|

市場調查報告書

商品編碼

1716596

聚酯纖維市場機會、成長動力、產業趨勢分析及2025-2034年預測Polyester Fiber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

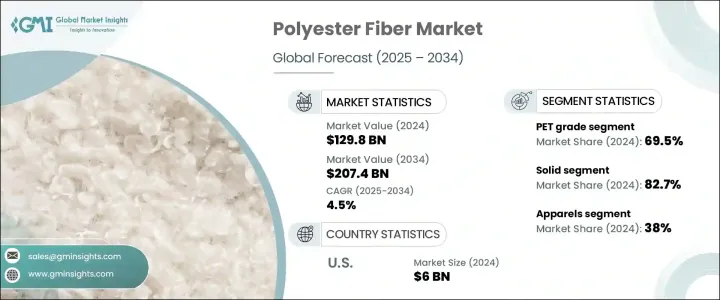

2024 年全球聚酯纖維市場價值為 1,298 億美元,預計 2025 年至 2034 年的複合年成長率為 4.5%。由石化產品合成的聚酯纖維仍然是全球用途最廣泛、使用最廣泛的合成纖維之一,這主要歸功於其強度、耐用性、靈活性和成本效益。隨著各行各業不斷尋求具有增強功能性和永續性的高性能材料,聚酯纖維成為紡織、汽車、家居裝飾和工業應用等多個垂直領域的頂級競爭者。時尚和家居裝飾領域對低維護、抗皺和快乾布料的需求不斷成長,加速了聚酯纖維的使用。

此外,環保和再生纖維製造等生產技術的不斷創新正在推動全球市場向前發展。消費者對永續和耐用材料的認知不斷提高,加上對天然纖維的經濟實惠的合成替代品的需求不斷增加,增強了聚酯纖維的主導地位。此外,全球市場參與者正專注於策略合作、合併和收購,以加強其生產能力和產品組合,進一步推動市場擴張。向循環經濟的轉變以及紡織品中再生聚酯的不斷增加也在塑造該行業的成長軌跡。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 1298億美元 |

| 預測值 | 2074億美元 |

| 複合年成長率 | 4.5% |

聚酯纖維市場依等級分為 PET(聚對苯二甲酸乙二醇酯)和 PCDT(聚-1,4-環己基-二亞甲基對苯二甲酸酯)。 2024 年,PET 級佔據市場主導地位,佔有 69.5% 的佔有率,這主要是因為它廣泛應用於服裝、包裝和工業用布。 PET 纖維以其耐用性、輕質性以及出色的耐濕性和耐化學性而聞名,在時尚和工業應用領域中受到青睞。消費者對環保產品的日益關注推動了對 PET 纖維的需求,因為它們可以回收製成新材料,從而有效地支持永續發展目標。由於消費者優先考慮耐用、低維護且具有價值和性能的服裝和產品,PET 纖維仍然是尋求滿足不斷變化的市場需求的製造商的首選。

根據產品類型,聚酯纖維市場分為實心纖維和空心纖維,其中實心聚酯纖維在 2024 年佔據 82.7% 的佔有率。實心纖維因其在服裝、床上用品、室內裝潢和其他需要強度、耐用性和易於護理的紡織產品中的廣泛應用而繼續受到關注。家庭和商業領域對抗皺、快乾和有彈性的布料的偏好日益成長,推動了對固體聚酯纖維的需求增加。此外,家居裝飾和室內陳設的趨勢強調美觀和功能性,也促進了這一領域的成長。消費者和製造商都認為固體聚酯纖維是一種適用於各種應用的經濟高效且高品質的解決方案,使其成為現代紡織品不可或缺的組成部分。

美國聚酯纖維市場價值預計在 2024 年達到 60 億美元,在強勁的工業需求、先進的製造能力和有利的貿易政策的推動下,將繼續保持領先地位。發達的紡織業和對國內製造業的日益重視正在鞏固中國在全球聚酯纖維領域的地位。合成纖維(尤其是聚酯纖維)進口量的增加,凸顯了美國各地時尚、家紡和工業用途對這些多功能材料的需求不斷成長

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商格局

- 利潤率分析

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 併購

- 生產流程的技術進步

- 汽車和工業應用的成長

- 產業陷阱與挑戰

- 環境法規

- 來自替代纖維的競爭

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依等級,2021-2034 年

- 主要趨勢

- 寵物

- 聚二甲基二烯丙基氯化銨

第6章:市場估計與預測:按產品,2021-2034 年

- 主要趨勢

- 堅硬的

- 空洞的

第7章:市場估計與預測:按應用,2021-2034 年

- 主要趨勢

- 地毯和地墊

- 不非織物纖維

- 纖維填充

- 服飾

- 家紡

- 其他

第8章:市場估計與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Alpek Polyester

- Far Eastern Group

- GreenFiber International

- Indorama Ventures

- Nan Ya Plastics Corporation

- Reliance Industries Limited

- Sinopec

- Stein Fibers

- Swicofil

- Teijin Limited

- Toray Industries

- William Barnet and Son

- Zhejiang Hengsheng Chemical Fiber Group

The Global Polyester Fiber Market, valued at USD 129.8 billion in 2024, is projected to grow at a CAGR of 4.5% from 2025 to 2034. Polyester fiber, synthesized from petrochemicals, remains one of the most versatile and widely used synthetic fibers worldwide, primarily due to its strength, durability, flexibility, and cost-effectiveness. As industries continuously seek high-performance materials that offer enhanced functionality and sustainability, polyester fiber emerges as a top contender across multiple verticals, including textiles, automotive, home furnishings, and industrial applications. The rising demand for low-maintenance, wrinkle-resistant, and quick-drying fabrics in the fashion and home decor segments is accelerating the use of polyester fibers.

