|

市場調查報告書

商品編碼

1716569

顯示控制器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Display Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

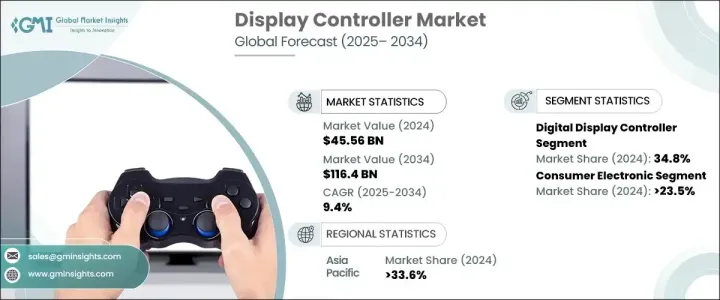

2024 年全球顯示控制器市場價值為 455.6 億美元,預計 2025 年至 2034 年期間的複合年成長率為 9.4%。成長主要得益於醫療保健、消費性電子、遊戲和製造業等各個領域擴大採用先進的顯示技術。隨著技術的不斷發展,各行各業正在整合高效能顯示解決方案,以增強使用者體驗並簡化操作。智慧家庭設備(例如內建顯示器的數位助理)的普及率不斷提高,增加了對緊湊、節能和多功能顯示控制器的需求。

此外,互動式智慧顯示器和觸控介面在商業和住宅環境中的日益普及為該市場增添了動力,鼓勵製造商創新和增強其產品供應。顯示控制器現在對於管理跨裝置的顯示功能、確保無縫視覺效果和提高整體營運效率至關重要。人工智慧 (AI) 和物聯網 (IoT) 的進步導致需要直覺和響應式使用者介面的智慧型裝置中顯示控制器的使用激增。這種技術進步促使製造商專注於設計提供卓越性能、更低延遲和改進電源管理的控制器,以滿足日益成長的沉浸式和動態顯示需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 455.6億美元 |

| 預測值 | 1164億美元 |

| 複合年成長率 | 9.4% |

智慧顯示器產業正在經歷顯著擴張,其市場價值到 2024 年將達到 33 億美元,預計在預測期內的複合年成長率為 11.3%。這種成長很大程度上得益於人工智慧和物聯網功能日益融入智慧家庭生態系統。智慧顯示控制器可以管理介面並最佳化設備效能,正變得越來越普遍,可以實現無縫的用戶互動並增強設備功能。家庭、辦公室和公共場所對智慧顯示器的需求日益成長,迫使公司不斷創新,提供語音控制、手勢識別和個人化用戶體驗等先進功能。

顯示控制器市場按最終用途產業細分,包括航太、汽車、消費性電子、遊戲、醫療保健和工業控制。航太和國防領域預計在 2024 年價值 71 億美元,預測期內複合年成長率將達到 10.6%。這種成長歸因於地緣政治緊張局勢加劇以及全球透過開發先進飛機系統來加強國防的推動。隨著航太技術變得越來越複雜,對可靠和高效能顯示器控制器的需求不斷增加,以確保在關鍵任務環境中高效運作。

2024 年德國顯示控制器市場規模達 24 億美元,預估複合年成長率為 9.9%。這一成長得益於該國的工業 4.0 計劃,該計劃強調透過整合人工智慧和物聯網技術實現製造流程的數位轉型。隨著德國推動智慧工廠和自動化系統,對能夠支援先進製造系統的顯示控制器的需求預計將上升。政府對尖端技術、自動化和工業創新的投資為德國顯示控制器市場的持續成長奠定了堅實的基礎。德國工業領域對現代顯示技術的採用正在提高生產效率並推動市場持續擴張。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商矩陣

