|

市場調查報告書

商品編碼

1685064

帶嘴和不帶嘴液體袋包裝市場機會、成長動力、產業趨勢分析和 2025 - 2034 年預測Spout and Non-Spout Liquid Pouch Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

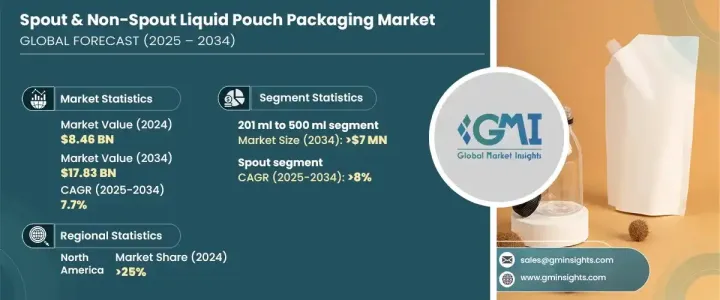

2024 年全球帶嘴和非帶嘴液體袋包裝市場價值為 84.6 億美元,預計 2025 年至 2034 年期間的複合年成長率為 7.7%。對靈活、輕巧、節省空間的包裝解決方案的需求不斷成長,推動了這一擴張。隨著消費者尋求方便、便攜和可重新密封的包裝選擇,企業正在轉向具有成本效益且高效的硬質容器替代品。人們對永續性的日益關注進一步加速了市場的成長,製造商紛紛投資可回收和可生物分解的包裝袋,以符合不斷變化的環境法規和消費者偏好。

電子商務的興起在推動液體袋需求方面發揮了至關重要的作用,因為它們具有耐用性、防溢出性和降低運輸成本的特性。這些包裝解決方案對食品和飲料、個人護理和家用產品等行業特別有吸引力,因為功能性和便利性是這些行業的首要任務。單份和攜帶式包裝形式的日益普及也推動了成長,迎合了尋求易於使用選擇的忙碌消費者的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 84.6億美元 |

| 預測值 | 178.3億美元 |

| 複合年成長率 | 7.7% |

技術進步正在改變市場,各公司專注於創新材料設計,以增強液體袋的強度、柔韌性和阻隔性。2D碼袋和溫度敏感標籤等智慧包裝解決方案正日益受到關注,提高了消費者參與度和產品安全性。此外,成本效益高的製造技術和生產自動化使液體袋包裝成為尋求最佳化供應鏈的企業的首選。

按容量分類,市場分為 200 毫升以下、201 毫升至 500 毫升、501 毫升至 1 公升以及 1 公升以上。由於多個行業的廣泛應用,201 毫升至 500 毫升細分市場預計到 2034 年將創收 700 萬美元。此容量範圍實現了便攜性和實用性的完美平衡,非常適合包裝飲料、醬汁、個人護理用品和家用液體。其緊湊的尺寸吸引了追求便利性的消費者,同時也確保了製造商高效的儲存和運輸。滿足各種應用的能力增強了其市場地位。

根據類型,市場還分為帶嘴包裝和不帶嘴包裝。吸嘴袋市場預計將實現最高成長,2025 年至 2034 年之間的複合年成長率為 8%。吸嘴袋因其可控分配和可重新密封的特點而越來越受歡迎,具有增強的功能性和便利性。它們能夠最大限度地減少產品浪費,同時確保易於使用,這使得它們成為液體包裝的理想選擇。這些袋子廣泛用於飲料、調味品和個人護理用品,特別是在防溢出和便攜性至關重要的地方。對一次性和旅行友善包裝的需求不斷成長是推動該領域擴張的重要因素。

2024 年北美佔 25% 的市場佔有率,其中美國需求強勁。消費者對環保和便利包裝的偏好繼續推動該地區的成長。支持永續材料和可回收包裝的監管措施進一步增強了市場。散裝包裝的日益普及和電子商務的擴張增加了對耐用、防溢液體袋的需求。成本效益生產技術的創新使液體袋包裝成為希望提高營運效率同時降低運輸成本的企業的一個有吸引力的選擇。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 方便包裝需求不斷成長

- 永續性和減少材料使用

- 大容量包裝的創新

- 電子商務和快速消費品的成長

- 成本效益和客製化

- 產業陷阱與挑戰

- 回收的複雜性

- 產品完整性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 噴口

- 無噴口

第6章:市場估計與預測:依產能,2021-2034

- 主要趨勢

- 最多 200 毫升

- 201 毫升至 500 毫升

- 501 毫升至 1 公升

- 1公升以上

第 7 章:市場估計與預測:按層壓板,2021 年至 2034 年

- 主要趨勢

- 兩層

- 三層

- 四層

- 其他

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 食品和飲料

- 果汁和飲料

- 醬汁和調味品

- 乳製品

- 工業的

- 油和潤滑劑

- 化學品

- 個人護理

- 液體肥皂

- 洗髮精和護髮素

- 居家護理

- 清潔劑

- 清潔解決方案

- 製藥

- 乳霜和凝膠

- 糖漿

第 9 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Amcor

- Ampac

- Cellpack Packaging

- Chengde

- Constantia Flexibles

- Glenroy

- Huhtamaki

- Impak Corporation

- Pouch Makers CA

- Smart Pouches

- Smurfit Kappa

- Sonoco

- Swiss Pac

- Tetra Pak

- Uflex

The Global Spout And Non-Spout Liquid Pouch Packaging Market was valued at USD 8.46 billion in 2024 and is expected to grow at a CAGR of 7.7% between 2025 and 2034. The increasing demand for flexible, lightweight, and space-efficient packaging solutions is driving this expansion. As consumers seek convenient, portable, and resealable packaging options, businesses are shifting toward cost-effective and efficient alternatives to rigid containers. The growing focus on sustainability has further accelerated market growth, with manufacturers investing in recyclable and biodegradable pouches to align with evolving environmental regulations and consumer preferences.

