|

市場調查報告書

商品編碼

1716476

透析市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dialysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

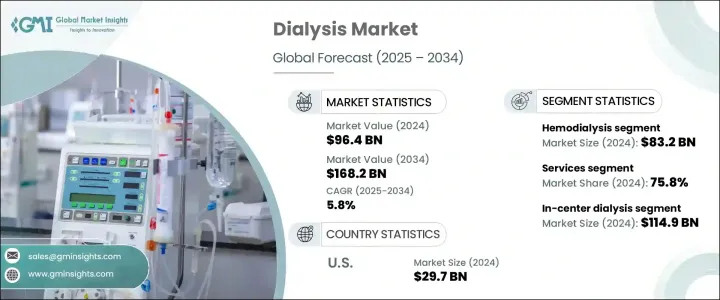

2024 年全球透析市場規模達到 964 億美元,預計 2025 年至 2034 年間將呈現 5.8% 的複合年成長率,呈現穩定成長態勢。這一成長主要受全球慢性腎病 (CKD)、末期腎臟病 (ESRD) 發病率上升以及人口老化加快的推動。糖尿病和高血壓是腎衰竭的兩個主要原因,其負擔日益加重,進一步推動了對透析治療的需求。隨著醫療保健系統面臨越來越大的提供有效腎臟護理的壓力,全球透析市場有望大幅擴張。此外,透析技術的進步、醫療保健支出的增加以及公共和私營部門推動的醫療保健框架的改善也促進了該市場的成長。

隨著人們對腎臟疾病的認知不斷提高以及患者獲得創新透析療法的機會增多,對家庭和中心透析服務的需求也在激增。此外,遠距醫療、遠距病人監控和具有使用者友好設計和改進的生物相容性的下一代透析機的整合正在改變治療格局,使患者能夠接受更安全、更有效的透析治療。個人化照護的轉變和家庭透析應用的成長趨勢預計將在未來十年進一步加速市場擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 964億美元 |

| 預測值 | 1682億美元 |

| 複合年成長率 | 5.8% |

透析市場大致分為兩大類:血液透析和腹膜透析。 2024 年,血液透析佔據主導地位,創造 832 億美元的收入。隨著全球 CKD 和 ESRD 病例持續攀升,醫療保健系統滿足日益成長的血液透析服務需求的壓力也越來越大。血液透析仍然是最廣泛使用的治療方法,主要是因為它對治療晚期腎衰竭具有很高的療效。血液透析機的持續創新,包括 Dialyzer HDF、生物相容性透析器、遠端監控系統和改進的人體工學設備的開發,正在提高治療效果和患者的舒適度。這些進步有望推動全球血液透析的普及,尤其是當越來越多的患者尋求可靠、有效的長期治療方案時。

透析市場進一步分為服務、消耗品和設備,其中服務佔據主導地位,到 2024 年將創造 758 億美元的市場價值。預計到 2034 年,服務部門的複合年成長率將達到 5.7%,包括慢性透析和急性透析服務,但慢性透析佔大部分佔有率。 CKD 患者通常需要持續透析治療,例如每週三到四次血液透析或每天進行腹膜透析。對透析服務的持續需求確保了穩定的收入來源,推動了該領域的長期成長。

光是美國透析市場在 2024 年的價值就達到 297 億美元,預計 2025 年至 2034 年的複合年成長率為 6%。作為最先進的醫療保健市場之一,美國在採用尖端透析技術和家庭透析解決方案方面處於領先地位。憑藉完善的專業透析中心和強大的基礎設施,該國正日益轉向遠端患者監控和家庭治療。 Fresenius Medical Care 和 DaVita Inc. 等主要市場參與者正在擴大其服務網路並整合先進的透析設備以滿足不斷成長的需求。對創新、患者友善解決方案的推動繼續促進美國市場的成長,使其成為全球透析市場的主要貢獻者。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 末期腎病(ESRD)患者數量不斷增加

