|

市場調查報告書

商品編碼

1716477

送貨無人機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Delivery Drone Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

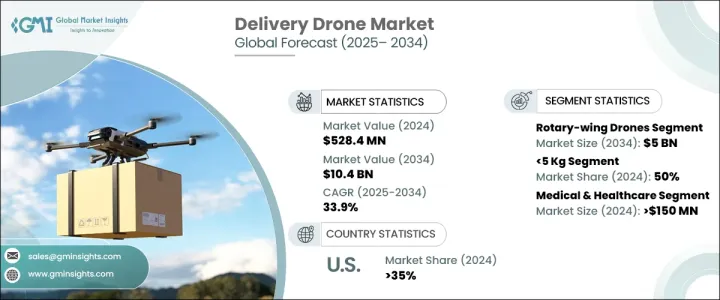

2024 年全球送貨無人機市場規模達到 5.284 億美元,預計 2025 年至 2034 年期間將以 33.9% 的強勁複合年成長率成長。各行各業對更快、更具成本效益、更有效率的送貨解決方案的需求不斷成長,推動了無人機技術的重大進步。隨著城市化的快速發展和電子商務的擴張,企業擴大轉向無人機物流,以滿足消費者對快速送貨日益成長的期望。無人機中人工智慧 (AI) 和自動化的融合增強了導航、障礙物檢測和整體運作效率,使其成為傳統運送方式的首選替代方案。

醫療保健是送貨無人機最具變革性的領域之一,事實證明,它們對於向偏遠或受災地區運送醫療用品、疫苗和緊急藥物至關重要。在基礎設施有限的地區,無人機是確保及時醫療救助的有效手段。此外,零售和食品配送服務正在經歷無人機物流的激增,該公司正在嘗試自動配送系統來最佳化最後一英里的營運。全球各地的監管機構也透過實施鼓勵創新同時確保安全和合規的政策,在簡化無人機使用方面發揮關鍵作用。隨著技術的不斷進步,送貨無人機的部署預計將進一步擴大,從而徹底改變全球供應鏈網路並改變各行各業的貨物運輸方式。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.284億美元 |

| 預測值 | 104億美元 |

| 複合年成長率 | 33.9% |

市場主要分為兩大類無人機:旋翼無人機和固定翼無人機。 2024年,旋翼無人機的收入將達到3億美元。由於具有垂直起飛和降落的能力,這些無人機在最後一英里的送貨服務中,尤其是在城市地區,佔據了主導地位。它們的靈活性和機動性使其成為在擁擠的城市景觀和複雜環境中導航的理想解決方案。人工智慧自動化進一步提高了他們的營運效率,使他們能夠即時檢測障礙物並確保安全可靠的交付。物流公司和電子商務巨頭對旋翼無人機的依賴日益增加,這將推動未來幾年市場擴張。

送貨無人機也依酬載能力分類,分為三個段落:5公斤、5-10公斤、10公斤以上。 2024 年,5 公斤類別佔據市場主導地位,佔有 50% 的佔有率。體積更小、重量更輕的無人機在城市和郊區的最後一英里物流中越來越受歡迎,事實證明,它在運輸小型消費品、食品和醫療用品方面非常有效。它們能夠簡化交付流程,同時降低營運成本,從而推動尋求創新且環保的供應鏈最佳化解決方案的企業廣泛採用。

2024 年,美國送貨無人機市場佔全球市場佔有率的 35%。該國仍然處於無人機技術發展的前沿,公共和私營部門的大量投資促進了無人機物流網路的創新。自主導航系統、人工智慧驅動的軍用無人機應用和民用無人機物流的進步進一步推動了市場成長。美國政府的支持性監管框架和持續的資助措施正在鞏固美國作為塑造全球送貨無人機產業未來的關鍵參與者的地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 製造商

- 零件供應商

- 技術提供者

- 服務提供者

- 最終用途

- 利潤率分析

- 技術與創新格局

- 重要新聞和舉措

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 對更快、更有效率的最後一哩配送解決方案的需求日益成長

- 電子商務呈指數級成長

- 無人機技術的持續進步

- 提高環境永續性

- 產業陷阱與挑戰

- 安全問題

- 監管挑戰

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:無人機市場評估與預測,2021 - 2034

- 主要趨勢

- 旋翼無人機

- 固定翼無人機

第6章:市場估計與預測:依酬載容量,2021 - 2034 年

- 主要趨勢

- 5公斤

- 5-10公斤

- 超過10公斤

第7章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 推進系統

- 導航與控制系統

- 感測器和成像設備

- 航空電子設備和飛行控制系統

- 電源電池

- 其他

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 電子商務與零售

- 醫療保健

- 送餐

- 包裹和郵政投遞

- 工業和貨運

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Amazon Prime Air

- DHL

- DJI

- EHang

- FedEx

- Flytrex

- Manna Drone Delivery

- Matternet

- Rakuten

- SkyCart

- Skyports

- UPS Flight Forward

- Wing (Alphabet Inc.)

- Wingcopter

- Zipline

The Global Delivery Drone Market reached USD 528.4 million in 2024 and is projected to grow at a robust CAGR of 33.9% between 2025 and 2034. The surging demand for faster, cost-effective, and more efficient delivery solutions across various industries is driving significant advancements in drone technology. With rapid urbanization and the expansion of e-commerce, businesses are increasingly turning to drone logistics to meet rising consumer expectations for swift deliveries. The integration of artificial intelligence (AI) and automation in drones is enhancing navigation, obstacle detection, and overall operational efficiency, making them a preferred alternative to traditional delivery methods.

