|

市場調查報告書

商品編碼

1716482

冷藏展示櫃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Refrigerated Display Cases Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

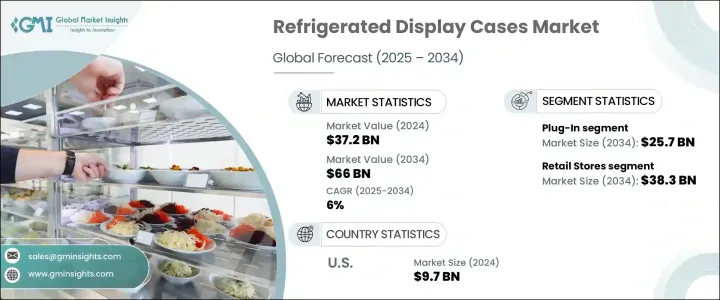

2024 年全球冷藏展示櫃市場價值為 372 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6%。對節能製冷系統的需求不斷成長以及對食品安全的日益關注是推動市場成長的主要因素。隨著零售店、超市和飯店企業繼續專注於提供新鮮和對溫度敏感的產品,對先進冷藏展示櫃的需求正在增加。此外,在更嚴格的政府法規和永續發展目標的推動下,環保冷凍解決方案的趨勢日益成長,促使製造商開發消耗更少能源並減少環境影響的創新系統。智慧冷卻系統、自動溫度監控和節能 LED 照明等技術進步進一步增強了現代冷藏展示櫃的吸引力。此外,物聯網功能的整合正在幫助企業在維持產品品質的同時提高營運效率,這對市場的上升趨勢做出了重大貢獻。

冷藏展示櫃市場分為三大主要產品類別:插入式、半插入式和遠端系統。插電式汽車在 2024 年創造了 152 億美元的市場規模,成為最受歡迎的細分市場。它們易於安裝和移動,並且無需外部冷凝器或複雜管道即可獨立運行,使其成為小型零售店、快閃店和臨時設置的理想選擇。隨著全球中小型零售企業數量的增加,對攜帶式、易於安裝的冷凍解決方案的需求預計將持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 372億美元 |

| 預測值 | 660億美元 |

| 複合年成長率 | 6% |

在應用方面,市場主要分為零售店、餐廳和酒店以及其他行業。零售店佔 2024 年總市佔率的 56.1%,預計到 2034 年將達到 383 億美元。這一成長是由對食品安全和保持產品新鮮度的日益重視所推動的。零售商正在投資溫控制冷設備,以延長產品保存期限,同時遵守政府規定的永續性標準。這些設備採用了智慧冷卻、節能壓縮機和 LED 照明系統等現代化技術,有助於降低營運成本並提高整體能源效率。

受美國食品零售和加工產業蓬勃發展的推動,美國冷藏展示櫃市場到 2024 年將創造 97 億美元的收入。超市、便利商店和食品服務機構數量的不斷增加推動了對高品質、可靠冷卻系統的需求。由於食品安全和能源效率仍然是美國市場的首要任務,企業擴大採用配備節能功能和改進的冷卻技術的先進冷藏展示櫃來滿足這些日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 零售商

- 衝擊力

- 成長動力

- 對新鮮和易腐食品的需求不斷增加

- 零售和食品服務業的採用率不斷提高

- 能源效率技術進步

- 消費者對方便即食食品的偏好日益增加

- 產業陷阱與挑戰

- 初始成本和維護費用高

- 嚴格的能源消耗監管要求

- 成長動力

- 消費者購買行為分析

- 人口趨勢

- 影響購買決策的因素

- 消費者產品採用

- 首選配銷通路

- 首選價格範圍

- 成長潛力分析

- 監管格局

- 定價分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 外掛

- 半插電式

- 偏僻的

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 零售店

- 餐廳和飯店

- 其他

第7章:市場估計與預測:依設計,2021 年至 2034 年

- 主要趨勢

- 垂直的

- 水平的

- 混合

第8章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 超市

- 便利商店

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第10章:公司簡介

- Arneg SPA

- Daikin Industries, Ltd.

- Danfoss A/S

- EPTA SPA Refrigeration

- Haier Group

- Hoshizaki International

- Hussmann Corporation

- Illinois Tool Works Inc.

- Lennox International

- Metalfrio Solutions SA

The Global Refrigerated Display Cases Market was valued at USD 37.2 billion in 2024 and is projected to grow at a CAGR of 6% between 2025 and 2034. The rising demand for energy-efficient refrigeration systems and increasing concerns about food safety are major factors driving the market's growth. As retail stores, supermarkets, and hospitality businesses continue to focus on offering fresh and temperature-sensitive products, the need for advanced refrigerated display cases is on the rise. Additionally, the growing trend toward eco-friendly refrigeration solutions, driven by stricter government regulations and sustainability goals, is pushing manufacturers to develop innovative systems that consume less energy and reduce environmental impact. Technological advancements, such as smart cooling systems, automated temperature monitoring, and energy-efficient LED lighting, further enhance the appeal of modern refrigerated display cases. Moreover, the integration of IoT-enabled features is helping businesses improve operational efficiency while maintaining product quality, which contributes significantly to the market's upward trajectory.