- 利潤率分析

- 技術與創新格局

- 專利分析

- 重要新聞和舉措

- 產業衝擊力

- 成長動力

- 高解析度顯示器擴大消費性電子產品的應用

- 高解析度和先進的顯示技術

- 工業自動化和物聯網普及

- 越來越重視節能設備

- 汽車產業對 ADAS 的採用

- 產業陷阱與挑戰

- 研發和製造成本高。

- 與先進顯示技術整合的複雜性

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 監管格局

第4章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- LCD顯示控制器

- 觸控螢幕顯示控制器

- 多重顯示器控制器

- 智慧型顯示控制器

- 數位顯示控制器

- 其他

第5章:市場估計與預測:依最終用途產業 2021 - 2034

- 主要趨勢

- 航太和國防

- 汽車

- 消費性電子產品

- 遊戲和娛樂

- 衛生保健

- 工業控制

- 其他

第6章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 日本

- 中國

- 印度

- 韓國

- 澳新銀行

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 南非

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 中東和非洲其他地區

第7章:公司簡介

- Analog Devices

- Barco

- Broadcom Inc.

- Fujitsu Limited

- Infineon Technologies

- LG Display Co., Ltd.

- Maxim Integrated

- Microchip Technology Inc.

- NXP Semiconductors

- ON Semiconductor

- Qualcomm Technologies, Inc.

- Renesas Electronics

- ROHM Semiconductor

- Samsung Electronics

- STMicroelectronics

- TDK Corporation

- Texas Instruments

- Toshiba Electronic Devices & Storage Corporation

- Xi'an NovaStar Tech Co., Ltd.

The Global Display Controller Market was valued at USD 45.56 billion in 2024 and is projected to grow at a CAGR of 9.4% between 2025 and 2034. The growth is primarily driven by the increasing adoption of advanced display technologies across diverse sectors, including healthcare, consumer electronics, gaming, and manufacturing. As technology continues to evolve, industries are integrating high-performance display solutions to enhance user experiences and streamline operations. The rising penetration of smart home devices, such as digital assistants with built-in displays, has amplified the demand for compact, energy-efficient, and multifunctional display controllers.

Moreover, the growing popularity of interactive smart displays and touch-based interfaces in commercial and residential environments has added momentum to this market, encouraging manufacturers to innovate and enhance their product offerings. Display controllers are now essential for managing display functionalities across devices, ensuring seamless visuals and enhancing overall operational efficiency. Advancements in artificial intelligence (AI) and the Internet of Things (IoT) have led to a surge in the use of display controllers in smart devices that require intuitive and responsive user interfaces. This technological evolution is pushing manufacturers to focus on designing controllers that offer superior performance, lower latency, and improved power management, catering to the growing demand for immersive and dynamic displays.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $45.56 Billion |

| Forecast Value | $116.4 Billion |

| CAGR | 9.4% |

The smart display sector is witnessing significant expansion, with its market valued at USD 3.3 billion in 2024 and projected to grow at a CAGR of 11.3% over the forecast period. This growth is largely fueled by the increasing integration of AI and IoT capabilities into smart home ecosystems. Smart display controllers, which manage the interface and optimize device performance, are becoming more prevalent, enabling seamless user interactions and enhancing device functionality. The growing demand for smart displays in homes, offices, and public spaces is compelling companies to innovate, offering advanced features such as voice control, gesture recognition, and personalized user experiences.

The display controller market is segmented by end-use industries, including aerospace, automotive, consumer electronics, gaming, healthcare, and industrial control. The aerospace and defense segment, valued at USD 7.1 billion in 2024, is expected to register a CAGR of 10.6% during the forecast period. This growth is attributed to rising geopolitical tensions and the global push to strengthen national defense through the development of advanced aircraft systems. As aerospace technology becomes more sophisticated, the demand for reliable and high-performance display controllers continues to escalate, ensuring efficient operations in mission-critical environments.

