|

市場調查報告書

商品編碼

1698587

靜脈注射解決方案市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Intravenous Solutions Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

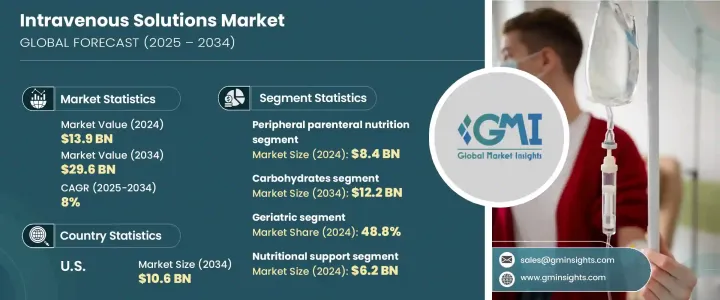

全球靜脈注射溶液市場價值為 139 億美元,預計 2025 年至 2034 年的複合年成長率為 8%。靜脈 (IV) 溶液是直接注射到患者血液中的無菌液體,用於維持水分、輸送藥物和提供必需的營養素。由於營養不良現像日益嚴重、慢性病盛行以及糧食不安全,靜脈注射溶液的需求正在上升。全球相當一部分人口面臨營養不良的問題,加劇了對靜脈注射治療的需求。此外,新生兒和兒科護理中靜脈輸液的使用日益增多與早產的高發生率有關,而早產需要專門的營養支持。世界各地的醫院和醫療機構繼續將靜脈注射解決方案融入患者護理中,用於補液療法、營養補充和術後恢復。

市場依類型分為全腸外營養及周邊腸外營養(PPN)。 2024 年,PPN 領域佔據市場主導地位,營收達 84 億美元。 PPN 是短期營養支持的首選方法,透過周邊靜脈提供葡萄糖、胺基酸和脂質等重要營養素。它有助於維持營養平衡,預防營養缺陷,並為口服攝取有限的患者提供支持。研究表明,及時進行 PPN 治療可降低感染和代謝併發症的風險,使其成為現代醫療治療的重要組成部分。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 139億美元 |

| 預測值 | 296億美元 |

| 複合年成長率 | 8% |

按成分細分,市場包括維生素和礦物質、碳水化合物、單劑量胺基酸、腸外脂肪乳劑和其他必需化合物。碳水化合物部分佔 2024 年市場總收入的 40.6%,預計到 2034 年將達到 122 億美元。葡萄糖基靜脈注射溶液被廣泛用於為無法透過常規方式獲得營養的重症患者提供熱量支持。這些解決方案在維持代謝穩定、防止肌肉分解和幫助恢復方面發揮關鍵作用。臨床研究支持碳水化合物類靜脈注射溶液在改善患者預後的有效性,尤其是在術後和創傷照護方面。

按年齡層別分類,老年人口佔據最高的市場佔有率,佔 2024 年總收入的 48.8%。老年人由於口渴感減弱、行動不便和各種健康狀況,很容易脫水。靜脈注射溶液可確保有效補水和營養輸送,預防與慢性疾病相關的併發症。全球人口老化進一步推動了需求,醫療保健提供者越來越依賴靜脈注射療法來治療吞嚥困難或胃腸道疾病的老年患者。

在應用方面,市場分為營養支持、輸血以及液體和電解質平衡。 2024 年,營養支持領域引領市場,創造 62 億美元的收入。營養不良、慢性病和術後恢復需求的發生率不斷上升,導致了這種成長。患有胃腸道疾病或影響營養吸收的疾病的患者可以從靜脈注射營養中受益匪淺,確保獲得足夠的營養以進行康復。

按最終用途分類,醫院和診所佔據市場主導地位,2024 年的收入佔有率為 58.8%。這些機構嚴重依賴靜脈注射液進行重症監護、手術、創傷管理和水合療法。慢性病盛行率的不斷上升和醫療基礎設施的進步進一步促進了採用。此外,診所也擴大了靜脈注射療法在治療慢性病和短期治療的應用。

