|

市場調查報告書

商品編碼

1716672

失禁護理市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Continence Care Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

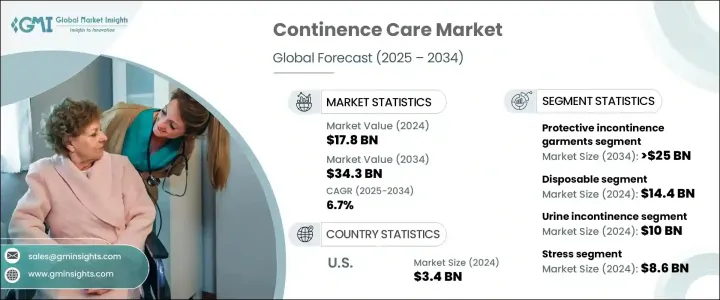

2024 年全球失禁護理市場價值為 178 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.7%。尿失禁、膀胱問題和相關疾病的盛行率不斷上升,推動著市場成長。隨著全球人口老化,壓力性尿失禁、膀胱過動症 (OAB) 和神經性膀胱問題等疾病變得越來越普遍,導致對失禁護理產品的需求增加。根據世界衛生組織 (WHO) 估計,到 2050 年,將有超過 15 億人年齡在 65 歲或以上,對有效的失禁護理解決方案的需求將持續上升。

醫療保健基礎設施的進步和人們對失禁管理的認知的提高也支持了市場擴張。此外,圍繞失禁的恥辱感正在逐漸減少,導致不同年齡層的人對失禁護理解決方案的接受度更高。產品設計的創新,包括開發謹慎、舒適和控制氣味的服裝,進一步鼓勵人們尋求適當的節制護理解決方案。電子商務平台在提高產品可及性方面發揮了關鍵作用,使消費者能夠探索各種各樣的失禁護理產品並選擇最能滿足他們需求的產品。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 178億美元 |

| 預測值 | 343億美元 |

| 複合年成長率 | 6.7% |

失禁護理市場由各種產品類別組成,包括吸收物品、外部設備和間歇性導管。向家庭護理和自我管理醫療保健的轉變正在影響人們對非侵入性失禁護理設備的日益成長的偏好。消費者擴大選擇謹慎且易於使用的解決方案,以便他們能夠私密有效地管理失禁。新興地區醫療保健投資的增加進一步擴大了失禁護理解決方案的覆蓋範圍,確保發展中國家的個人能夠獲得這些必需產品。此外,提供即時警報的基於感測器的失禁設備等技術進步正在透過提供增強的用戶體驗和更好的護理來重塑市場。

在主要產品類別中,防護失禁服裝預計將顯著成長。預計該領域的複合年成長率為 6.8%,到 2034 年將達到 250 億美元。這些服裝旨在處理尿失禁和大便失禁,具有高吸收性、氣味控制和卓越的舒適性。由於其多功能性和有效性,它們被醫院、療養院和家庭護理機構廣泛採用,成為失禁護理市場不可或缺的一部分。

市場進一步分為一次性產品和可重複使用產品,其中一次性產品佔據主導地位。 2024 年,一次性產品的收入為 144 億美元,這主要歸功於其便利性和易用性。這些產品無需清洗和維護,非常適合老年人和以感染控制為首要任務的臨床環境中的人員。它們的實用性和效率使其成為家庭護理環境中管理失禁的首選,為市場成長做出了重大貢獻。

2024 年,美國失禁護理市場價值為 34 億美元,這得益於患有失禁問題以及肥胖和前列腺疾病等其他健康問題的老年人數量的增加。對創新、易於管理的產品(包括超吸收材料和智慧失禁設備)的需求不斷成長,正在推動市場成長。這些產品在零售店和網路商店的供應量不斷增加,使得消費者更容易購買到它們,從而鼓勵了更廣泛的採用,並增強了市場的積極前景。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 泌尿系統疾病盛行率不斷上升