Germany display controller market generated USD 2.4 billion in 2024 and is forecasted to grow at a CAGR of 9.9%. This growth is supported by the country's Industry 4.0 initiative, which emphasizes the digital transformation of manufacturing processes by integrating AI and IoT technologies. As Germany pushes for smart factories and automated systems, the demand for display controllers capable of supporting advanced manufacturing systems is expected to rise. Government-backed investments in cutting-edge technologies, automation, and industrial innovation are creating a robust foundation for sustained growth in the German display controller market. The adoption of modern display technologies in Germany's industrial sector is enhancing production efficiency and driving the continued expansion of the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research Approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Vendor matrix

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news and initiatives

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Expansion of consumer electronics with high-resolution displays

- 3.7.1.2 High-resolution and advanced display technologies

- 3.7.1.3 Industrial automation and IoT proliferation

- 3.7.1.4 Growing emphasis on energy-efficient devices

- 3.7.1.5 Adoption of ADAS in the automotive industry

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High cost of R&D and manufacturing.

- 3.7.2.2 Complexity in integration with advanced display technologies

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Bn)

- 4.1 Key trends

- 4.2 LCD display controller

- 4.3 Touchscreen display controller

- 4.4 Multi-display controller

- 4.5 Smart display controller

- 4.6 Digital display controller

- 4.7 Others

Chapter 5 Market Estimates and Forecast, By End Use Industry 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Aerospace & defence

- 5.3 Automotive

- 5.4 Consumer electronics

- 5.5 Gaming & entertainment

- 5.6 Healthcare

- 5.7 Industrial control

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 The U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Rest of Europe

- 6.4 Asia Pacific

- 6.4.1 Japan

- 6.4.2 China

- 6.4.3 India

- 6.4.4 South Korea

- 6.4.5 ANZ

- 6.4.6 Rest of Asia Pacific

- 6.5 Latin America

- 6.5.1 Brazil

- 6.5.2 Mexico

- 6.5.3 Rest of Latin America

- 6.6 Middle East and Africa

- 6.6.1 South Africa

- 6.6.2 UAE

- 6.6.3 Saudi Arabia

- 6.6.4 Rest of Middle East and Africa

Chapter 7 Company Profiles

- 7.1 Analog Devices

- 7.2 Barco

- 7.3 Broadcom Inc.

- 7.4 Fujitsu Limited

- 7.5 Infineon Technologies

- 7.6 LG Display Co., Ltd.

- 7.7 Maxim Integrated

- 7.8 Microchip Technology Inc.

- 7.9 NXP Semiconductors

- 7.10 ON Semiconductor

- 7.11 Qualcomm Technologies, Inc.

- 7.12 Renesas Electronics

- 7.13 ROHM Semiconductor

- 7.14 Samsung Electronics

- 7.15 STMicroelectronics

- 7.16 TDK Corporation

- 7.17 Texas Instruments

- 7.18 Toshiba Electronic Devices & Storage Corporation

- 7.19 Xi'an NovaStar Tech Co., Ltd.

電子價格標籤驅動積體電路:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

電子價格標籤驅動積體電路:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 全球顯示控制器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年)

全球顯示控制器市場研究報告 - 產業分析、規模、佔有率、成長、趨勢及預測(2025 年至 2033 年) 驅動 IC 市場(按產品類型、應用和地區)

驅動 IC 市場(按產品類型、應用和地區) 全球顯示驅動積體電路(DDIC)市場全球PMOLED市場2026 年至 2032 年顯示控制器市場類型、應用、最終用戶和地區分佈電子顯示器市場按技術、應用、最終用途行業和地區分類

全球顯示驅動積體電路(DDIC)市場全球PMOLED市場2026 年至 2032 年顯示控制器市場類型、應用、最終用戶和地區分佈電子顯示器市場按技術、應用、最終用途行業和地區分類 顯示控制器市場規模、佔有率、成長分析,按類型、按應用、按技術、按最終用戶、按地區 - 行業預測,2025-2032 年

顯示控制器市場規模、佔有率、成長分析,按類型、按應用、按技術、按最終用戶、按地區 - 行業預測,2025-2032 年 顯示控制器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029 年

顯示控制器市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、地區和競爭細分,2019-2029 年 顯示驅動器積體電路(DDIC)的全球市場2024-2028

顯示驅動器積體電路(DDIC)的全球市場2024-2028