- 糖尿病發生率上升

- 腎臟捐贈短缺

- 透析治療的有利報銷方案

- 已開發國家和開發中國家的研發投資不斷增加

- 產業陷阱與挑戰

- 產品召回

- 透析治療相關併發症

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 技術格局

- 報銷場景

- 波特的分析

- PESTEL分析

- 差距分析

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 血液透析

- 腹膜透析

第6章:市場估計與預測:按產品和服務,2021 - 2034 年

- 主要趨勢

- 服務

- 慢性透析

- 急性透析

- 耗材

- 透析器

- 導管

- 訪問產品

- 濃縮物

- 其他耗材

- 裝置

- 透析機

- 水處理系統

- 其他設備

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 中心透析

- 居家透析

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- angiodynamics

- Asahi KASEI

- B. Braun

- Baxter

- Becton, Dickinson and Company

- DaVita

- Dialife

- Fresenius

- JMS

- Medtronic

- NIKKISO

- NIPRO

- Rogosin Institute

- SATELLITE HEALTHCARE

- SB-KAWASUMI

- Teleflex

- TORAY

- US RENAL CARE

The Global Dialysis Market reached USD 96.4 billion in 2024 and is expected to witness a steady growth trajectory at a CAGR of 5.8% between 2025 and 2034. This growth is primarily driven by the rising incidence of chronic kidney disease (CKD), end-stage renal disease (ESRD), and a rapidly aging population worldwide. The increasing burden of diabetes and hypertension, the two major causes of kidney failure, is further propelling the demand for dialysis treatments. With healthcare systems under mounting pressure to provide effective renal care, the global dialysis market is poised to expand significantly. Additionally, advancements in dialysis technology, growing healthcare expenditures, and improved healthcare frameworks driven by public and private sectors are contributing to this market's growth.

The demand for home-based and in-center dialysis services is also surging, supported by rising awareness of renal diseases and enhanced patient access to innovative dialysis therapies. Furthermore, the integration of telemedicine, remote patient monitoring, and next-generation dialysis machines with user-friendly designs and improved biocompatibility are transforming the treatment landscape, allowing patients to undergo safer and more efficient dialysis sessions. The shift toward personalized care and the growing trend of home dialysis adoption are expected to further accelerate market expansion over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $96.4 Billion |

| Forecast Value | $168.2 Billion |

| CAGR | 5.8% |

The dialysis market is broadly segmented into two main types-hemodialysis and peritoneal dialysis. Hemodialysis accounted for a dominant share in 2024, generating USD 83.2 billion in revenue. As CKD and ESRD cases continue to climb globally, the pressure on healthcare systems to meet the growing demand for hemodialysis services is intensifying. Hemodialysis remains the most widely used treatment method, primarily because of its high efficacy in managing advanced kidney failure. The ongoing innovations in hemodialysis machines, including the development of Dialyzer HDF, biocompatible dialyzers, telemonitoring systems, and improved ergonomic equipment, are enhancing treatment outcomes and patient comfort. These advancements are expected to boost the adoption of hemodialysis worldwide, especially as more patients seek reliable and efficient long-term treatment options.

The dialysis market is further categorized into services, consumables, and equipment, with services dominating the landscape by generating USD 75.8 billion in 2024. Expected to grow at a 5.7% CAGR through 2034, the services segment includes both chronic and acute dialysis services, though chronic dialysis accounts for the majority share. Patients with CKD typically require ongoing dialysis treatments, such as three to four hemodialysis sessions weekly or daily peritoneal dialysis. This sustained need for dialysis services ensures a consistent revenue stream, driving long-term growth in this segment.

