|

市場調查報告書

商品編碼

1708150

顱骨植入物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cranial Implant Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

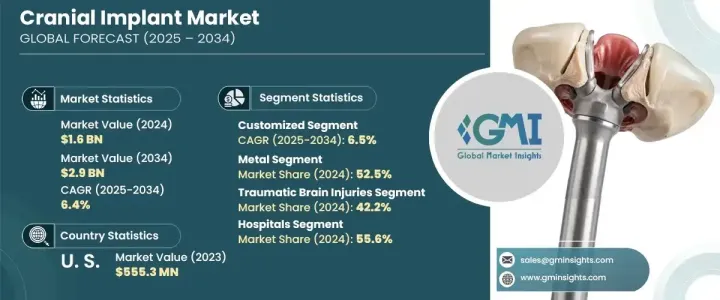

2024 年全球顱腦植入物市場價值為 16 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.4%。受神經系統疾病、創傷性腦損傷盛行率上升以及先進外科技術的日益普及的推動,該市場正在穩步成長。在全球範圍內,越來越多的患者因中風、癲癇、阿茲海默症和先天性顱骨畸形等疾病而需要進行顱骨重建。隨著全球人口老化和事故相關頭部損傷的增加,對高品質顱腦植入物的需求預計將激增。 3D 列印和生物材料的不斷進步正在徹底改變這個行業,使植入物更加精確、耐用和生物相容性。此外,已開發市場的有利監管政策正在加速產品核准,使企業能夠更有效地推出創新解決方案。新興經濟體醫療保健投資的增加和神經和創傷護理可近性的提高也促進了市場擴張。

市場分為客製化產品和非客製化產品。 2024 年,客製化顱骨植入物產值達 10 億美元,並將實現顯著成長,預計未來十年的複合年成長率為 6.5%。這些植入物因其能夠提供精確的貼合度、增強重建效果和功能性能而越來越受歡迎。利用 CT 掃描和 MRI 等先進的影像技術,醫療專業人員可以創建與個人顱骨結構無縫對齊的患者專用植入物。這種個人化的方法顯著改善了術後恢復和美學效果,推動了整個醫療保健行業對客製化解決方案的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16億美元 |

| 預測值 | 29億美元 |

| 複合年成長率 | 6.4% |

顱骨植入物主要由金屬、聚合物或陶瓷材料製成。 2024 年,金屬產業佔據市場主導地位,佔有 52.5% 的佔有率,創造了 8.309 億美元的收入。鈦及其合金由於其出色的強度、生物相容性和長期耐用性仍然是首選。金屬植入物為大腦提供了卓越的保護,使其成為從創傷或複雜的顱骨手術中恢復的患者的理想選擇。與聚合物植入物相比,金屬植入物的壽命更長、失敗率更低,因此在醫療程序中廣泛使用。

2024 年北美顱腦植入物市場規模為 6.406 億美元,預計到 2034 年將達到 12 億美元。這一成長主要得益於創傷性腦損傷 (TBI) 發病率的上升以及該地區先進的醫療保健基礎設施。尤其是美國,受益於鼓勵尖端醫療技術開發和商業化的支持性監管環境。人工智慧輔助成像、3D 列印和生物工程材料的採用正在重塑顱骨植入物的格局,從而實現更有效率、更個性化的治療方案。這些技術進步,加上強勁的醫療保健支出和對神經外科解決方案的高度認知,使北美成為全球市場成長的主要貢獻者。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 創傷性腦損傷(TBI)病例不斷增加

- 神經系統疾病和顱骨畸形的盛行率不斷上升

- 3D列印和客製化植入技術的進步

- 生物相容性和智慧材料的採用日益增多

- 產業陷阱與挑戰

- 顱骨植入物和外科手術費用高昂

- 嚴格的監管批准和合規要求

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 客製化

- 非客製化

第6章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 金屬

- 聚合物

- 聚醚醚酮(PEEK)

- 聚甲基丙烯酸甲酯(PMMA)

- 其他聚合物

- 陶瓷製品

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 創傷性腦損傷

- 腫瘤切除病例

- 神經外科重建手術

- 其他應用

第8章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 神經外科中心

- 學術研究機構

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- 3D Systems

- Acumed LLC

- Anatomics Pty Ltd

- B. Braun SE

- Brainlab

- evonos GmbH & Co. KG

- Integra LifeSciences

- Johnson & Johnson

- Kelyniam Global Inc.

- KLS Martin

- Medartis AG

- Medtronic

- Matrix Surgical USA

- Renishaw plc.

- Stryker Corporation

- Zimmer Biomet

The Global Cranial Implant Market was valued at USD 1.6 billion in 2024 and is projected to grow at a CAGR of 6.4% between 2025 and 2034. The market is experiencing steady growth, driven by the rising prevalence of neurological disorders, traumatic brain injuries, and the increasing adoption of advanced surgical techniques. A growing number of patients worldwide require cranial reconstruction due to conditions such as strokes, epilepsy, Alzheimer's disease, and congenital skull deformities. With an aging global population and an uptick in accident-related head injuries, demand for high-quality cranial implants is expected to surge. Continuous advancements in 3D printing and biomaterials are revolutionizing the industry, making implants more precise, durable, and biocompatible. Furthermore, favorable regulatory policies in developed markets are accelerating product approvals, allowing companies to introduce innovative solutions more efficiently. Increasing healthcare investments and improved accessibility to neuro and trauma care in emerging economies also contribute to market expansion.