One of the most transformative sectors for delivery drones is healthcare, where they are proving indispensable for transporting medical supplies, vaccines, and emergency medications to remote or disaster-stricken regions. In areas with limited infrastructure, drones provide an efficient means of ensuring timely medical assistance. Moreover, retail and food delivery services are witnessing a surge in drone-based logistics, with companies experimenting with autonomous delivery systems to optimize last-mile operations. Regulatory bodies across the globe are also playing a crucial role in streamlining drone usage by implementing policies that encourage innovation while ensuring safety and compliance. As technological advancements continue, the deployment of delivery drones is expected to expand further, revolutionizing global supply chain networks and transforming the way goods are transported across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $528.4 Million |

| Forecast Value | $10.4 Billion |

| CAGR | 33.9% |

The market is segmented into two primary drone categories: rotary-wing and fixed-wing drones. In 2024, rotary-wing drones accounted for USD 300 million in revenue. These drones have gained prominence in last-mile delivery services, particularly in urban areas, due to their ability to take off and land vertically. Their agility and maneuverability make them an ideal solution for navigating congested cityscapes and complex environments. AI-powered automation is further enhancing their operational efficiency, allowing them to detect obstacles in real-time and ensure safe, reliable deliveries. The growing reliance on rotary-wing drones by logistics companies and e-commerce giants is set to fuel market expansion in the coming years.

Delivery drones are also classified based on payload capacity, falling into three segments: 5 Kg, 5-10 Kg, and more than 10 Kg. The 5 Kg category dominated the market in 2024, holding a 50% share. Smaller, lightweight drones are gaining traction for last-mile logistics in urban and suburban areas, proving highly effective for transporting small consumer goods, food, and medical supplies. Their ability to streamline delivery processes while reducing operational costs is driving widespread adoption among businesses seeking innovative and eco-friendly solutions for supply chain optimization.

U.S. Delivery Drone Market accounted for 35% of the global market share in 2024. The country remains at the forefront of drone technology development, with substantial investments from both public and private sectors fostering innovation in drone logistics networks. Advancements in autonomous navigation systems, AI-driven military drone applications, and civilian drone logistics are further propelling market growth. The U.S. government's supportive regulatory framework and continued funding initiatives are solidifying the nation's position as a key player in shaping the future of the global delivery drone industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 Service providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Patent analysis

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising need for faster and more efficient last-mile delivery solutions

- 3.8.1.2 Exponential growth of e-commerce

- 3.8.1.3 Ongoing advancements in drone technology

- 3.8.1.4 Increasing environmental sustainability

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Safety concerns

- 3.8.2.2 Regulatory challenges

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Drone, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Rotary-wing drones

- 5.3 Fixed-wing drones

Chapter 6 Market Estimates & Forecast, By Payload Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 5 kg

- 6.3 5-10 kg

- 6.4 More than 10 kg

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Propulsion system

- 7.3 Navigation & control system

- 7.4 Sensors & imaging device

- 7.5 Avionics & flight control system

- 7.6 Power source battery

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 E-commerce & retail

- 8.3 Medical & healthcare

- 8.4 Food delivery

- 8.5 Parcel & postal delivery

- 8.6 Industrial & cargo

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Singapore

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Amazon Prime Air

- 10.2 DHL

- 10.3 DJI

- 10.4 EHang

- 10.5 FedEx

- 10.6 Flytrex

- 10.7 Manna Drone Delivery

- 10.8 Matternet

- 10.9 Rakuten

- 10.10 SkyCart

- 10.11 Skyports

- 10.12 UPS Flight Forward

- 10.13 Wing (Alphabet Inc.)

- 10.14 Wingcopter

- 10.15 Zipline

貨運無人機市場:2026-2032年全球市場預測(按無人機類型、負載容量、航程、動力來源、應用和最終用戶分類)

貨運無人機市場:2026-2032年全球市場預測(按無人機類型、負載容量、航程、動力來源、應用和最終用戶分類) 2026年全球無人機終端配送市場報告2026年全球貨運無人機市場報告2026年全球無人機配送市場報告2026年全球無人機配送服務市場報告

2026年全球無人機終端配送市場報告2026年全球貨運無人機市場報告2026年全球無人機配送市場報告2026年全球無人機配送服務市場報告 全球無人機配送市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球無人機配送市場規模、佔有率、趨勢和成長分析報告(2026-2034) 全球無人機配送市場-產業規模、佔有率、趨勢、機會、預測:按類型、負載容量、最終用戶、地區和競爭格局分類,2021-2031年

全球無人機配送市場-產業規模、佔有率、趨勢、機會、預測:按類型、負載容量、最終用戶、地區和競爭格局分類,2021-2031年 按無人機類型、組件、解決方案、有效負載容量、航程、速度和地區分類的配送無人機市場規模、佔有率和成長分析 - 行業預測(2026-2033 年)

按無人機類型、組件、解決方案、有效負載容量、航程、速度和地區分類的配送無人機市場規模、佔有率和成長分析 - 行業預測(2026-2033 年) 貨運無人機市場規模、佔有率、成長分析(按無人機類型、負載容量、應用、技術、最終用戶和地區分類)—2025-2032年產業預測

貨運無人機市場規模、佔有率、成長分析(按無人機類型、負載容量、應用、技術、最終用戶和地區分類)—2025-2032年產業預測 貨運無人機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

貨運無人機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測