在北美,靜脈注射溶液市場正在快速擴張,預計到 2034 年美國市場規模將達到 106 億美元。不斷成長的醫療保健需求、確保產品品質的嚴格 FDA 法規以及先進靜脈注射溶液的高採用率促進了市場成長。隨著靜脈注射療法的不斷進步和人們日益認知到其益處,未來幾年市場將迎來大幅擴張。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 營養不良病例不斷增加

- 早產率高

- 胃腸道疾病、神經系統疾病、癌症等疾病的發生率不斷上升

- 外科手術數量不斷增加

- 產業陷阱與挑戰

- 嚴格的監管和品質要求

- 成長動力

- 成長潛力分析

- 監管格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 完全腸外營養

- 周邊腸外營養

第6章:市場估計與預測:依構成,2021 年至 2034 年

- 主要趨勢

- 碳水化合物

- 維生素和礦物質

- 單劑量胺基酸

- 腸外脂肪乳劑

- 其他作品

第7章:市場估計與預測:依年齡層,2021 年至 2034 年

- 主要趨勢

- 兒科

- 成年人

- 老年

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 營養支持

- 輸血

- 液體和電解質平衡

- 其他應用

第9章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院和診所

- 門診手術中心

- 居家照護環境

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- AdvaCare Pharma

- Amanta Healthcare

- Axa Parenterals

- B. Braun

- Baxter International

- Fresenius Kabi

- Grifols

- ICU Medical

- JW Life Science

- Otsuka Pharmaceutical

The Global Intravenous Solutions Market, valued at USD 13.9 billion in 2024, is projected to expand at a CAGR of 8% from 2025 to 2034. Intravenous (IV) solutions are sterile liquids administered directly into a patient's bloodstream to maintain hydration, deliver medications, and supply essential nutrients. Demand for IV solutions is rising due to increasing malnutrition, the prevalence of chronic diseases, and food insecurity. A significant portion of the global population struggles with inadequate nutrition, fueling the need for IV solutions. Additionally, the growing use of IV fluids in neonatal and pediatric care is linked to the high incidence of preterm births, which require specialized nutritional support. Hospitals and healthcare facilities worldwide continue to integrate IV solutions into patient care for hydration therapy, nutrient replenishment, and post-surgical recovery.

The market is divided by type into total parenteral nutrition and peripheral parenteral nutrition (PPN). In 2024, the PPN segment dominated the market, reaching USD 8.4 billion in revenue. PPN is a preferred method for short-term nutritional support, supplying vital nutrients such as dextrose, amino acids, and lipids through peripheral veins. It helps maintain nutritional balance, prevents deficiencies, and supports patients with limited oral intake. Research suggests that timely PPN administration reduces the risk of infections and metabolic complications, making it a crucial component in modern medical treatments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.9 Billion |

| Forecast Value | $29.6 Billion |

| CAGR | 8% |

Segmented by composition, the market includes vitamins and minerals, carbohydrates, single-dose amino acids, parenteral lipid emulsions, and other essential compounds. The carbohydrates segment accounted for 40.6% of total market revenue in 2024 and is expected to reach USD 12.2 billion by 2034. Dextrose-based IV solutions are widely used to provide caloric support to critically ill patients who cannot receive nutrition through conventional means. These solutions play a key role in maintaining metabolic stability, preventing muscle breakdown, and aiding recovery. Clinical studies support the effectiveness of carbohydrate-based IV solutions in improving patient outcomes, especially in postoperative and trauma care.

By age group, the geriatric population accounted for the highest market share, representing 48.8% of total revenue in 2024. Older adults are highly susceptible to dehydration due to reduced thirst sensation, mobility challenges, and various health conditions. IV solutions ensure effective hydration and nutrient delivery, preventing complications linked to chronic illnesses. The aging global population further drives demand, with healthcare providers increasingly relying on IV therapy for elderly patients with swallowing difficulties or gastrointestinal disorders.

In terms of application, the market is segmented into nutritional support, blood transfusion, and fluid and electrolyte balance. The nutritional support segment led the market in 2024, generating USD 6.2 billion in revenue. The rising incidence of malnutrition, chronic diseases, and post-surgical recovery needs, contribute to this growth. Patients with gastrointestinal disorders or conditions affecting nutrient absorption benefit significantly from IV-administered nutrition, ensuring adequate nourishment for recovery.

