|

市場調查報告書

商品編碼

1684838

三相家用備用發電機組市場機會、成長動力、產業趨勢分析與預測 2025 - 2034Three Phase Home Standby Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

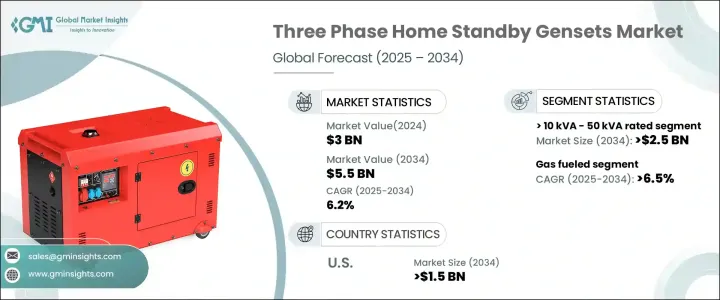

2024 年全球三相家用備用發電機組市場價值為 30 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.2%。隨著天氣相關災害發生的頻率和強度不斷增加,再加上老化電力基礎設施的脆弱性,對可靠備用電源解決方案的需求持續上升。由於颶風、冬季風暴和電網故障導致停電現象變得更加普遍,屋主將電力安全放在首位。隨著現代家庭採用更多高能耗電器和智慧家居技術,對不間斷電力供應的需求進一步推動了市場的擴張。此外,政府旨在加強住宅基礎設施的措施和家庭自動化的興起趨勢也促進了市場成長。隨著技術進步提高了發電機的效率、噪音和燃油經濟性,越來越多的屋主投資三相備用發電機組作為長期電力解決方案。

預計到 2034 年,額定功率在 >10 kVA 和 50 kVA 之間的發電機組的細分市場將產生 25 億美元的收入。這些系統被廣泛用於支援基本家庭功能,包括 HVAC 系統、家庭安全網路和其他高能耗設備。尤其是較大的房屋,依賴這些發電機組來無縫管理大量內部負載。儘管與其他備用解決方案相比,前期成本較高,但這些設備的長期可靠性和效率使其成為在停電期間尋求不間斷電力的屋主的首選。自動轉換開關和遠端監控功能的整合進一步增強了它們的吸引力,為屋主提供了更大的便利性和對備用電源系統的控制。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 30億美元 |

| 預測值 | 55億美元 |

| 複合年成長率 | 6.2% |

到 2034 年,三相家用備用發電機組市場的瓦斯部分預計將以 6.5% 的複合年成長率成長。這些發電機因其使用壽命長、易於維護以及顆粒物和氮氧化物 (NOx) 排放量顯著降低而越來越受到青睞。隨著天然氣基礎設施的擴大和環境法規的收緊,屋主選擇使用燃氣發電機組來符合永續發展目標。與柴油動力替代品相比,燃氣發電機組運作更安靜,燃料儲存問題減少,能源供應更穩定,使其成為住宅應用的理想選擇。此外,隨著技術進步提高燃油效率和排放控制,預計未來幾年燃氣備用發電機的採用將會加速。

預計到 2034 年,美國三相家用備用發電機組市場將創收 15 億美元。對電子設備和家庭自動化系統的依賴日益增加,再加上正在進行的住房開發計劃,推動了市場需求。房地產行業的擴張,加上快速的城市化和人口成長,進一步促進了備用發電機的普及。電網基礎設施老化和頻繁停電凸顯了可靠備用電源解決方案的重要性。隨著極端天氣條件變得越來越難以預測,越來越多的美國屋主投資備用發電機組以確保能源安全。此外,可支配收入的增加和對能源彈性的認知的增強推動了住宅環境對高性能三相發電機組的需求。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 市場估計和預測參數

- 預測計算

- 資料來源

- 基本的

- 次要

- 有薪資的

- 民眾

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 戰略展望

- 創新與永續發展格局

第5章:市場規模及預測:依功率等級,2021 – 2034 年

- 主要趨勢

- ≤ 10千伏安

- > 10 千伏安 - 50 千伏安

- > 50 千伏安 - 100 千伏安

- >100千伏安

第6章:市場規模及預測:依燃料,2021 – 2034 年

- 主要趨勢

- 柴油引擎

- 氣體

- 其他

第 7 章:市場規模及預測:依產品,2021 – 2034 年

- 主要趨勢

- 空氣冷卻

- 液體冷卻

第 8 章:市場規模與預測:按地區,2021 – 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第9章:公司簡介