The market is divided into customized and non-customized products. In 2024, customized cranial implants generated USD 1 billion and are set for notable growth, with a projected CAGR of 6.5% over the next decade. These implants are gaining popularity due to their ability to provide a precise fit, enhancing both reconstructive outcomes and functional performance. Using advanced imaging techniques such as CT scans and MRIs, medical professionals can create patient-specific implants that align seamlessly with an individual's skull structure. This personalized approach significantly improves post-surgical recovery and aesthetic results, fueling the demand for customized solutions across the healthcare sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.9 Billion |

| CAGR | 6.4% |

Cranial implants are primarily made from metal, polymer, or ceramic materials. The metal segment dominated the market in 2024, holding a 52.5% share and generating USD 830.9 million in revenue. Titanium and its alloys remain the preferred choice due to their exceptional strength, biocompatibility, and long-term durability. Metal implants offer superior protection to the brain, making them ideal for patients recovering from traumatic injuries or complex skull surgeries. Compared to polymer-based implants, metal options provide enhanced longevity and lower failure rates, driving their widespread adoption in medical procedures.

North America Cranial Implant Market generated USD 640.6 million in 2024 and is projected to reach USD 1.2 billion by 2034. This growth is largely driven by the increasing incidence of traumatic brain injuries (TBI) and the region's advanced healthcare infrastructure. The United States, in particular, benefits from a supportive regulatory environment that encourages the development and commercialization of cutting-edge medical technologies. The adoption of AI-assisted imaging, 3D printing, and bioengineered materials is reshaping the landscape of cranial implants, enabling more efficient and customized treatment options. These technological advancements, combined with strong healthcare spending and high awareness of neurosurgical solutions, position North America as a key contributor to global market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing cases of traumatic brain injuries (TBI)

- 3.2.1.2 Growing prevalence of neurological disorders and skull deformities

- 3.2.1.3 Advancements in 3D printing and custom implant technologies

- 3.2.1.4 Increasing adoption of biocompatible and smart materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cranial implants and surgical procedures

- 3.2.2.2 Stringent regulatory approvals and compliance requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Customized

- 5.3 Non-customized

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Metal

- 6.3 Polymer

- 6.3.1 Polyetheretherketone (PEEK)

- 6.3.2 Polymethylmethacrylate (PMMA)

- 6.3.3 Other polymers

- 6.4 Ceramic

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Traumatic brain injuries

- 7.3 Tumor resection cases

- 7.4 Neurosurgical reconstructive procedures

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Neurosurgery centers

- 8.4 Academic and research institute

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 3D Systems

- 10.2 Acumed LLC

- 10.3 Anatomics Pty Ltd

- 10.4 B. Braun SE

- 10.5 Brainlab

- 10.6 evonos GmbH & Co. KG

- 10.7 Integra LifeSciences

- 10.8 Johnson & Johnson

- 10.9 Kelyniam Global Inc.

- 10.10 KLS Martin

- 10.11 Medartis AG

- 10.12 Medtronic

- 10.13 Matrix Surgical USA

- 10.14 Renishaw plc.

- 10.15 Stryker Corporation

- 10.16 Zimmer Biomet

顱骨植入市場:2026-2032年全球市場預測(依產品類型、材料、適應症、最終用戶及通路分類)

顱骨植入市場:2026-2032年全球市場預測(依產品類型、材料、適應症、最終用戶及通路分類) 2026年全球個人化顱骨植入市場報告2026年全球顱骨植入市場報告

2026年全球個人化顱骨植入市場報告2026年全球顱骨植入市場報告 顱骨植入市場規模、佔有率和成長分析(按產品類型、材質、最終用途和地區分類)-2026-2033年產業預測

顱骨植入市場規模、佔有率和成長分析(按產品類型、材質、最終用途和地區分類)-2026-2033年產業預測 2021-2031 年北美顱腦植入物市場報告(範圍、細分、動態和競爭分析)

2021-2031 年北美顱腦植入物市場報告(範圍、細分、動態和競爭分析) 2021-2031 年歐洲顱腦植入物市場報告(範圍、細分、動態和競爭分析)

2021-2031 年歐洲顱腦植入物市場報告(範圍、細分、動態和競爭分析) 2021-2031年亞太地區顱腦植入物市場報告(範圍、細分、動態和競爭分析)

2021-2031年亞太地區顱腦植入物市場報告(範圍、細分、動態和競爭分析) 個人化顱骨植入物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

個人化顱骨植入物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 全球顱顏植入市場

全球顱顏植入市場 顱骨植入市場規模、佔有率、趨勢分析報告:依產品、材料、最終用途、細分市場預測,2025-2030

顱骨植入市場規模、佔有率、趨勢分析報告:依產品、材料、最終用途、細分市場預測,2025-2030