|

市場調查報告書

商品編碼

1716636

公車調度管理系統軟體市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Bus Dispatch Management System Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

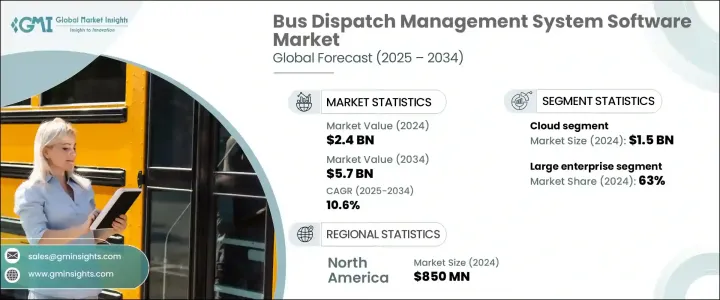

2024 年全球公車調度管理系統軟體市場價值為 24 億美元,預估 2025 年至 2034 年的複合年成長率為 10.6%。受公共交通技術投資增加和對高效車隊管理解決方案的需求不斷成長的推動,該市場正在快速擴張。隨著城市人口的不斷成長,交通運輸機構和運輸提供商正在轉向先進的軟體解決方案,以最佳化公車營運、提高調度準確性並簡化整體車隊監控。隨著世界各地的城市優先考慮更智慧、更永續的行動解決方案,向數位化公共交通基礎設施的轉變進一步加速了需求。

隨著城市化進程的加快,對結構良好、可靠的公共交通網路的需求變得至關重要。城市人口激增導致道路擁擠加劇、通勤量增加,需要採用智慧公車調度管理系統。這些先進的平台可實現即時監控、自動調度和人工智慧路線最佳化,確保車隊平穩運作並提升通勤體驗。政府和私人交通機構正在積極投資這些技術,以減少延誤、提高燃油效率並降低營運成本。此外,對綠色環保交通解決方案的日益追求也導致對整合電動和混合動力汽車管理的公車調度軟體的需求增加。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 24億美元 |

| 預測值 | 57億美元 |

| 複合年成長率 | 10.6% |

市場主要根據部署模型進行細分,其中基於雲端的解決方案和內部部署的解決方案是兩大類別。基於雲端的解決方案佔據了該領域的主導地位,2024 年創造了 15 億美元的收入,預計 2025 年至 2034 年期間的複合年成長率將達到 11%。基於雲端的調度管理軟體提供了無與倫比的可擴展性,使運輸機構能夠無縫管理車隊營運,無論車隊規模大小。這些解決方案還支援遠端訪問,使車隊經理和調度員能夠從任何具有網際網路連接的地方監控即時操作。基於雲端的平台的靈活性和成本效益已被廣泛採用,特別是在尋求強大且面向未來的解決方案的運輸機構中。

依企業規模分析市場時,大型企業佔據主導地位,2024年將佔63%的市場。公共交通管理部門和擁有大量預算的跨國公車業者繼續投資於複雜的公車調度管理軟體。這些先進的系統為大型組織提供即時追蹤、預測分析和人工智慧驅動的最佳化工具,從而提高車隊性能並減少停機時間。隨著企業尋求提高乘客安全、營運效率和成本管理,大規模交通營運對自動化的需求不斷成長,進一步推動了市場擴張。

北美佔據公車調度管理系統軟體市場的 35% 佔有率,2024 年市場規模達 8.5 億美元。該地區強大的市場影響力歸功於智慧移動解決方案的日益普及以及人工智慧、物聯網和雲端運算在交通營運中的整合。隨著交通運輸機構不斷更新其車隊管理策略,對先進公車調度軟體的需求預計將激增,從而進一步推動未來幾年的市場成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 軟體開發商/供應商

- 硬體提供者

- 系統整合商

- 電信公司

- 交通運輸機構/營運商

- 利潤率分析

- 價格趨勢

- 技術與創新格局

- 專利分析

- 案例研究

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 對高效公共交通的需求不斷增加

- 都市化和人口成長

- 增加對公共交通技術的投資

- 汽車感測器技術日益發展

- 產業陷阱與挑戰

- 網路連線有限和基礎設施限制

- 來自傳統交通運輸機構或利害關係人的抵制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依部署模型,2021 - 2034 年

