|

市場調查報告書

商品編碼

1716487

一次性盤子市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Disposable Plates Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

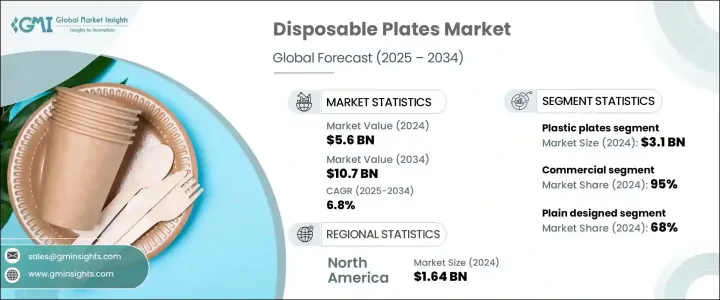

2024 年全球一次性盤子市場規模達到 56 億美元,預計 2025 年至 2034 年的複合年成長率為 6.8%。市場成長主要受到向永續生活方式轉變的日益增加以及對傳統餐具環保替代品的需求不斷成長的推動。隨著消費者環保意識的增強,人們明顯偏好由可生物分解、可堆肥和可回收材料製成的一次性盤子。人們越來越關注減少碳足跡和減少一次性塑膠垃圾,這是影響該市場發展軌蹟的關鍵促進因素。此外,食品配送服務、餐飲業務和快餐店的激增也增加了對便利性和永續餐飲解決方案的需求。

隨著越來越多的消費者優先考慮符合永續性和道德採購的產品,製造商正在透過開發由甘蔗渣、竹子、棕櫚葉和玉米澱粉基材料等可再生資源製成的盤子。這些環保盤子提供了實用的替代品,同時又不影響耐用性和美觀性。此外,政府日益加強的旨在遏制塑膠垃圾和鼓勵綠色包裝實踐的法規為市場參與者創造了新的機會。大型活動、公司聚會和公共場所擴大採用環保餐盤,這反映出更廣泛的文化轉向,即人們越來越重視環境責任。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 56億美元 |

| 預測值 | 107億美元 |

| 複合年成長率 | 6.8% |

市場按產品類型細分,包括塑膠、鋁、紙和其他材料,預計紙盤在 2025 年至 2034 年期間的複合年成長率為 7.3%。紙盤因其可生物分解、易於處理以及與多種食品的兼容性而廣受歡迎。消費者越來越遠離塑膠盤子,因為塑膠盤子因其對環境的不利影響而受到嚴格審查。該行業正在迅速轉向創新的可生物分解替代品,包括由植物性塑膠和生物塗層材料製成的產品,這些產品模仿塑膠的特性,但會自然分解而不會留下有毒殘留物。因此,紙盤逐漸成為追求實用和環保解決方案的消費者和企業的首選。

根據最終用途,一次性盤子市場分為住宅和商業領域,其中商業應用佔 2024 年總佔有率的 95%。商業領域包括食品服務提供者、餐飲公司和飲料中心,由於其便利性和成本效益,對一次性盤子的需求持續高漲。越來越多的餐廳開始採用棕櫚葉盤子,因為棕櫚葉盤子堅固耐用、外觀優雅,而且可以盛裝冷熱食物,不會洩漏或破損。採用這種永續的選擇也能讓企業吸引有環保意識的顧客,進而提高他們的品牌聲譽。

美國一次性盤子市場佔據全球主導地位,佔有 76% 的佔有率,2024 年創造的價值為 16.4 億美元。美國市場受益於對環境永續性的大力推動以及消費者對環保產品的明顯轉變。隨著人們忙碌生活節奏的加快,以及外帶餐飲的流行,國內對一次性盤子的需求不斷增加。隨著消費者優先考慮便利性和環境影響,一次性盤子等一次性產品繼續提供符合現代快節奏生活的實用解決方案。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素。

- 利潤率分析。

- 中斷

- 未來展望

- 製成品

- 經銷商

- 供應商格局

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 增強環保意識

- 消費者對環保產品的需求

- 產業陷阱與挑戰

- 轉向可重複使用的替代品

- 來自傳統塑膠的競爭

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 塑膠盤子

- 鋁板

- 紙磁碟

- 其他(樹葉盤、麥秸盤等)

第6章:市場估計與預測:依設計,2021-2034

- 主要趨勢

- 隔間

- 清楚的

第7章:市場估計與預測:按價格,2021-2034 年

- 主要趨勢

- 低的

- 中等的

- 高的

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 住宅

- 商業的

- 食品和飲料

- 飯店和咖啡館

- 接待和活動

- 其他(快餐店等)

第9章:市場估計與預測:按配銷通路,2021-2034

- 主要趨勢

- 線上

- 公司網站

- 電子商務

- 離線

- 超市/大賣場

- 專賣店

- 其他(食品服務供應商等)

第10章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 11 章:公司簡介

- D&W Fine Pack

- Dart Container Corporation

- Dopla

- Duni

- Fast Plast

- Genpak

- Georgia-Pacific

- Hotpack Group

- Huhtamaki

- International Paper

- Pactiv

- Polar Plastic

- Poppies Europe

- Seow Khim Polythelene

- Vegware

The Global Disposable Plates Market reached USD 5.6 billion in 2024 and is projected to expand at a CAGR of 6.8% from 2025 to 2034. The market growth is largely fueled by the rising shift toward sustainable living and the increasing demand for eco-friendly alternatives to traditional tableware. With growing environmental awareness among consumers, there is a notable preference for disposable plates made from biodegradable, compostable, and recycled materials. The expanding focus on reducing carbon footprints and minimizing single-use plastic waste has been a key driver shaping this market's trajectory. Additionally, the surge in food delivery services, catering businesses, and quick-service restaurants has amplified the need for convenient and sustainable dining solutions.

