|

市場調查報告書

商品編碼

1698339

人工智慧在電信市場的機會、成長動力、產業趨勢分析以及 2025 - 2034 年預測AI in Telecommunication Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

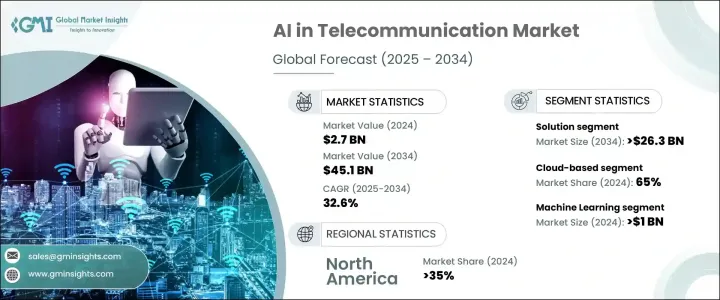

2024 年全球電信人工智慧市場價值為 27 億美元,預計 2025 年至 2034 年期間的複合年成長率將達到 32.6%。人工智慧驅動的解決方案正在徹底改變電信業的網路營運、客戶服務和基礎設施管理。人工智慧與電信網路和 5G 技術的融合增強了自動化、即時分析和異常檢測能力。借助人工智慧,頻譜控制得到改善,確保最佳化頻寬管理並減少高流量區域的延遲。人工智慧驅動的詐欺偵測系統可以降低網路安全風險,幫助電信供應商保護其網路和財務。人工智慧也在改變客戶互動方式,因為聊天機器人和數位助理簡化了回應並減少了人工干預的需要。人工智慧驅動的自然語言處理 (NLP) 工具可以自動解決問題,提高客戶滿意度,同時降低營運成本。

市場根據組件細分為解決方案和服務。解決方案部分的價值在 2024 年為 17 億美元,預計到 2034 年將超過 263 億美元。人工智慧廣泛應用於業務流程自動化、詐欺偵測和網路效能監控,從而提高整個電信營運的效率和安全性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 27億美元 |

| 預測值 | 451億美元 |

| 複合年成長率 | 32.6% |

電信業者依靠人工智慧驅動的詐欺偵測工具來對抗安全威脅。機器學習演算法自動偵測並防止詐欺活動,確保遵守監管標準,同時最大限度地減少財務損失。人工智慧驅動的自動化加強了服務回應,提高了網路的安全性和可靠性。

借助人工智慧聊天機器人和虛擬助手,電信業的客戶服務得到了顯著改善。透過使用 NLP 實現服務自動化,電信公司可以更快地處理查詢並解決問題,而無需人工干預。這種自動化不僅降低了成本,還增強了品牌忠誠度。人工智慧還可以透過學習過去的互動來個性化回應並提高服務質量,在簡化客戶互動方面發揮至關重要的作用。

根據部署模式,市場進一步細分為基於雲端的解決方案和內部部署的解決方案。基於雲端的人工智慧在 2024 年佔據主導地位,佔有 65% 的佔有率,預計在整個預測期內將大幅成長。雲端運算的可擴展性、靈活性和成本效益使電信供應商無需大量基礎設施投資即可整合人工智慧,從而加速整個產業的採用。

對於處理敏感客戶資料的電信公司來說,私人 AI 實施仍然是首選,可確保更好地控制安全性、合規性和資料隱私。許多電信公司正在部署私有人工智慧模型,以遵守行業特定的法規並提高網路效率。

人工智慧即服務 (AIaaS) 在電信營運商中越來越受歡迎,它無需內部開發團隊即可提供數據驅動的洞察。 2024 年 AIaaS 市值為 97 億美元,預計到 2032 年複合年成長率將超過 33%。這種模式使小型電信公司能夠以較低的成本利用人工智慧驅動的商業智慧解決方案。

人工智慧驅動的邊緣運算透過在網路邊緣實現即時資料處理來最佳化網路效能。這項創新減少了延遲,改善了頻寬管理,並確保即使在高峰流量負載下也能無縫運行,從而增強了行動和寬頻服務。

電信市場的人工智慧按應用細分,包括機器學習、NLP 和深度學習。機器學習領域價值到 2024 年將超過 10 億美元,因其在預測性維護、網路最佳化和詐欺檢測中的作用而佔據主導地位。基於人工智慧的機器學習模型可協助電信公司減少網路故障,進而提高服務可靠性。

NLP 正在改變客戶服務自動化,它允許 AI 系統根據先前的互動來分析和回應用戶查詢,從而提高保留率。 2023 年 NLP 市場價值為 55 億美元,預計 2024 年至 2032 年將成長 25% 以上。

深度學習擴大用於語音識別和自動呼叫路由,從而實現更有效率的客戶服務營運。人工智慧驅動的語音轉文本解決方案提高了殘疾人的可訪問性,同時增強了電信系統內的內容索引和檢索。