The rise of e-commerce has played a crucial role in boosting demand for liquid pouches, as they offer durability, spill resistance, and reduced shipping costs. These packaging solutions are particularly appealing to industries such as food and beverage, personal care, and household products, where functionality and convenience are top priorities. The increasing adoption of single-serve and on-the-go packaging formats has also fueled growth, catering to busy consumers looking for easy-to-use options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.46 Billion |

| Forecast Value | $17.83 Billion |

| CAGR | 7.7% |

Technological advancements are transforming the market, with companies focusing on innovative material designs that enhance the strength, flexibility, and barrier properties of liquid pouches. Smart packaging solutions, such as QR-coded pouches and temperature-sensitive labels, are gaining traction, improving consumer engagement and product safety. Additionally, cost-efficient manufacturing techniques and automation in production are making liquid pouch packaging a preferred choice for businesses looking to optimize their supply chains.

The market is segmented by capacity into up to 200 ml, 201 ml to 500 ml, 501 ml to 1 liter, and above 1 liter. The 201 ml to 500 ml segment is projected to generate USD 7 million by 2034, driven by its widespread adoption across multiple industries. This capacity range provides the perfect balance of portability and practicality, making it ideal for packaging beverages, sauces, personal care items, and household liquids. Its compact size appeals to consumers looking for convenience while ensuring efficient storage and transportation for manufacturers. The ability to cater to various applications strengthens its market prominence.

The market is also categorized by type into spout and non-spout packaging. The spout segment is set to register the highest growth, with a CAGR of 8% between 2025 and 2034. Spout pouches are becoming increasingly popular due to their controlled dispensing and resealable features, offering enhanced functionality and convenience. Their ability to minimize product waste while ensuring ease of use makes them highly desirable for liquid packaging. These pouches are widely utilized for beverages, condiments, and personal care items, especially where spill prevention and portability are essential. The rising demand for single-use and travel-friendly packaging is a significant factor driving the expansion of this segment.

North America accounted for a 25% share of the market in 2024, with strong demand in the United States. Consumer preference for eco-friendly and convenient packaging continues to drive growth in the region. Regulatory initiatives supporting sustainable materials and recyclable packaging further strengthen the market. The increasing popularity of bulk packaging and the expansion of e-commerce have heightened the demand for durable, spill-proof liquid pouches. Innovations in cost-efficient production technologies have made liquid pouch packaging an attractive option for businesses looking to improve operational efficiency while reducing transportation costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Key news & initiatives

- 3.3 Regulatory landscape

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Rising demand for convenience packaging

- 3.4.1.2 Sustainability and reduced material use

- 3.4.1.3 Innovation in large-capacity packaging

- 3.4.1.4 Growth in e-commerce and FMCG

- 3.4.1.5 Cost efficiency and customization

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 Recycling complexity

- 3.4.2.2 Product integrity issues

- 3.4.1 Growth drivers

- 3.5 Growth potential analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Spout

- 5.3 Non-Spout

Chapter 6 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 200 ml

- 6.3 201 ml to 500 ml

- 6.4 501 ml to 1 liter

- 6.5 Above 1 liter

Chapter 7 Market Estimates & Forecast, By Laminates, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Two layers

- 7.3 Three layers

- 7.4 Four layers

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverages

- 8.2.1 Juices & beverages

- 8.2.2 Sauces & condiments

- 8.2.3 Dairy products

- 8.3 Industrial

- 8.3.1 Oils & lubricants

- 8.3.2 Chemicals

- 8.4 Personal care

- 8.4.1 Liquid soaps

- 8.4.2 Shampoos & conditioners

- 8.5 Home care

- 8.5.1 Detergents

- 8.5.2 Cleaning solutions

- 8.6 Pharmaceutical

- 8.6.1 Creams & gels

- 8.6.2 Syrups

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amcor

- 10.2 Ampac

- 10.3 Cellpack Packaging

- 10.4 Chengde

- 10.5 Constantia Flexibles

- 10.6 Glenroy

- 10.7 Huhtamaki

- 10.8 Impak Corporation

- 10.9 Pouch Makers CA

- 10.10 Smart Pouches

- 10.11 Smurfit Kappa

- 10.12 Sonoco

- 10.13 Swiss Pac

- 10.14 Tetra Pak

- 10.15 Uflex

液體包裝袋市場規模、佔有率和成長分析(按包裝類型、材料、產品類型、容量、應用和地區分類)-2026-2033年產業預測

液體包裝袋市場規模、佔有率和成長分析(按包裝類型、材料、產品類型、容量、應用和地區分類)-2026-2033年產業預測 到 2030 年有嘴和無嘴液體袋包裝市場預測:按產品、材料、產能、分銷管道、應用和地區進行的全球分析

到 2030 年有嘴和無嘴液體袋包裝市場預測:按產品、材料、產能、分銷管道、應用和地區進行的全球分析