U.S. Dialysis Market alone was valued at USD 29.7 billion in 2024, with an anticipated growth rate of 6% CAGR from 2025 to 2034. As one of the most advanced healthcare markets, the U.S. is at the forefront of adopting cutting-edge dialysis technologies and home dialysis solutions. With well-established specialized dialysis centers and robust infrastructure, the country is witnessing an increasing shift toward remote patient monitoring and home-based treatments. Key market players such as Fresenius Medical Care and DaVita Inc. are expanding their service networks and integrating advanced dialysis equipment to meet rising demand. The push for innovative, patient-friendly solutions continues to enhance market growth across the U.S., positioning it as a leading contributor to the global dialysis market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of end-stage renal diseases (ESRD) patients

- 3.2.1.2 Increasing incidence of diabetes

- 3.2.1.3 Shortage of donor kidneys

- 3.2.1.4 Favorable reimbursement scenario for dialysis treatment

- 3.2.1.5 Growing research and development investments in developed and developing countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Product recalls

- 3.2.2.2 Complications associated with dialysis treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Gap analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hemodialysis

- 5.3 Peritoneal dialysis

Chapter 6 Market Estimates and Forecast, By Product and Services, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Services

- 6.2.1 Chronic dialysis

- 6.2.2 Acute dialysis

- 6.3 Consumables

- 6.3.1 Dialyzers

- 6.3.2 Catheters

- 6.3.3 Access products

- 6.3.4 Concentrates

- 6.3.5 Other consumables

- 6.4 Equipment

- 6.4.1 Dialysis machines

- 6.4.2 Water treatment systems

- 6.4.3 Other equipment

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 In-center dialysis

- 7.3 Home dialysis

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 angiodynamics

- 9.2 Asahi KASEI

- 9.3 B. Braun

- 9.4 Baxter

- 9.5 Becton, Dickinson and Company

- 9.6 DaVita

- 9.7 Dialife

- 9.8 Fresenius

- 9.9 JMS

- 9.10 Medtronic

- 9.11 NIKKISO

- 9.12 NIPRO

- 9.13 Rogosin Institute

- 9.14 SATELLITE HEALTHCARE

- 9.15 SB-KAWASUMI

- 9.16 Teleflex

- 9.17 TORAY

- 9.18 U.S. RENAL CARE

聚碸透析器市場:依透析器類型、滅菌方法、膜結構、通路和最終用戶分類-2026-2032年全球預測透析服務市場:按產品類型、透析方法、治療環境、患者類型和最終用戶分類-2026-2032年全球預測

聚碸透析器市場:依透析器類型、滅菌方法、膜結構、通路和最終用戶分類-2026-2032年全球預測透析服務市場:按產品類型、透析方法、治療環境、患者類型和最終用戶分類-2026-2032年全球預測 2026年全球血液透析機及設備市場報告

2026年全球血液透析機及設備市場報告 日本透析設備市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類,2026-2034年透析市場規模、佔有率、趨勢及預測(按類型、產品類型、服務、最終用戶和地區分類),2026-2034年

日本透析設備市場規模、佔有率、趨勢和預測:按類型、最終用戶和地區分類,2026-2034年透析市場規模、佔有率、趨勢及預測(按類型、產品類型、服務、最終用戶和地區分類),2026-2034年 透析中心市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按所有權、透析類型、服務、地區和競爭情況分類),2021-2031年透析試劑盒市場:依材料、透析方法、定價模式、最終用戶和銷售管道,全球預測,2026-2032年

透析中心市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按所有權、透析類型、服務、地區和競爭情況分類),2021-2031年透析試劑盒市場:依材料、透析方法、定價模式、最終用戶和銷售管道,全球預測,2026-2032年 全球透析市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)日本透析市場報告(按類型(血液透析 (HD)、腹膜透析 (PD))、產品和服務(設備、耗材、透析藥物、服務)、最終用戶(中心透析、家庭透析)和地區分類,2026-2034 年)

全球透析市場:市場規模、市場佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)日本透析市場報告(按類型(血液透析 (HD)、腹膜透析 (PD))、產品和服務(設備、耗材、透析藥物、服務)、最終用戶(中心透析、家庭透析)和地區分類,2026-2034 年) 透析設備市場規模、佔有率及成長分析(按類型、最終用戶和地區分類)-2026-2033年產業預測

透析設備市場規模、佔有率及成長分析(按類型、最終用戶和地區分類)-2026-2033年產業預測