|

市場調查報告書

商品編碼

1698509

電子製造服務市場機會、成長動力、產業趨勢分析及 2025-2034 年預測Electronic Manufacturing Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

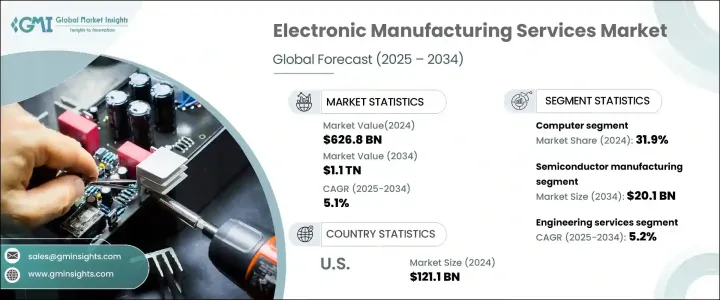

全球電子製造服務市場規模到 2024 年將達到 6,268 億美元,預計在 2025 年至 2034 年期間的複合年成長率將達到 5.1%,這主要得益於技術的快速進步和各行各業需求的不斷成長。這種上升趨勢的動力來自於消費性電子產品的激增、物聯網 (IoT) 的廣泛應用以及汽車、醫療保健和計算等行業對複雜電子元件的日益依賴。該公司正在大力投資自動化、人工智慧 (AI) 和機器人技術,以增強生產能力、提高效率並滿足不斷變化的效能期望。

電動車(EV)的日益普及是 EMS 市場成長的主要催化劑。電動車需要先進的電子元件,例如電池管理系統、電力電子系統、馬達控制器和資訊娛樂系統。隨著對這些車輛的需求不斷成長,製造商正在增加產量並採用尖端技術以滿足嚴格的性能和永續性要求。汽車電子創新的推動導致對高科技製造解決方案的大量投資,使 EMS 供應商能夠提供更有效率、更可靠的組件。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 6268億美元 |

| 預測值 | 1.1兆美元 |

| 複合年成長率 | 5.1% |

EMS 市場分為幾個主要部分,包括電子製造、工程服務、測試和開發實施、物流服務等。其中,電子製造業在2024年創造了3,765億美元的收入,由於對小型化、高性能設備和永續生產實踐的需求不斷成長,仍保持主導地位。公司正在整合先進的自動化和人工智慧驅動的品質控制,以最佳化製造流程、提高成本效率並滿足現代消費性電子和汽車應用的嚴格要求。

EMS 市場的應用範圍涵蓋消費性電子、航太、汽車、醫療設備和半導體製造,並不斷發展以滿足這些不同領域的需求。 2024 年,電腦領域佔據 31.9% 的市場佔有率,佔據領先地位,反映出對高效能運算系統和小型化元件的需求不斷成長。隨著人工智慧驅動的技術和數據密集型應用的普及,製造商正專注於精確、經濟高效的生產技術,以支援下一代運算解決方案。

2024 年,北美佔據 EMS 市場的 21.5% 佔有率,電子、汽車和醫療保健領域的進步推動了強勁成長。該地區的公司優先考慮高科技製造、永續性以及物聯網、電動車和自動化等下一代技術,以確保競爭優勢。該地區對研發 (R&D) 和持續創新的承諾進一步鞏固了其作為全球 EMS 行業關鍵參與者的地位。隨著對先進生產技術和策略合作的投資不斷增加,北美製造商有望推動電子製造服務的未來。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 消費性電子產品需求不斷成長

- 電動車(EV)的普及率不斷提高

- 智慧型設備和物聯網的普及率不斷提高

- 半導體產業的成長

- 國防和航太電子需求不斷成長

- 產業陷阱與挑戰

- 初期投資要求高

- 供應鏈管理的複雜性

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 電子製造業

- PCB組裝

- 電纜組件

- 機電組裝/箱體構建

- 測試

- 原型設計

- 其他

- 工程服務

- 電路設計

- PCB 佈局

- 其他

- 測試與開發實施

- 電路組裝測試

- 完全組裝的單元測試

- 其他

- 物流服務

- 庫存管理

- 再製造

- 其他

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 電腦

- 消費性電子產品

- 航太與國防

- 醫療保健

- 汽車

- 半導體製造

- 機器人技術

- 農業

- 電力與能源

- 其他

第7章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第8章:公司簡介

- ASE TECHNOLOGY HOLDING

- All Shore Industries, Inc.