- 政府的支持性報銷政策

- 慢性病發生率上升,人口老化加劇

- 最近的技術進步和新產品開發

- 產業陷阱與挑戰

- 社會恥辱和患者不情願

- 產品相關的併發症和副作用

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 報銷場景

- 消費者行為分析

- 差距分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 保護性失禁服裝

- 一次防護內衣

- 一次性成人尿布

- 成人布尿布

- 一次性護墊和襯墊

- 男警衛

- 膀胱控制墊

- 失禁襯墊

- 有腰帶和不帶腰帶的內衣

- 免洗護墊

- 導尿管

- 留置導尿管

- 間歇導尿管

- 外部導管

- 失禁子宮托

- 環形子宮托

- GellHorn陰道栓劑

- 其他子宮托

- 失禁吊帶與網片

- 女性失禁吊帶與網片

- 男性失禁吊帶與網片

- 失禁引流袋

- 神經刺激

- 薦神經刺激

- 電神經刺激

- 尿袋

- 腿尿袋

- 床邊尿袋

- 失禁夾

- 人工括約肌

- 人工尿道括約肌

- 人工腸括約肌

第6章:市場估計與預測:按可用性,2021 年至 2034 年

- 主要趨勢

- 一次性的

- 可重複使用的

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 尿失禁

- 大便失禁

- 雙重失禁

第 8 章:市場估計與預測:按失禁類型,2021 年至 2034 年

- 主要趨勢

- 壓力

- 混合

- 敦促

- 其他失禁類型

第9章:市場估計與預測:依疾病,2021 年至 2034 年

- 主要趨勢

- 女性健康

- 懷孕和分娩

- 停經

- 子宮切除術

- 其他女性健康疾病

- 慢性疾病

- 精神障礙

- 良性攝護腺增生

- 膀胱癌

- 其他疾病

第 10 章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 超級吸收劑

- 棉織物

- 塑膠

- 乳膠

- 其他材料

第 11 章:市場估計與預測:按性別,2021 年至 2034 年

- 主要趨勢

- 女性

- 男性

第 12 章:市場估計與預測:依年齡,2021 年至 2034 年

- 主要趨勢

- 40至59歲

- 60至79歲

- 20至39歲

- 80多年

- 20歲以下

第 13 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 零售店

- 電子商務

第 14 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 護理設施

- 長期照護中心

- 門診手術中心

- 其他最終用途

第 15 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 16 章:公司簡介

- ABENA

- Attends Healthcare

- B. Braun

- BD

- CardinalHealth

- Coloplast

- ConvaTec

- Essity

- First Quality

- Fu Burg

- Hollister

- Kimberly-Clark

- Medline

- MRK Healthcare

- Ontex

- Paul Hartmann

- Principle Business

- Unicharm

- Urocare

The Global Continence Care Market was valued at USD 17.8 billion in 2024 and is anticipated to grow at a CAGR of 6.7% between 2025 and 2034. The rising prevalence of urinary incontinence, bladder issues, and related disorders is driving market growth. As the global population continues to age, conditions such as stress incontinence, Overactive Bladder (OAB), and neurogenic bladder problems are becoming more widespread, contributing to an increased demand for continence care products. With the World Health Organization (WHO) estimating that by 2050, over 1.5 billion people will be aged 65 or older, the need for effective continence care solutions will continue to rise.

Advances in healthcare infrastructure and increasing awareness about incontinence management are also supporting market expansion. Additionally, the stigma surrounding incontinence is gradually diminishing, leading to higher acceptance of continence care solutions across diverse age groups. Innovations in product design, including the development of discreet, comfortable, and odor-controlling garments, have further encouraged individuals to seek appropriate continence care solutions. E-commerce platforms have played a pivotal role in improving product accessibility, enabling consumers to explore a wide range of continence care products and select those that best meet their needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.8 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 6.7% |

The continence care market is composed of various product categories, including absorbent items, external devices, and intermittent catheters. The shift toward home care and self-managed healthcare is influencing the growing preference for non-invasive continence care devices. Consumers are increasingly opting for discreet and easy-to-use solutions that allow them to manage incontinence privately and effectively. Increased healthcare investments in emerging regions have further expanded the reach of continence care solutions, ensuring that individuals in developing countries can access these essential products. Moreover, technological advancements, such as sensor-based incontinence devices that provide real-time alerts, are reshaping the market by offering enhanced user experience and improved care.