As more consumers prioritize products aligned with sustainability and ethical sourcing, manufacturers are responding by developing plates from renewable resources such as sugarcane bagasse, bamboo, palm leaves, and cornstarch-based materials. These eco-friendly plates offer a practical alternative without compromising on durability and aesthetics. Furthermore, increasing governmental regulations aimed at curbing plastic waste and encouraging green packaging practices are creating new opportunities for market players. The rising adoption of eco-friendly plates at large-scale events, corporate gatherings, and public venues reflects a broader cultural shift toward environmental responsibility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.6 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 6.8% |

The market is segmented by product type, including plastic, aluminum, paper, and other materials, with paper plates expected to witness a 7.3% CAGR from 2025 to 2034. Paper plates are gaining massive popularity due to their biodegradable nature, ease of disposal, and compatibility with a wide range of food products. Consumers are increasingly steering away from plastic plates, which are under heavy scrutiny for their adverse environmental impact. The industry is seeing a rapid shift toward innovative biodegradable alternatives, including products made from plant-based plastics and bio-coated materials that mimic the properties of plastic but break down naturally without leaving toxic residues. As a result, paper plates are emerging as the preferred choice for both consumers and businesses aiming for practical and eco-conscious solutions.

Based on end-use, the disposable plates market is classified into residential and commercial sectors, with commercial applications accounting for 95% of the overall share in 2024. The commercial segment, which includes food service providers, catering companies, and beverage centers, continues to drive high demand for disposable plates due to their convenience and cost-effectiveness. Increasingly, these establishments are adopting palm leaf plates, drawn to their sturdiness, elegant appearance, and ability to hold both hot and cold foods without leakage or breakage. The use of such sustainable options also allows businesses to appeal to environmentally aware customers, thereby enhancing their brand reputation.

U.S. Disposable Plates Market dominated the global landscape with a 76% share, generating USD 1.64 billion in 2024. The U.S. market benefits from a strong push toward environmental sustainability and a marked consumer shift toward eco-friendly products. The increasing pace of on-the-go lifestyles, along with the popularity of takeout meals and beverages, has significantly contributed to the rising demand for disposable plates in the country. With consumers prioritizing convenience and environmental impact, single-use products such as disposable plates continue to offer practical solutions that align with modern, fast-paced living.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Increased environmental awareness

- 3.5.1.2 Consumer demand for eco-friendly products

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 Shift toward reusable alternatives

- 3.5.2.2 Competition from traditional plastics

- 3.5.1 Growth drivers

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Plastic plates

- 5.3 Aluminum plates

- 5.4 Paper plates

- 5.5 Others (leaf plates, wheat straw plates etc.)

Chapter 6 Market Estimates & Forecast, By Design, 2021-2034 (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Compartmental

- 6.3 Plain

Chapter 7 Market Estimates & Forecast, By Price, 2021-2034 (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Food & beverage

- 8.3.2 Hotels and cafes

- 8.3.3 Hospitality and events

- 8.3.4 Others (quick-service restaurants etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Online

- 9.2.1 Company websites

- 9.2.2 E-commerce

- 9.3 Offline

- 9.3.1 Supermarkets/hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Others (foodservice suppliers etc.)

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 D&W Fine Pack

- 11.2 Dart Container Corporation

- 11.3 Dopla

- 11.4 Duni

- 11.5 Fast Plast

- 11.6 Genpak

- 11.7 Georgia-Pacific

- 11.8 Hotpack Group

- 11.9 Huhtamaki

- 11.10 International Paper

- 11.11 Pactiv

- 11.12 Polar Plastic

- 11.13 Poppies Europe

- 11.14 Seow Khim Polythelene

- 11.15 Vegware

一次性餐盤市場分析及預測(至2035年):依類型、材質、應用、產品類型、最終用戶、技術、功能、製程、部署類型及服務分類環保紙盤市場分析及預測(至2035年):類型、產品類型、材料類型、應用、最終用戶、製造流程、技術、功能、安裝類型、解決方案

一次性餐盤市場分析及預測(至2035年):依類型、材質、應用、產品類型、最終用戶、技術、功能、製程、部署類型及服務分類環保紙盤市場分析及預測(至2035年):類型、產品類型、材料類型、應用、最終用戶、製造流程、技術、功能、安裝類型、解決方案 全球一次性餐盤市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球一次性餐盤市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 中東和非洲紙杯市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031)紙杯產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙杯市場-佔有率分析、產業趨勢、統計和成長預測(2026-2031)紙杯產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 日本紙杯市場規模、佔有率、趨勢和預測:按杯型、壁型、應用、分銷管道、最終用戶和地區分類,2026-2034年

日本紙杯市場規模、佔有率、趨勢和預測:按杯型、壁型、應用、分銷管道、最終用戶和地區分類,2026-2034年 紙杯市場規模、佔有率和成長分析(按杯型、終端用途產業、壁厚類型、杯容量、銷售管道和地區分類)-2026-2033年產業預測

紙杯市場規模、佔有率和成長分析(按杯型、終端用途產業、壁厚類型、杯容量、銷售管道和地區分類)-2026-2033年產業預測 全球自動販賣杯市場紙杯市場:2025-2030年預測一次性盤子的全球市場

全球自動販賣杯市場紙杯市場:2025-2030年預測一次性盤子的全球市場