人工智慧自動化還透過監控系統效能、預測故障和分配資源來最大限度地提高效率,從而改善電信網路管理。預計到 2028 年,智慧型手機用戶數量將達到 77 億,凸顯了對人工智慧電信解決方案日益成長的需求。

北美在電信市場的人工智慧領域處於領先地位,到 2024 年將佔據 35% 以上的佔有率。美國仍處於領先地位,其主要

目錄

第1章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究與驗證

- 主要來源

- 資料探勘來源

- 市場定義

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 平台提供者

- 技術整合商

- 經銷商

- 最終用途

- 利潤率分析

- 技術與創新格局

- 重要新聞和舉措

- 已使用案例

- 使用案例 1

- 好處

- 投資報酬率

- 使用案例 2

- 好處

- 投資報酬率

- 使用案例 1

- 案例研究

- 案例研究 1

- 消費者姓名

- 挑戰

- 解決方案

- 影響

- 案例研究 1

- 消費者姓名

- 挑戰

- 解決方案

- 影響

- 案例研究 1

- 價格趨勢分析

- 專利分析

- 監管格局

- 衝擊力

- 成長動力

- 網路自動化和客戶服務領域人工智慧應用日益增多

- 人工智慧與5G技術的融合

- 電信業對預測分析的需求不斷增加

- 擴展人工智慧驅動的網路安全解決方案

- 產業陷阱與挑戰

- 資料隱私和安全問題

- 初期投資成本高

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 解決方案

- 服務

第6章:市場估計與預測:依部署模型,2021 - 2034 年

- 主要趨勢

- 本地

- 基於雲端

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 機器學習(ML)

- 自然語言處理(NLP)

- 深度學習

- 其他

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 網路最佳化

- 網路安全

- 客戶分析

- 虛擬助手

- 詐欺偵測

- 預測性維護

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- Accenture

- Amazon Web Services (AWS)

- Amdocs

- AT&T

- Baidu

- Cisco Systems

- Ericsson

- Hewlett Packard Enterprise (HPE)

- IBM

- Intel

- Microsoft

- NEC

- Nokia

- NVIDIA

- Oracle

- Qualcomm

- Salesforce

- Samsung Electronics

- ZTE

The Global AI In Telecommunication Market, valued at USD 2.7 billion in 2024, is on track to expand at a CAGR of 32.6% from 2025 to 2034. AI-driven solutions are revolutionizing network operations, customer service, and infrastructure management within the telecom industry. The integration of AI with telecom networks and 5G technology enhances automation, real-time analysis, and anomaly detection. With AI, spectrum control improves, ensuring optimized bandwidth management and reduced latency in high-traffic areas. AI-powered fraud detection systems mitigate cybersecurity risks, helping telecom providers safeguard their networks and finances. AI is also transforming customer interactions, as chatbots and digital assistants streamline responses and reduce the need for human intervention. AI-driven natural language processing (NLP) tools allow for automated issue resolution, enhancing customer satisfaction while cutting operational costs.

The market is segmented based on components into solutions and services. The solutions segment, valued at USD 1.7 billion in 2024, is projected to surpass USD 26.3 billion by 2034. AI is widely applied in business process automation, fraud detection, and network performance monitoring, increasing efficiency and security across telecom operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $45.1 Billion |

| CAGR | 32.6% |

Telecom providers rely on AI-powered fraud detection tools to combat security threats. Machine learning algorithms automatically detect and prevent fraudulent activities, ensuring compliance with regulatory standards while minimizing financial losses. AI-driven automation strengthens service response, improving network security and reliability.

Customer service within the telecom sector has seen significant improvements with AI-powered chatbots and virtual assistants. By automating services using NLP, telecom companies handle inquiries faster and resolve issues without human intervention. This automation not only reduces costs but also strengthens brand loyalty. AI also plays a crucial role in streamlining customer interactions by learning from past engagements to personalize responses and improve service quality.

The market is further segmented by deployment models into cloud-based and on-premises solutions. Cloud-based AI dominated with a 65% share in 2024 and is expected to grow substantially throughout the forecast period. The scalability, flexibility, and cost efficiency of cloud computing enable telecom providers to integrate AI without heavy infrastructure investments, accelerating adoption across the industry.

Private AI implementations remain a preferred choice for telecom companies handling sensitive customer data, ensuring better control over security, compliance, and data privacy. Many telecom firms are deploying private AI models to adhere to industry-specific regulations and enhance network efficiency.

AI-as-a-Service (AIaaS) is gaining traction among telecom operators, providing access to data-driven insights without the need for in-house development teams. The AIaaS market, valued at USD 9.7 billion in 2024, is expected to grow at a CAGR of over 33% through 2032. This model allows smaller telecom firms to leverage AI-driven business intelligence solutions at reduced costs.

AI-driven edge computing is optimizing network performance by enabling real-time data processing at the network edge. This innovation reduces latency, improves bandwidth management, and ensures seamless operations even during peak traffic loads, enhancing mobile and broadband services.

