時,受快速數位轉型的推動,亞太地區正經歷最快的成長,預計複合年成長率為 12.2%。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商矩陣

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 產業衝擊力

- 成長動力

- 5G和光纖網路的擴展

- 汽車LiDAR整合

- 醫學影像需求不斷成長

- 工業自動化與智慧製造

- 資料中心和雲端運算服務的擴展。

- 產業陷阱與挑戰

- 高資本支出

- 技術快速淘汰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 監管格局

第4章:市場估計與預測:依類型,2021 年至 2034 年

- 主要趨勢

- 光纖通道 SAN 交換機

- 4 Gbps

- 8 Gbps

- 16 Gbps

- 32 Gbps

- 乙太網路SAN 交換機

- 1 GbE

- 10 GbE

- 25 GbE

- 40 Gb以太網

- 100 GbE

第5章:市場估計與預測:依部署類型 2021 – 2034

- 主要趨勢

- 本地

- 雲

- 混合

第6章:市場估計與預測:按應用 2021 年至 2034 年

- 主要趨勢

- 資料儲存和備份

- 虛擬化

- 資料中心

- 企業網路

- 雲端運算

- 其他

第7章:市場估計與預測:依最終用途產業 2021 年至 2034 年

- 主要趨勢

- 金融服務

- 電信

- 政府

- 媒體和娛樂

- 航空

- 其他

第8章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 日本

- 中國

- 印度

- 韓國

- 澳新銀行

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 中東和非洲其他地區

第9章:公司簡介

- Arista Networks, Inc.

- ATTO Technology, Inc.

- Brocade Communications Systems, Inc.

- Cisco Systems, Inc.

- Dell Technologies Inc.

- Extreme Networks, Inc.

- Fortinet, Inc.

- Fujitsu Limited

- Hewlett Packard Enterprise (HPE) Development LP

- Huawei Technologies Co., Ltd.

- IBM Corporation

- Juniper Networks, Inc.

- Lenovo Group Limited

- NEC Corporation

- QLogic Corporation (part of Marvell Technology Group)

The Global Storage Area Network Switches Market reached USD 21.4 billion in 2024 and is expected to grow at a CAGR of 10.8% from 2025 to 2034. This growth is driven by the global rollout of high-speed 5G networks, widespread adoption of high-speed fiber optics, and the growing importance of data centers and cloud computing. These advancements are pushing organizations to move from traditional SAN storage systems to more sophisticated, high-port-density switching interconnects. As a result, SAN switches are now considered essential for modern infrastructures, providing scalable storage solutions that ensure seamless data mobility across multiple cloud platforms.

The market for SAN switches is divided into two primary types: fiber channel SAN switches and Ethernet SAN switches. In 2024, fiber channel SAN switches dominate the market, holding a share of 56%, and are expected to grow at the fastest rate, with a CAGR of 12%. Fiber channel SAN switches are increasingly preferred for high-performance environments, particularly in sectors that require low-latency and reliable storage solutions, such as healthcare and finance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.4 Billion |

| Forecast Value | $59.4 Billion |

| CAGR | 10.8% |

By deployment type, the market is segmented into on-premises, cloud-based, and hybrid models. In 2024, the on-premises segment holds the largest market share at over 40.8%, while cloud-based SAN switches are the fastest-growing segment, expected to grow at a CAGR of 12.4%. The on-premises market is valued at USD 8.7 billion in 2024 and is projected to maintain steady growth due to strict compliance regulations in industries such as healthcare and defense, where secure, high-performance storage is critical.

In terms of application, the SAN switches market is categorized into data storage and backup, virtualization, data centers, enterprise networking, cloud computing, and others. Data centers hold the largest market share, accounting for 22.9% of the total in 2024, and are expected to see the fastest growth with a CAGR of 12.6%. This trend is linked to the expanding demand for storage solutions in hyperscale data centers, driven by the need for high-performance and energy-efficient systems.

For end-use industries, financial services lead the market, making up 34.9% of the total market share in 2024, with the fastest growth projected at a CAGR of 12.2%. As financial institutions increasingly rely on SAN switches for tasks such as high-frequency trading and real-time data processing, the demand for these technologies is expected to continue rising.