Additionally, ongoing innovations in production technologies, such as eco-friendly and recycled fiber manufacturing, are driving the global market forward. Heightened consumer awareness about sustainable and durable materials, coupled with increasing demand for affordable synthetic alternatives to natural fibers, is reinforcing polyester fiber's dominance. Moreover, global market players are focusing on strategic collaborations, mergers, and acquisitions to strengthen their production capacities and product portfolios, further fueling market expansion. The shift toward circular economies and the rising incorporation of recycled polyester in textiles are also shaping the industry's growth trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $129.8 Billion |

| Forecast Value | $207.4 Billion |

| CAGR | 4.5% |

The polyester fiber market is segmented by grade into PET (polyethylene terephthalate) and PCDT (poly-1,4-cyclohexylene-dimethylene terephthalate). PET grade dominated the market with a 69.5% share in 2024, primarily due to its extensive use in clothing, packaging, and industrial fabrics. Known for its durability, lightweight nature, and excellent resistance to moisture and chemicals, PET fiber continues to be favored in fashion and industrial applications alike. The increasing consumer focus on eco-friendly products is driving the demand for PET fibers since they can be recycled into new materials, effectively supporting sustainability goals. As consumers prioritize long-lasting, low-maintenance garments and products that offer value and performance, PET fibers remain the preferred choice for manufacturers looking to meet evolving market demands.

By product type, the polyester fiber market is divided into solid and hollow fibers, with solid polyester fibers capturing an 82.7% share in 2024. Solid fibers continue gaining traction owing to their widespread use in apparel, bedding, upholstery, and other textile products that require strength, durability, and ease of care. The growing preference for wrinkle-resistant, fast-drying, and resilient fabrics in both home and commercial sectors is pushing the demand for solid polyester fibers higher. Additionally, trends in home decor and interior furnishings that emphasize aesthetic appeal along with functionality are contributing to the growth of this segment. Consumers and manufacturers alike are recognizing solid polyester fibers as a cost-effective and high-quality solution for various applications, making them an indispensable component of modern textiles.

U.S. polyester fiber market, valued at USD 6 billion in 2024, continues to hold a leading position, driven by robust industrial demand, advanced manufacturing capabilities, and favorable trade policies. The well-developed textile industry and growing emphasis on domestic manufacturing are reinforcing the country's stronghold in the global polyester fiber space. Increasing imports of synthetic fibers, especially polyester, highlight the rising need for these versatile materials in fashion, home textiles, and industrial uses across the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Merger and acquisitions

- 3.6.1.2 Technological advancements in production process

- 3.6.1.3 Growth in automotive and industrial applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental regulations

- 3.6.2.2 Competition from alternative fibers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Grade, 2021–2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 PET

- 5.3 PCDT

Chapter 6 Market Estimates and Forecast, By Product, 2021–2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Hollow

Chapter 7 Market Estimates and Forecast, By Application, 2021–2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Carpets & rugs

- 7.3 Non-woven fiber

- 7.4 Fiberfill

- 7.5 Apparel

- 7.6 Home textile

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021–2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alpek Polyester

- 9.2 Far Eastern Group

- 9.3 GreenFiber International

- 9.4 Indorama Ventures

- 9.5 Nan Ya Plastics Corporation

- 9.6 Reliance Industries Limited

- 9.7 Sinopec

- 9.8 Stein Fibers

- 9.9 Swicofil

- 9.10 Teijin Limited

- 9.11 Toray Industries

- 9.12 William Barnet and Son

- 9.13 Zhejiang Hengsheng Chemical Fiber Group

聚酯纖維拉繩市場規模、佔有率和成長分析:按基材、塗層類型、丹尼爾/厚度、電纜應用和地區分類-2026-2033年產業預測

聚酯纖維拉繩市場規模、佔有率和成長分析:按基材、塗層類型、丹尼爾/厚度、電纜應用和地區分類-2026-2033年產業預測 聚酯纖維市場:全球市場按產品類型、形態、功能、製造流程和應用進行預測-2026-2032年

聚酯纖維市場:全球市場按產品類型、形態、功能、製造流程和應用進行預測-2026-2032年 全球聚酯纖維市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034)

全球聚酯纖維市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034) 2032 年聚酯纖維市場預測:按產品類型、等級、形式、原料、應用、最終用戶和地區進行的全球分析

2032 年聚酯纖維市場預測:按產品類型、等級、形式、原料、應用、最終用戶和地區進行的全球分析 聚酯纖維市場報告:趨勢、預測和競爭分析(至2031年)

聚酯纖維市場報告:趨勢、預測和競爭分析(至2031年) 聚酯纖維市場規模、佔有率和成長分析(按產品類型、等級、幾何形狀、自動化程度和地區)- 2025-2032 年產業預測全球聚酯纖維市場預測(2025-2030)聚酯纖維市場:按成分、按部署模式、按技術、按組織規模、按最終用戶、按地區,2024-2031

聚酯纖維市場規模、佔有率和成長分析(按產品類型、等級、幾何形狀、自動化程度和地區)- 2025-2032 年產業預測全球聚酯纖維市場預測(2025-2030)聚酯纖維市場:按成分、按部署模式、按技術、按組織規模、按最終用戶、按地區,2024-2031