- 主要趨勢

- 本地

- 雲

第6章:市場估計與預測:依企業規模,2021 - 2034 年

- 主要趨勢

- 大型企業

- 中小企業

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 路線最佳化

- 即時追蹤

- 車隊管理

- 調度與通訊

- 其他

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 大眾運輸機構

- 私營巴士營運商

- 教育機構

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第10章:公司簡介

- BusHive

- Cubic Transportation Systems

- Driver Schedule

- GIRO

- Goal Systems

- GPS Insight

- Hudson Software

- IBI Group

- INIT Innovations in Transportation

- Optibus

- Reveal Management Services

- Ride Systems

- Routematch Software

- Samsara Networks

- Syncromatics

- TransLoc

- Trapeze Group

- TripSpark Technologies

- Verizon Connect Reveal

- Zonar Systems

The Global Bus Dispatch Management System Software Market was valued at USD 2.4 billion in 2024 and is projected to grow at a CAGR of 10.6% from 2025 to 2034. The market is experiencing rapid expansion, driven by increasing investments in public transport technology and the rising need for efficient fleet management solutions. With urban populations continuing to grow, transit agencies and transportation providers are turning to advanced software solutions that optimize bus operations, enhance scheduling accuracy, and streamline overall fleet monitoring. The shift toward digitized public transportation infrastructure is further accelerating demand as cities worldwide prioritize smarter, more sustainable mobility solutions.

As urbanization intensifies, the need for well-structured and reliable public transportation networks becomes critical. The surge in urban population results in increased road congestion and higher commuter volumes, necessitating the adoption of intelligent bus dispatch management systems. These advanced platforms enable real-time monitoring, automated scheduling, and AI-powered route optimization, ensuring smooth fleet operations and enhanced commuter experience. Governments and private transit agencies are actively investing in these technologies to reduce delays, improve fuel efficiency, and minimize operational costs. Additionally, the growing push for green and eco-friendly transit solutions is leading to an increased demand for bus dispatch software that integrates electric and hybrid vehicle management.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 10.6% |

The market is primarily segmented based on deployment models, with cloud-based and on-premises solutions being the two major categories. Cloud-based solutions dominated the segment, generating USD 1.5 billion in 2024, and are expected to grow at a CAGR of 11% between 2025 and 2034. Cloud-based dispatch management software offers unparalleled scalability, allowing transportation agencies to seamlessly manage fleet operations regardless of size. These solutions also enable remote access, giving fleet managers and dispatchers the ability to monitor real-time operations from any location with internet connectivity. The flexibility and cost-effectiveness of cloud-based platforms have led to widespread adoption, particularly among transit agencies looking for robust and future-ready solutions.

When analyzing the market by enterprise size, large enterprises held a dominant position, accounting for 63% of the market share in 2024. Public transportation authorities and multinational bus operators with substantial budgets continue to invest in sophisticated bus dispatch management software. These advanced systems empower large organizations with real-time tracking, predictive analytics, and AI-driven optimization tools that enhance fleet performance and reduce downtime. The rising need for automation in large-scale transit operations further fuels market expansion as enterprises seek to improve passenger safety, operational efficiency, and cost management.

North America led the bus dispatch management system software market with a 35% share, generating USD 850 million in 2024. The region's strong market presence is attributed to the growing adoption of smart mobility solutions and the integration of AI, IoT, and cloud computing in transit operations. As transportation agencies continue to modernize their fleet management strategies, demand for advanced bus dispatch software is expected to surge, further driving market growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software developers/vendors

- 3.2.2 Hardware providers

- 3.2.3 System integrators

- 3.2.4 Telecommunications companies

- 3.2.5 Transit agencies/operators

- 3.3 Profit margin analysis

- 3.4 Price trends

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Case study

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for efficient public transportation

- 3.10.1.2 Growing urbanization and population growth

- 3.10.1.3 Increasing investments in public transport technology

- 3.10.1.4 Rising growth of automotive sensor technology

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Limited internet connectivity and infrastructure limitations

- 3.10.2.2 Resistance from traditional transit agencies or stakeholders

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 On-premises

- 5.3 Cloud

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Large enterprises

- 6.3 SME

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Route optimization

- 7.3 Real-time tracking

- 7.4 Fleet management

- 7.5 Dispatch and communication

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Public transit agencies

- 8.3 Private bus operators

- 8.4 Educational institutions

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 BusHive

- 10.2 Cubic Transportation Systems

- 10.3 Driver Schedule

- 10.4 GIRO

- 10.5 Goal Systems

- 10.6 GPS Insight

- 10.7 Hudson Software

- 10.8 IBI Group

- 10.9 INIT Innovations in Transportation

- 10.10 Optibus

- 10.11 Reveal Management Services

- 10.12 Ride Systems

- 10.13 Routematch Software

- 10.14 Samsara Networks

- 10.15 Syncromatics

- 10.16 TransLoc

- 10.17 Trapeze Group

- 10.18 TripSpark Technologies

- 10.19 Verizon Connect Reveal

- 10.20 Zonar Systems