Among the key product categories, protective incontinence garments are expected to witness notable growth. This segment is projected to grow at a CAGR of 6.8%, reaching USD 25 billion by 2034. These garments are designed to handle both urinary and fecal incontinence, offering high absorption, odor control, and superior comfort. They are widely adopted in hospitals, nursing homes, and home care settings due to their versatility and effectiveness, making them an integral part of the continence care market.

The market is further divided into disposable and reusable products, with disposable products dominating the segment. Disposable products generated USD 14.4 billion in 2024, largely due to their convenience and ease of use. These products eliminate the need for washing and maintenance, making them ideal for elderly individuals and those in clinical settings where infection control is a top priority. Their practicality and efficiency have made them a preferred choice for managing incontinence in home care settings, contributing significantly to market growth.

The U.S. continence care market was valued at USD 3.4 billion in 2024, driven by the rising number of older adults experiencing incontinence issues and other health conditions such as obesity and prostate ailments. The growing demand for innovative, easy-to-manage products, including super-absorbent materials and smart incontinence devices, is boosting market growth. The increased availability of these products in both retail and online stores has made them more accessible to consumers, encouraging greater adoption and reinforcing the market's positive outlook.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of urologic disorders

- 3.2.1.2 Supportive reimbursement policies by governments

- 3.2.1.3 Increasing incidence of chronic diseases coupled with rising aging population

- 3.2.1.4 Recent technological advancements and new product developments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Social stigma and patient reluctance

- 3.2.2.2 Product-related complications and side effects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Consumer behaviour analysis

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Protective incontinence garments

- 5.2.1 Disposable protective underwears

- 5.2.2 Disposable adult diapers

- 5.2.3 Cloth adult diapers

- 5.2.4 Disposable pads and liners

- 5.2.4.1 Male guards

- 5.2.4.2 Bladder control pads

- 5.2.4.3 Incontinence liners

- 5.2.4.3.1 Belted and beltless under garments

- 5.2.4.3.2 Disposable under pads

- 5.3 Urinary catheters

- 5.3.1 Indwelling (foley) catheters

- 5.3.2 Intermittent catheter

- 5.3.3 External catheters

- 5.4 Incontinence pessaries

- 5.4.1 Ring pessaries

- 5.4.2 GellHorn pessaries

- 5.4.3 Other pessaries

- 5.5 Incontinence slings and meshes

- 5.5.1 Female incontinence slings and meshes

- 5.5.2 Male incontinence slings and meshes

- 5.6 Incontinence drainage bags

- 5.7 Nerve stimulation

- 5.7.1 Sacral nerve stimulation

- 5.7.2 Electrical nerve stimulation

- 5.8 Urine bags

- 5.8.1 Leg urine bags

- 5.8.2 Bedside urine bags

- 5.9 Incontinence clamps

- 5.10 Artificial sphincters

- 5.10.1 Artificial urinary sphincters

- 5.10.2 Artificial bowel sphincters

Chapter 6 Market Estimates and Forecast, By Usability, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Disposable

- 6.3 Reusable

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Urine incontinence

- 7.3 Fecal incontinence

- 7.4 Dual incontinence

Chapter 8 Market Estimates and Forecast, By Incontinence Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Stress

- 8.3 Mixed

- 8.4 Urge

- 8.5 Other incontinence types

Chapter 9 Market Estimates and Forecast, By Disease, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Feminine health

- 9.2.1 Pregnancy and childbirth

- 9.2.2 Menopause

- 9.2.3 Hysterectomy

- 9.2.4 Other feminine health diseases

- 9.3 Chronic diseases

- 9.4 Mental disorders

- 9.5 Benign prostatic hyperplasia

- 9.6 Bladder cancer

- 9.7 Other diseases

Chapter 10 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Super absorbents

- 10.3 Cotton fabrics

- 10.4 Plastic

- 10.5 Latex

- 10.6 Other materials

Chapter 11 Market Estimates and Forecast, By Gender, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 Female