- Celestica Inc.

- Compal Electronics, Inc.

- Delta Group Electronics, Inc.

- Fabrinet

- FLEX LTD

- Foxconn (Hon Hai Precision Industry Co., Ltd.)

- Integrated Micro-Electronics, Inc.

- Inventec

- Jabil Inc.

- Kimball Electronics, Inc.

- Plexus Corp.

- Quanta Computer lnc

- Sanmina Corporation

- Shenzhen Kinwong Electronic Co., Ltd.

- TPV Technology Co., Ltd.

- VIRTEX (Formerly Altron Inc)

- Wistron Corporation

The Global Electronic Manufacturing Services Market, valued at USD 626.8 billion in 2024, is set to expand at a CAGR of 5.1% from 2025 to 2034, driven by rapid advancements in technology and increasing demand across various industries. This upward trajectory is fueled by the surge in consumer electronics, the widespread adoption of the Internet of Things (IoT), and the growing reliance on sophisticated electronic components across industries such as automotive, healthcare, and computing. Companies are heavily investing in automation, artificial intelligence (AI), and robotics to enhance production capabilities, improve efficiency, and meet evolving performance expectations.

The increasing adoption of electric vehicles (EVs) is a major catalyst for EMS market growth. EVs require advanced electronic components such as battery management systems, power electronics, motor controllers, and infotainment systems. As demand for these vehicles rises, manufacturers are ramping up production and incorporating cutting-edge technologies to meet stringent performance and sustainability requirements. The push for innovation in automotive electronics is leading to significant investments in high-tech manufacturing solutions, allowing EMS providers to deliver more efficient and reliable components.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $626.8 Billion |

| Forecast Value | $1.1 Trillion |

| CAGR | 5.1% |

The EMS market is categorized into several key segments, including electronic manufacturing, engineering services, test and development implementation, logistics services, and others. Among these, the electronic manufacturing segment generated USD 376.5 billion in 2024, maintaining its dominant position due to the rising need for miniaturization, high-performance devices, and sustainable production practices. Companies are integrating advanced automation and AI-driven quality control to optimize manufacturing processes, enhance cost efficiency, and meet the stringent requirements of modern consumer electronics and automotive applications.

With applications spanning consumer electronics, aerospace, automotive, medical devices, and semiconductor manufacturing, the EMS market continues to evolve to meet the needs of these diverse sectors. The computer segment led with a 31.9% market share in 2024, reflecting the increasing demand for high-performance computing systems and miniaturized components. As AI-driven technologies and data-intensive applications gain traction, manufacturers are focusing on precise, cost-effective production techniques to support the next generation of computing solutions.

North America accounted for a 21.5% share of the EMS market in 2024, with strong growth driven by advancements in the electronics, automotive, and healthcare sectors. Companies in the region are prioritizing high-tech manufacturing, sustainability, and next-generation technologies such as IoT, electric vehicles, and automation to secure a competitive edge. The region's commitment to research and development (R&D) and continuous innovation further solidifies its position as a key player in the global EMS industry. With increasing investments in advanced production techniques and strategic collaborations, North American manufacturers are poised to drive the future of electronic manufacturing services.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for consumer electronics

- 3.2.1.2 Growing adoption of electric vehicles (EVs)

