|

市場調查報告書

商品編碼

1699431

液體冷卻系統市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Liquid Cooling Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

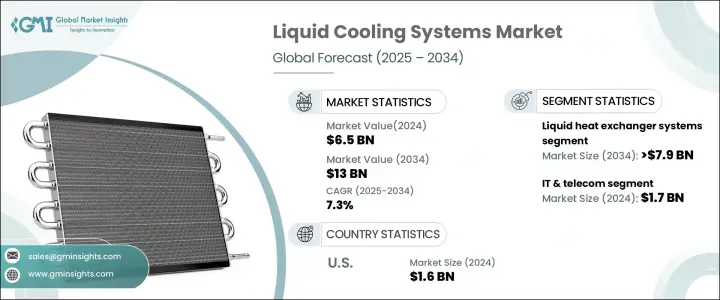

2024 年全球液體冷卻系統市場價值為 65 億美元,預計 2025 年至 2034 年的複合年成長率為 7.3%。高效能運算、人工智慧和機器學習的需求激增,正在加速從傳統空氣冷卻到更高效的液體冷卻解決方案的轉變。伺服器功率密度的快速增加暴露了空氣冷卻方法的局限性,導致資料中心採用液體冷卻作為更好的替代方案。增強的熱管理能力使得液體冷卻對於處理高密度伺服器環境不可或缺。根據行業研究,液體冷卻具有更高的散熱效率,可確保提高性能並節省能源。隨著企業優先考慮現代 IT 基礎架構的節能解決方案,市場正在穩步擴張。

市場按產品類型細分為液體熱交換器系統和基於壓縮機的系統。液體熱交換器系統在 2024 年的收入為 40 億美元,預計到 2034 年將超過 79 億美元。這些系統透過液體介質傳遞熱量,從而提供卓越的能源效率,減少對機械壓縮的依賴。人們對更安靜、高性能的冷卻解決方案的日益青睞推動了多個行業對液體熱交換器系統的巨大需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 65億美元 |

| 預測值 | 130億美元 |

| 複合年成長率 | 7.3% |

根據最終用戶細分,市場涵蓋各個行業,包括 BFSI、醫療保健、分析設備、工業、IT 和電信、汽車、政府和國防等。 2024 年,IT 和電信成為主導領域,創造 17 億美元的收入並佔據約 56% 的市場佔有率。對先進熱管理解決方案日益成長的需求正在推動 IT 和電信業的採用。隨著雲端運算、人工智慧和邊緣運算導致資料處理工作量不斷增加,傳統的冷卻技術已被證明效率低。液體冷卻因其能夠在高功率運算環境中有效管理熱量、降低能耗並提高整體系統效能而越來越受到青睞。產業報告顯示,液體冷卻系統的傳熱效率可比空氣冷卻方法高出 1,000 倍,使其成為大型 IT 基礎架構的首選。

2024 年,美國液體冷卻系統市場規模接近 16 億美元,預計 2025 年至 2034 年期間的複合年成長率將達到 8%。美國在高效能運算、超大規模資料中心和先進技術基礎設施方面的強大實力為其市場領導地位做出了貢獻。公司正在迅速投資液體冷卻解決方案,以提高營運效率和永續性。隨著人工智慧、機器學習和邊緣運算不斷推動資料處理要求,傳統的冷卻方法正在變得過時。對創新冷卻技術的需求不斷成長,支持了美國液體冷卻系統市場的擴張。領先科技公司的存在進一步加強了該地區在行業中的地位。

目錄

第1章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商格局

- 重要新聞和舉措

- 監管格局

- 衝擊力

- 成長動力

- 資料中心熱密度不斷上升

- 能源效率和永續發展舉措

- 技術進步和行業採用

- 產業陷阱與挑戰

- 初始資本支出高

- 缺乏標準化和相容性問題

- 成長動力

- 技術格局

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:依產品類型,2021-2032

- 主要趨勢

- 液體熱交換器系統

- 基於壓縮機的系統

第6章:市場估計與預測:依組件,2021 年至 2034 年

- 主要趨勢

- 解決方案

- 服務

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- BFSI(銀行、金融服務和保險)

- 衛生保健

- 分析設備

- 工業的

- IT和電信

- 汽車

- 政府和國防

- 其他(能源、零售、製造等)

第8章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直接的

- 間接

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 印尼

- 新加坡

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- MEA 其餘地區

第10章:公司簡介

- Asetek Inc

- Boyd Corporation

- CoolIT Systems

- Emerson Electric Co

- Fujitsu

- Green Revolution Cooling Inc

- HUBER+SUHNER

- Koolance

- Lytron Inc

- MillerWelds

- Newegg

- Parker NA

- Rittal GmbH & Co

- Schneider Electric SE

- Watteredge

The Global Liquid Cooling Systems Market was valued at USD 6.5 billion in 2024 and is projected to expand at a CAGR of 7.3% from 2025 to 2034. The surge in demand for high-performance computing, artificial intelligence, and machine learning is accelerating the shift from traditional air cooling to more efficient liquid cooling solutions. The rapid increase in server power densities has exposed the limitations of air-based cooling methods, leading data centers to adopt liquid cooling as a superior alternative. Enhanced thermal management capabilities make liquid cooling indispensable for handling high-density server environments. According to industry research, liquid cooling delivers greater heat dissipation efficiency, ensuring improved performance and energy savings. The market is witnessing steady expansion as businesses prioritize energy-efficient solutions for modern IT infrastructure.