- 11.3 Male

Chapter 12 Market Estimates and Forecast, By Age, 2021 – 2034 ($ Mn)

- 12.1 Key trends

- 12.2 40 to 59 years

- 12.3 60 to 79 years

- 12.4 20 to 39 years

- 12.5 80+ years

- 12.6 Below 20 years

Chapter 13 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 13.1 Key trends

- 13.2 Retail stores

- 13.3 E-commerce

Chapter 14 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 14.1 Key trends

- 14.2 Hospitals

- 14.3 Nursing facilities

- 14.4 Long term care centers

- 14.5 Ambulatory surgical centers

- 14.6 Other end use

Chapter 15 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 15.1 Key trends

- 15.2 North America

- 15.2.1 U.S.

- 15.2.2 Canada

- 15.3 Europe

- 15.3.1 Germany

- 15.3.2 UK

- 15.3.3 France

- 15.3.4 Spain

- 15.3.5 Italy

- 15.3.6 Netherlands

- 15.4 Asia Pacific

- 15.4.1 China

- 15.4.2 Japan

- 15.4.3 India

- 15.4.4 Australia

- 15.4.5 South Korea

- 15.5 Latin America

- 15.5.1 Brazil

- 15.5.2 Mexico

- 15.5.3 Argentina

- 15.6 Middle East and Africa

- 15.6.1 South Africa

- 15.6.2 Saudi Arabia

- 15.6.3 UAE

Chapter 16 Company Profiles

- 16.1 ABENA

- 16.2 Attends Healthcare

- 16.3 B. Braun

- 16.4 BD

- 16.5 CardinalHealth

- 16.6 Coloplast

- 16.7 ConvaTec

- 16.8 Essity

- 16.9 First Quality

- 16.10 Fu Burg

- 16.11 Hollister

- 16.12 Kimberly-Clark

- 16.13 Medline

- 16.14 MRK Healthcare

- 16.15 Ontex

- 16.16 Paul Hartmann

- 16.17 Principle Business

- 16.18 Unicharm

- 16.19 Urocare

2026年全球一次性失禁用品市場報告

2026年全球一次性失禁用品市場報告 成人尿墊市場-2026-2031年預測

成人尿墊市場-2026-2031年預測 腎臟病和泌尿系統失禁器械市場:按器械類型、最終用戶、材料類型、分銷管道、年齡層和性別分類的全球預測,2026-2032年

腎臟病和泌尿系統失禁器械市場:按器械類型、最終用戶、材料類型、分銷管道、年齡層和性別分類的全球預測,2026-2032年 一次性失禁用品市場規模、佔有率和成長分析(按產品、應用、失禁類型、疾病、材料、性別和地區分類)-2026-2033年產業預測2025年全球失禁護理市場報告

一次性失禁用品市場規模、佔有率和成長分析(按產品、應用、失禁類型、疾病、材料、性別和地區分類)-2026-2033年產業預測2025年全球失禁護理市場報告 一次性失禁產品市場按產品類型、材料、分銷管道和地區分類

一次性失禁產品市場按產品類型、材料、分銷管道和地區分類 一次性失禁產品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

一次性失禁產品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 一次性失禁產品市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、地區和競爭細分,2020-2030 年)

一次性失禁產品市場-全球產業規模、佔有率、趨勢、機會和預測(按產品類型、應用、地區和競爭細分,2020-2030 年) 一次性失禁產品市場報告:趨勢、預測和競爭分析(至 2031 年)

一次性失禁產品市場報告:趨勢、預測和競爭分析(至 2031 年) 全球可重複使用失禁產品市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)

全球可重複使用失禁產品市場:產業分析、規模、佔有率、成長、趨勢和預測(2025-2032 年)