- 3.2.1.3 Rising adoption of smart devices and IoT

- 3.2.1.4 Growth of the semiconductor industry

- 3.2.1.5 Rising defense and aerospace electronics needs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment requirements

- 3.2.2.2 Complexity in managing supply chains

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Bn)

- 5.1 Key trends

- 5.2 Electronic manufacturing

- 5.2.1 PCB assembly

- 5.2.2 Cable assembly

- 5.2.3 Electromechanical assembly/box build

- 5.2.4 Testing

- 5.2.5 Prototyping

- 5.2.6 Others

- 5.3 Engineering services

- 5.3.1 Circuit design

- 5.3.2 PCB layout

- 5.3.3 Others

- 5.4 Test & development implementation

- 5.4.1 Circuit assembly testing

- 5.4.2 Fully assembled unit testing

- 5.4.3 Others

- 5.5 Logistics services

- 5.5.1 Inventory management

- 5.5.2 Remanufacturing

- 5.5.3 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Bn)

- 6.1 Key trends

- 6.2 Computer

- 6.3 Consumer electronics

- 6.4 Aerospace & defense

- 6.5 Medical & healthcare

- 6.6 Automotive

- 6.7 Semiconductor manufacturing

- 6.8 Robotics

- 6.9 Agriculture

- 6.10 Power & energy

- 6.11 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ASE TECHNOLOGY HOLDING

- 8.2 All Shore Industries, Inc.

- 8.3 Celestica Inc.

- 8.4 Compal Electronics, Inc.

- 8.5 Delta Group Electronics, Inc.

- 8.6 Fabrinet

- 8.7 FLEX LTD

- 8.8 Foxconn (Hon Hai Precision Industry Co., Ltd.)

- 8.9 Integrated Micro-Electronics, Inc.

- 8.10 Inventec

- 8.11 Jabil Inc.

- 8.12 Kimball Electronics, Inc.

- 8.13 Plexus Corp.

- 8.14 Quanta Computer lnc

- 8.15 Sanmina Corporation

- 8.16 Shenzhen Kinwong Electronic Co., Ltd.

- 8.17 TPV Technology Co., Ltd.

- 8.18 VIRTEX (Formerly Altron Inc)

- 8.19 Wistron Corporation

電子製造服務 (EMS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、零件、應用、製程、最終用戶、解決方案和階段分類

電子製造服務 (EMS) 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、零件、應用、製程、最終用戶、解決方案和階段分類 電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球綠色電子製造市場報告

2026年全球綠色電子製造市場報告 綠色電子製造市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、服務、產業、地區及競爭格局分類,2021-2031年)電子製造服務市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、產業、地區和競爭格局分類,2021-2031年

綠色電子製造市場-全球產業規模、佔有率、趨勢、機會及預測(依技術、服務、產業、地區及競爭格局分類,2021-2031年)電子製造服務市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、產業、地區和競爭格局分類,2021-2031年 電子製造服務 (EMS) 市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測 (2026-2034)

電子製造服務 (EMS) 市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測 (2026-2034) EMS和ODM市場規模、佔有率和成長分析(按類型、應用和地區分類)-產業預測(2026-2033年)電子製造服務 (EMS) 和原始設計製造商 (ODM) 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(電子製造服務、原始設計製造商)、應用、地區和競爭格局分類,2020-2030 年預測

EMS和ODM市場規模、佔有率和成長分析(按類型、應用和地區分類)-產業預測(2026-2033年)電子製造服務 (EMS) 和原始設計製造商 (ODM) 市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型(電子製造服務、原始設計製造商)、應用、地區和競爭格局分類,2020-2030 年預測 全球EMS和ODM市場依類型、應用和地區劃分(2032年)

全球EMS和ODM市場依類型、應用和地區劃分(2032年) 電子製造服務市場(按服務類型、技術和應用)—全球預測,2025-2032

電子製造服務市場(按服務類型、技術和應用)—全球預測,2025-2032