The market is segmented by product type into liquid heat exchanger systems and compressor-based systems. Liquid heat exchanger systems accounted for USD 4 billion in revenue in 2024 and are expected to exceed USD 7.9 billion by 2034. These systems provide superior energy efficiency by transferring heat through a liquid medium, reducing the reliance on mechanical compression. The increasing preference for quieter, high-performance cooling solutions is driving significant demand for liquid heat exchanger systems across multiple industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $13 Billion |

| CAGR | 7.3% |

By end-user segmentation, the market encompasses various industries, including BFSI, healthcare, analytical equipment, industrial, IT & telecom, automotive, government & defense, and others. IT & telecom emerged as the dominant segment in 2024, generating USD 1.7 billion in revenue and capturing approximately 56% of the market share. The growing need for advanced thermal management solutions is propelling adoption in IT and telecom industries. With data processing workloads intensifying due to cloud computing, AI, and edge computing, traditional cooling techniques are proving inefficient. Liquid cooling is increasingly favored for its ability to manage heat effectively in high-power computing environments, lower energy consumption, and enhance overall system performance. Industry reports suggest that liquid cooling systems can achieve heat transfer efficiency up to 1,000 times greater than air-based methods, making them a preferred choice for large-scale IT infrastructure.

The US market for liquid cooling systems stood at nearly USD 1.6 billion in 2024 and is set to grow at a CAGR of 8% between 2025 and 2034. The country's strong presence in high-performance computing, hyperscale data centers, and advanced technological infrastructure contributes to its market leadership. Companies are rapidly investing in liquid cooling solutions to enhance operational efficiency and sustainability. As AI, machine learning, and edge computing continue to push data processing requirements, traditional cooling approaches are becoming obsolete. The demand for innovative cooling technologies is growing, supporting the expansion of the liquid cooling systems market in the US. The presence of leading technology firms further strengthens the region's position in the industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Escalating heat densities in data centers

- 3.5.1.2 Energy efficiency and sustainability Initiatives

- 3.5.1.3 Technological advancements and industry adoption

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High initial capital expenditure

- 3.5.2.2 Lack of standardization and compatibility Issues

- 3.5.1 Growth drivers

- 3.6 Technology landscape

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2032 (USD Billion) (Units)

- 5.1 Key Trends

- 5.2 Liquid heat exchanger systems

- 5.3 Compressor-Based systems

Chapter 6 Market Estimates & Forecast, By Component, 2021 – 2034, (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Solution

- 6.3 Services

Chapter 7 Market Estimates & Forecast, By End Use, 2021 – 2034, (USD Billion) (Units)

- 7.1 Key trends

- 7.2 BFSI (banking, financial services, and insurance)

- 7.3 Healthcare

- 7.4 Analytical equipment

- 7.5 Industrial

- 7.6 IT & telecom

- 7.7 Automotive

- 7.8 Government & defense

- 7.9 Others (Energy, Retail, Manufacturing, etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Malaysia

- 9.4.7 Indonesia

- 9.4.8 Singapore

- 9.4.9 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Asetek Inc

- 10.2 Boyd Corporation

- 10.3 CoolIT Systems

- 10.4 Emerson Electric Co

- 10.5 Fujitsu

- 10.6 Green Revolution Cooling Inc

- 10.7 HUBER+SUHNER

- 10.8 Koolance

- 10.9 Lytron Inc

- 10.10 MillerWelds

- 10.11 Newegg

- 10.12 Parker NA

- 10.13 Rittal GmbH & Co

- 10.14 Schneider Electric SE

- 10.15 Watteredge

液冷系統市場:按類型、組件、系統類型、冷卻技術、安裝配置和應用分類-2026-2032年全球市場預測

液冷系統市場:按類型、組件、系統類型、冷卻技術、安裝配置和應用分類-2026-2032年全球市場預測 冷板液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)行內冷卻分配設備市場:依冷卻能力、產品類型、氣流方向、安裝方式、冷卻方式、最終用戶分類,全球預測,2026-2032年液-液冷卻劑分配單元市場:按單元類型、冷卻能力、流量、材料類型、價格範圍、終端用戶產業和銷售管道,全球預測,2026-2032年高冷卻能力冷卻液分配單元市場:依冷卻類型、產品類型、容量範圍、運轉模式、控制技術、應用、最終用戶、通路分類,全球預測,2026-2032年兩相液冷系統市場(依產品類型、終端用戶產業、冷卻劑和應用分類)-全球預測,2026-2032年按技術、系統容量、冷卻劑、最終用戶和部署方式分類的資料中心主動式液冷系統全球預測(2026-2032 年)

冷板液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)行內冷卻分配設備市場:依冷卻能力、產品類型、氣流方向、安裝方式、冷卻方式、最終用戶分類,全球預測,2026-2032年液-液冷卻劑分配單元市場:按單元類型、冷卻能力、流量、材料類型、價格範圍、終端用戶產業和銷售管道,全球預測,2026-2032年高冷卻能力冷卻液分配單元市場:依冷卻類型、產品類型、容量範圍、運轉模式、控制技術、應用、最終用戶、通路分類,全球預測,2026-2032年兩相液冷系統市場(依產品類型、終端用戶產業、冷卻劑和應用分類)-全球預測,2026-2032年按技術、系統容量、冷卻劑、最終用戶和部署方式分類的資料中心主動式液冷系統全球預測(2026-2032 年) 液冷系統市場規模、佔有率和趨勢分析報告:按類型、容量、最終用途、地區和細分市場預測(2026-2033 年)

液冷系統市場規模、佔有率和趨勢分析報告:按類型、容量、最終用途、地區和細分市場預測(2026-2033 年) 全球液冷系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球液冷系統市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球液冷系統市場報告

2026年全球液冷系統市場報告