By end use, hospitals and clinics dominated the market, holding a 58.8% revenue share in 2024. These facilities rely heavily on IV solutions for critical care, surgeries, trauma management, and hydration therapy. The increasing prevalence of chronic diseases and advancements in healthcare infrastructure further boost adoption. Additionally, clinics have expanded their use of IV therapy for managing chronic conditions and short-term treatments.

In North America, the intravenous solutions market is witnessing rapid expansion, with the US projected to reach USD 10.6 billion by 2034. Rising healthcare demands, stringent FDA regulations ensuring product quality, and high adoption rates of advanced IV solutions contribute to market growth. With ongoing advancements and increasing awareness of IV therapy's benefits, the market is poised for significant expansion in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing cases of malnutrition

- 3.2.1.2 High prevalence of pre-term births

- 3.2.1.3 Increasing prevalence of diseases, such as gastrointestinal disorder, neurological diseases, and cancer

- 3.2.1.4 Increasing number of surgical procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory and quality requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Total parenteral nutrition

- 5.3 Peripheral parenteral nutrition

Chapter 6 Market Estimates and Forecast, By Composition, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Carbohydrates

- 6.3 Vitamins and minerals

- 6.4 Single-dose amino acids

- 6.5 Parenteral lipid emulsion

- 6.6 Other compositions

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

- 7.4 Geriatric

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Nutritional support

- 8.3 Blood transfusion

- 8.4 Fluid and electrolyte balance

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgery centers

- 9.4 Home care settings

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AdvaCare Pharma

- 11.2 Amanta Healthcare

- 11.3 Axa Parenterals

- 11.4 B. Braun

- 11.5 Baxter International

- 11.6 Fresenius Kabi

- 11.7 Grifols

- 11.8 ICU Medical

- 11.9 JW Life Science

- 11.10 Otsuka Pharmaceutical

全球靜脈輸液市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球靜脈輸液市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 日本靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年

日本靜脈輸液市場規模、佔有率、趨勢和預測:按類型、營養成分和地區分類,2026-2034年 靜脈輸液市場規模、佔有率和成長分析(按產品、營養成分和地區分類)—產業預測(2026-2033 年)

靜脈輸液市場規模、佔有率和成長分析(按產品、營養成分和地區分類)—產業預測(2026-2033 年) 靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分、最終用途、地區和細分市場預測(2026-2033 年)

靜脈輸液市場規模、佔有率和趨勢分析報告:按類型、營養成分、最終用途、地區和細分市場預測(2026-2033 年) 林格氏液:2025-2031年全球市佔率與排名、總收入與需求預測

林格氏液:2025-2031年全球市佔率與排名、總收入與需求預測 輸液解決方案市場按產品類型、最終用戶、應用、分銷管道和包裝類型分類-2025-2032 年全球預測

輸液解決方案市場按產品類型、最終用戶、應用、分銷管道和包裝類型分類-2025-2032 年全球預測 全球藥用級氯化鉀市場:依通路、應用和地區(~2035年)

全球藥用級氯化鉀市場:依通路、應用和地區(~2035年) 靜脈輸液市場:市場規模、佔有率、前景、按解決方案、輸液袋類型、應用、最終用戶和地區分類的機會分析,2025 年至 2032 年靜脈注射液市場規模、佔有率、趨勢及預測(按類型、營養成分及地區分類),2025 年至 2033 年美國靜脈注射注射液市場規模、佔有率、趨勢分析報告:按產品、營養、最終用途、細分市場預測,2025-2030 年

靜脈輸液市場:市場規模、佔有率、前景、按解決方案、輸液袋類型、應用、最終用戶和地區分類的機會分析,2025 年至 2032 年靜脈注射液市場規模、佔有率、趨勢及預測(按類型、營養成分及地區分類),2025 年至 2033 年美國靜脈注射注射液市場規模、佔有率、趨勢分析報告:按產品、營養、最終用途、細分市場預測,2025-2030 年