The AI in telecommunication market is segmented by applications, including machine learning, NLP, and deep learning. The machine learning segment, valued at over USD 1 billion in 2024, dominates due to its role in predictive maintenance, network optimization, and fraud detection. AI-based machine learning models help telecom companies improve service reliability by reducing network failures.

NLP is transforming customer service automation by allowing AI systems to analyze and respond to user queries based on previous interactions, leading to higher retention rates. The NLP market, valued at USD 5.5 billion in 2023, is expected to grow over 25% from 2024 to 2032.

Deep learning is increasingly used for speech recognition and automated call routing, enabling more efficient customer service operations. AI-driven speech-to-text solutions improve accessibility for people with disabilities while enhancing content indexing and retrieval within telecom systems.

AI automation is also improving administrative telecom network management by monitoring system performance, predicting failures, and allocating resources to maximize efficiency. The rise in smartphone users, projected to reach 7.7 billion by 2028, highlights the growing need for AI-powered telecom solutions.

North America leads the AI in telecommunication market, holding over 35% of the share in 2024. The US remains at the forefront, with major t

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Platform provider

- 3.2.2 Technology integrators

- 3.2.3 Distributors

- 3.2.4 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Used cases

- 3.6.1 Used case 1

- 3.6.1.1 Benefits

- 3.6.1.2 ROI

- 3.6.2 Used case 2

- 3.6.2.1 Benefits

- 3.6.2.2 ROI

- 3.6.1 Used case 1

- 3.7 Case study

- 3.7.1 Case study 1

- 3.7.1.1 Consumer name

- 3.7.1.2 Challenge

- 3.7.1.3 Solution

- 3.7.1.4 Impact

- 3.7.2 Case study 1

- 3.7.2.1 Consumer name

- 3.7.2.2 Challenge

- 3.7.2.3 Solution

- 3.7.2.4 Impact

- 3.7.1 Case study 1

- 3.8 Pricing trend analysis

- 3.9 Patent analysis

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising AI adoption for network automation and customer service

- 3.11.1.2 Integration of AI with 5G technology

- 3.11.1.3 Increasing demand for predictive analytics in telecom

- 3.11.1.4 Expansion of AI-driven cybersecurity solutions

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Data privacy and security concerns

- 3.11.2.2 High initial investment costs

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Machine Learning (ML)

- 7.3 Natural Language Processing (NLP)

- 7.4 Deep Learning

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Network optimization

- 8.3 Network security

- 8.4 Customer analytics

- 8.5 Virtual assistants

- 8.6 Fraud detection

- 8.7 Predictive maintenance

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Accenture

- 10.2 Amazon Web Services (AWS)

- 10.3 Amdocs

- 10.4 AT&T

- 10.5 Baidu

- 10.6 Cisco Systems

- 10.7 Ericsson

- 10.8 Google

- 10.9 Hewlett Packard Enterprise (HPE)

- 10.10 IBM

- 10.11 Intel

- 10.12 Microsoft

- 10.13 NEC

- 10.14 Nokia

- 10.15 NVIDIA

- 10.16 Oracle

- 10.17 Qualcomm

- 10.18 Salesforce

- 10.19 Samsung Electronics

- 10.20 ZTE

2026年雲端通訊人工智慧(AI)全球市場報告

2026年雲端通訊人工智慧(AI)全球市場報告 通訊OSS/BSS市場預測至2034年-按組件、部署模式、營運商類型、網路類型、架構、最終用戶和地區分類的全球分析

通訊OSS/BSS市場預測至2034年-按組件、部署模式、營運商類型、網路類型、架構、最終用戶和地區分類的全球分析 通訊產業人工智慧(AI)市場規模、佔有率和成長分析:按組件、部署模式、應用和地區分類-2026-2033年產業預測

通訊產業人工智慧(AI)市場規模、佔有率和成長分析:按組件、部署模式、應用和地區分類-2026-2033年產業預測 通訊領域人工智慧市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、技術、應用、部署類型、地區和競爭格局分類,2021-2031年2034年通訊產業人工智慧市場預測-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析

通訊領域人工智慧市場-全球產業規模、佔有率、趨勢、機會和預測:按組件、技術、應用、部署類型、地區和競爭格局分類,2021-2031年2034年通訊產業人工智慧市場預測-按組件、部署模式、組織規模、技術、應用、最終用戶和地區分類的全球分析 通訊領域人工智慧市場:依技術、組件、應用、部署模式和企業規模分類-2026-2032年全球市場預測

通訊領域人工智慧市場:依技術、組件、應用、部署模式和企業規模分類-2026-2032年全球市場預測 印尼電信:通訊業自動化、人工智慧和高階網路案例研究

印尼電信:通訊業自動化、人工智慧和高階網路案例研究 AMD公司:GPU、APU、DPU和AI網卡的全球部署狀況2026年全球通訊領域生成式人工智慧市場報告2026年全球人工智慧(AI)光纖網路控制器市場報告

AMD公司:GPU、APU、DPU和AI網卡的全球部署狀況2026年全球通訊領域生成式人工智慧市場報告2026年全球人工智慧(AI)光纖網路控制器市場報告