Geographically, North America is the largest market for SAN switches, accounting for 37.7% of the global share in 2024. Meanwhile, the Asia-Pacific region is experiencing the fastest growth, with a projected CAGR of 12.2%, fueled by the region's rapid digital transformation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of 5G and fiber networks

- 3.7.1.2 Automotive LiDAR integration

- 3.7.1.3 Increasing demand for medical imaging

- 3.7.1.4 Industrial automation and smart manufacturing

- 3.7.1.5 Expansion of data centers and cloud computing services.

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High capital expenditure

- 3.7.2.2 Rapid technological obsolescence

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Bn)

- 4.1 Key trends

- 4.2 Fibre channel SAN switches

- 4.2.1 4 Gbps

- 4.2.2 8 Gbps

- 4.2.3 16 Gbps

- 4.2.4 32 Gbps

- 4.3 Ethernet SAN switches

- 4.3.1 1 GbE

- 4.3.2 10 GbE

- 4.3.3 25 GbE

- 4.3.4 40 GbE

- 4.3.5 100 GbE

Chapter 5 Market Estimates and Forecast, By Deployment Type 2021 – 2034 (USD Bn)

- 5.1 Key trends

- 5.2 On-premises

- 5.3 Cloud

- 5.4 Hybrid

Chapter 6 Market Estimates and Forecast, By Application 2021 – 2034 (USD Bn)

- 6.1 Key trends

- 6.2 Data storage and backup

- 6.3 Virtualization

- 6.4 Data centers

- 6.5 Enterprise networking

- 6.6 Cloud computing

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry 2021 – 2034 (USD Bn)

- 7.1 Key trends

- 7.2 Financial services

- 7.3 Telecommunications

- 7.4 Government

- 7.5 Media and entertainment

- 7.6 Aviation

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021– 2034 ($ Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 The U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 UAE

- 8.6.3 Saudi Arabia

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Arista Networks, Inc.

- 9.2 ATTO Technology, Inc.

- 9.3 Brocade Communications Systems, Inc.

- 9.4 Cisco Systems, Inc.

- 9.5 Dell Technologies Inc.

- 9.6 Extreme Networks, Inc.

- 9.7 Fortinet, Inc.

- 9.8 Fujitsu Limited

- 9.9 Hewlett Packard Enterprise (HPE) Development LP

- 9.10 Huawei Technologies Co., Ltd.

- 9.11 IBM Corporation

- 9.12 Juniper Networks, Inc.

- 9.13 Lenovo Group Limited

- 9.14 NEC Corporation

- 9.15 QLogic Corporation (part of Marvell Technology Group)

2026年全球伺服器儲存區域網路網路市場報告2026年全球儲存區域網路(SAN)解決方案市場報告

2026年全球伺服器儲存區域網路網路市場報告2026年全球儲存區域網路(SAN)解決方案市場報告 伺服器儲存區域網路市場:依儲存技術、部署模式和最終用戶產業分類-2026-2032年全球市場預測2026年全球儲存區域網路市場報告

伺服器儲存區域網路市場:依儲存技術、部署模式和最終用戶產業分類-2026-2032年全球市場預測2026年全球儲存區域網路市場報告 儲存區域網路市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署類型、最終用戶、解決方案和安裝類型分類

儲存區域網路市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署類型、最終用戶、解決方案和安裝類型分類 伺服器儲存區域網路市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、類型、組織、地區和競爭對手分類,2021-2031 年

伺服器儲存區域網路市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、類型、組織、地區和競爭對手分類,2021-2031 年 控制器區域網路 (CAN):全球市場佔有率和排名、總收入和需求預測 (2025-2031)

控制器區域網路 (CAN):全球市場佔有率和排名、總收入和需求預測 (2025-2031) 全球控制器區域網路(CAN)收發器市場

全球控制器區域網路(CAN)收發器市場 儲存區域網路市場規模、佔有率和趨勢分析報告:按組件、SAN 類型、技術、組織規模、最終用途、地區和細分市場預測,2025 年至 2033 年

儲存區域網路市場規模、佔有率和趨勢分析報告:按組件、SAN 類型、技術、組織規模、最終用途、地區和細分市場預測,2025 年至 2033 年 儲存區域網路(SAN) 市場:按組件、按 SAN 類型、按技術、按最終用戶、垂直行業和按地區

儲存區域網路(SAN) 市場:按組件、按 SAN 類型、按技術、按最終用戶、垂直行業和按地區