- Ashok Leyland

- Caterpillar

- Champion Power Equipment

- Cummins

- Eaton

- Generac Power Systems

- Gillette Generators

- HIMOINSA

- HIPOWER

- Kirloskar

- Mahindra Powerol

- Powerica

- PR Power

- Rehlko

- Rolls-Royce

The Global Three Phase Home Standby Gensets Market was valued at USD 3 billion in 2024 and is projected to grow at a CAGR of 6.2% between 2025 and 2034. With the increasing frequency and intensity of weather-related disasters, coupled with vulnerabilities in aging power infrastructure, the demand for reliable backup power solutions continues to rise. Homeowners are prioritizing power security as outages become more prevalent due to hurricanes, winter storms, and grid failures. As modern homes incorporate more energy-intensive appliances and smart home technologies, the need for uninterrupted electricity supply further drives the market's expansion. Additionally, government initiatives aimed at strengthening residential infrastructure and the rising trend of home automation contribute to market growth. With technological advancements enhancing generator efficiency, noise reduction, and fuel economy, more homeowners are investing in three-phase standby gensets as a long-term power solution.

The market segment comprising gensets with power ratings between >10 kVA and 50 kVA is anticipated to generate USD 2.5 billion by 2034. These systems are widely adopted to support essential household functions, including HVAC systems, home security networks, and other high-energy appliances. Larger homes, in particular, rely on these gensets for their ability to seamlessly manage substantial internal loads. Despite the higher upfront costs compared to alternative backup solutions, the long-term reliability and efficiency of these units make them a preferred choice for homeowners who seek uninterrupted power during outages. The integration of automatic transfer switches and remote monitoring capabilities further enhances their appeal, offering homeowners greater convenience and control over their backup power systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 6.2% |

The gas-fueled segment of the three-phase home standby gensets market is expected to grow at a CAGR of 6.5% through 2034. These generators are increasingly favored for their long operational life, ease of maintenance, and significantly lower emissions of particulate matter and nitrogen oxides (NOx). As natural gas infrastructure expands and environmental regulations tighten, homeowners are opting for gas-fueled gensets to align with sustainability goals. Compared to diesel-powered alternatives, gas gensets offer quieter operation, reduced fuel storage concerns, and a more consistent energy supply, making them an attractive choice for residential applications. Furthermore, with technological advancements improving fuel efficiency and emissions control, the adoption of gas-powered standby generators is expected to accelerate in the coming years.

The U.S. three-phase home standby gensets market is projected to generate USD 1.5 billion by 2034. Increasing reliance on electronic devices and home automation systems, combined with ongoing housing development initiatives, fuels market demand. The expansion of the real estate sector, coupled with rapid urbanization and population growth, further contributes to the rising adoption of standby generators. Aging power grid infrastructure and frequent blackouts have underscored the importance of reliable backup power solutions. As extreme weather conditions become more unpredictable, more U.S. homeowners are investing in standby gensets to ensure energy security. Additionally, increasing disposable incomes and greater awareness of energy resilience drive the demand for high-performance three-phase gensets across residential settings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 – 2034 ('000 Units & USD Million)

- 5.1 Key trends

- 5.2 ≤ 10 kVA

- 5.3 > 10 kVA - 50 kVA

- 5.4 > 50 kVA - 100 kVA

- 5.5 > 100 kVA

Chapter 6 Market Size and Forecast, By Fuel, 2021 – 2034 ('000 Units & USD Million)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Others

Chapter 7 Market Size and Forecast, By Product, 2021 – 2034 ('000 Units & USD Million)

- 7.1 Key trends

- 7.2 Air cooled

- 7.3 Liquid cooled

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 ('000 Units & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Mexico

- 8.7.3 Argentina

Chapter 9 Company Profiles

- 9.1 Ashok Leyland

- 9.2 Caterpillar

- 9.3 Champion Power Equipment

- 9.4 Cummins

- 9.5 Eaton

- 9.6 Generac Power Systems

- 9.7 Gillette Generators

- 9.8 HIMOINSA

- 9.9 HIPOWER

- 9.10 Kirloskar

- 9.11 Mahindra Powerol

- 9.12 Powerica

- 9.13 PR Power

- 9.14 Rehlko

- 9.15 Rolls-Royce