The refrigerated display cases market is segmented into three main product categories: Plug-In, Semi Plug-In, and Remote systems. Plug-In units generated USD 15.2 billion in 2024, making them the most popular segment. Their ease of installation and mobility, combined with their ability to operate independently without external condensers or complex piping, makes them ideal for small retail outlets, pop-up stores, and temporary setups. As the number of small and medium-sized retail businesses increases globally, the demand for portable and easy-to-install refrigeration solutions is expected to continue growing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $37.2 Billion |

| Forecast Value | $66 Billion |

| CAGR | 6% |

In terms of application, the market is primarily segmented into Retail Stores, Restaurants & Hotels, and Other sectors. Retail Stores accounted for 56.1% of the total market share in 2024 and are expected to reach USD 38.3 billion by 2034. This growth is driven by an increased focus on food safety and maintaining product freshness. Retailers are investing in temperature-controlled refrigeration units that extend product shelf life while adhering to government-mandated sustainability standards. These units incorporate modern technologies such as smart cooling, energy-efficient compressors, and LED lighting systems, which help reduce operational costs and improve overall energy efficiency.

The U.S. refrigerated display cases market generated USD 9.7 billion in 2024, driven by the country's robust food retail and processing industries. The rising number of supermarkets, convenience stores, and food service establishments has fueled the demand for high-quality, reliable refrigeration systems. As food safety and energy efficiency remain top priorities in the U.S. market, businesses are increasingly adopting advanced refrigerated display cases equipped with energy-saving features and improved cooling technologies to meet these growing demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for fresh and perishable food

- 3.2.1.2 Growing adoption in the retail and food service sectors

- 3.2.1.3 Technological advancements in energy efficiency

- 3.2.1.4 Rising consumer preference for convenient and ready-to-eat food

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost and maintenance expenses

- 3.2.2.2 Stringent regulatory requirements for energy consumption

- 3.2.1 Growth drivers

- 3.3 Consumer buying behavior analysis

- 3.3.1 Demographic trends

- 3.3.2 Factors affecting buying decision

- 3.3.3 Consumer product adoption

- 3.3.4 Preferred distribution channel

- 3.3.5 Preferred price range

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Plug-in

- 5.3 Semi plug-in

- 5.4 Remote

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Retail stores

- 6.3 Restaurants & hotels

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Design, 2021 – 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Vertical

- 7.3 Horizontal

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 – 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Supermarkets

- 8.3 Convenience stores

Chapter 9 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Arneg S.P.A

- 10.2 Daikin Industries, Ltd.

- 10.3 Danfoss A/S

- 10.4 EPTA S.P.A Refrigeration

- 10.5 Haier Group

- 10.6 Hoshizaki International

- 10.7 Hussmann Corporation

- 10.8 Illinois Tool Works Inc.

- 10.9 Lennox International

- 10.10 Metalfrio Solutions S.A.

冷藏展示櫃市場報告:依產品類型、產品設計、最終用途及地區分類,2026-2034年

冷藏展示櫃市場報告:依產品類型、產品設計、最終用途及地區分類,2026-2034年 冷藏展示櫃市場:2026-2032年全球市場預測(依產品類型、服務類型、溫度、門類型、最終用戶和安裝配置分類)義式霜淇淋展示櫃市場:依產品類型、門類型、容量範圍、最終用戶和安裝方式分類,全球預測(2026-2032年)

冷藏展示櫃市場:2026-2032年全球市場預測(依產品類型、服務類型、溫度、門類型、最終用戶和安裝配置分類)義式霜淇淋展示櫃市場:依產品類型、門類型、容量範圍、最終用戶和安裝方式分類,全球預測(2026-2032年) 冷藏展示櫃市場規模、佔有率和趨勢分析報告:按展示類型、類型、設計、最終用途和細分市場預測(2025-2033 年)

冷藏展示櫃市場規模、佔有率和趨勢分析報告:按展示類型、類型、設計、最終用途和細分市場預測(2025-2033 年) 2026年全球保溫器展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球檯式保溫器與展示櫃市場報告

2026年全球保溫器展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球冷藏展示櫃市場報告2026年全球檯式保溫器與展示櫃市場報告 冷藏展示櫃市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、產品設計、地區和競爭格局分類,2021-2031年全球桌上型披薩保溫器及展示櫃市場(依產品類型、容量、通路及應用分類)預測(2026-2032年)

冷藏展示櫃市場-全球產業規模、佔有率、趨勢、機會、預測:按產品類型、產品設計、地區和競爭格局分類,2021-2031年全球桌上型披薩保溫器及展示櫃市場(依產品類型、容量、通路及應用分類)預測(2026-2032年)