|

市場調查報告書

商品編碼

1684724

行動寬頻基礎設施市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Mobile Broadband Infrastructure Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

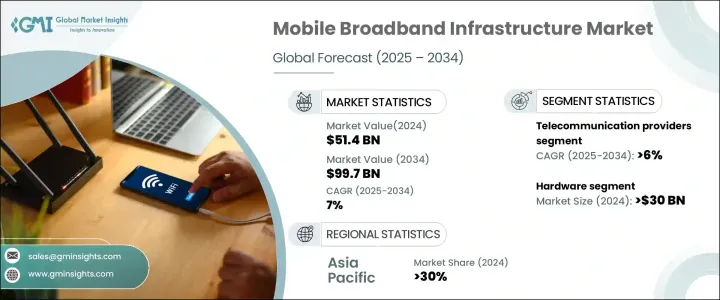

2024 年全球行動寬頻基礎設施市場規模達到 514 億美元,預計 2025 年至 2034 年期間將以 7% 的複合年成長率強勁成長。這一成長主要得益於 5G 網路的快速擴張以及旨在增強 4G LTE 覆蓋範圍的大量投資,尤其是在新興經濟體。隨著行動裝置使用量的不斷成長,以及視訊串流和物聯網應用的普及,對電信服務的需求激增。這些趨勢加劇了對更先進的網路基礎設施的需求,以處理日益成長的資料流量和連接要求。行動寬頻基礎設施市場在確保用戶和企業能夠可靠、高速地存取網際網路方面發揮著至關重要的作用,尤其是在行動網路仍處於發展階段的地區。支援不斷成長的資料消費和設備連接的能力是關鍵,使得基礎設施升級和擴展成為全球電信公司的首要任務。

推動該市場成長的主要因素之一是硬體部分,其市場規模在 2024 年將達到 300 億美元。由於現代行動網路需要越來越先進的系統來滿足 5G 及更高技術的更高功率、更低延遲和可擴展性需求,因此對硬體解決方案的需求仍然強勁。網路基礎設施必須處理大量增加的資料傳輸和設備連接,這需要高度可靠、高效能的硬體。隨著電信供應商推出 5G 等更先進的技術,對強大硬體解決方案的需求預計將持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 514億美元 |

| 預測值 | 997億美元 |

| 複合年成長率 | 7% |

從終端用戶來看,行動寬頻基礎設施市場分為電信供應商、企業和政府部門。尤其是電信供應商,預計將經歷穩定成長,預計 2025 年至 2034 年之間的複合年成長率為 6%。視訊串流、物聯網整合和即時通訊等數據密集型活動推動了對更大網路容量的需求,這促使電信公司大力投資升級其網路。這些投資對於擴大覆蓋範圍和提高頻寬能力至關重要,確保電信服務能夠滿足消費者和企業日益成長的需求。

2024 年,亞太地區佔 30% 的市場佔有率,其中中國占主導地位。中國政府積極投資推動技術基礎建設,特別是5G網路的部署,使中國成為網路擴展的全球領導者。中國科技巨頭正帶頭大規模部署5G基地台,為該地區的基礎設施發展做出重大貢獻。這項快速發展使中國不僅成為自身市場的重要參與者,也成為全球行動寬頻基礎設施解決方案的主要供應商。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 供應商概況

- 組件提供者

- 製造商

- 經銷商

- 最終用戶

- 利潤率分析

- 技術與創新格局

- 專利分析

- 2024年主要國家行動上網用戶普及率

- 2024 年蜂窩網路連接統計數據

- 監管格局

- 衝擊力

- 成長動力

- 智慧型設備和物聯網擴展導致對高速連接的需求不斷成長

- 5G 網路加速普及,增強基礎設施能力

- 增加對網路升級和擴展的電信投資

- 偏遠和服務欠缺地區對行動衛星服務的依賴日益增加

- 雲端運算和邊緣運算的進步推動了強勁的網路需求

- 產業陷阱與挑戰

- 部署先進基礎設施的資本成本高昂

- 監管和合規障礙延遲了技術推廣

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 硬體

- 天線和收發器

- 遠程無線電單元 (RRU)

- 基頻單元 (BBU)

- 濾波器和雙工器

- 功率放大器

- 其他

- 軟體

- 網路管理系統

- 營運支撐系統(OSS)

- 業務支援系統 (BSS)

- 網路功能虛擬化 (NFV)

- 其他

- 服務

- 網路諮詢

- 整合與部署

- 支援與維護

第6章:市場估計與預測:依技術,2021 - 2034 年

- 主要趨勢

- 3G

- 4G

- 5G

第 7 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 電信業者

- 企業

- 政府

第 8 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第9章:公司簡介

- Altiostar Networks

- Arista Networks

- Aviat Networks

- Cambium Networks

- Ciena

- Cisco Systems

- CommScope

- Ericsson

- FiberHome

- Fujitsu

- Huawei Technologies

- Juniper Networks

- Mavenir Systems

- NEC

- Nokia

- Parallel Wireless

- Qualcomm

- Radwin

- Samsung Electronics

- ZTE

The Global Mobile Broadband Infrastructure Market reached USD 51.4 billion in 2024 and is expected to experience robust growth at a CAGR of 7% from 2025 to 2034. This growth is largely driven by the rapid expansion of 5G networks and significant investments aimed at enhancing 4G LTE coverage, particularly in emerging economies. As mobile device usage continues to rise, along with video streaming and the proliferation of IoT applications, the demand for telecom services has surged. These trends are intensifying the need for more advanced network infrastructure to handle the increasing volume of data traffic and connectivity requirements. The mobile broadband infrastructure market plays a vital role in ensuring that users and businesses have reliable, high-speed access to the Internet, especially in regions where mobile networks are still in the development phase. The ability to support growing data consumption and device connectivity is key, making infrastructure upgrades and expansion a top priority for telecom companies worldwide.

One of the primary components driving the growth of this market is the hardware segment, which accounted for USD 30 billion in 2024. The demand for hardware solutions remains strong as modern mobile networks require increasingly advanced systems to meet the higher power, lower latency, and scalability demands of 5G and beyond. Network infrastructure must handle substantial increases in data transfer and device connectivity, which requires highly reliable, high-performance hardware. This growing need for robust hardware solutions is expected to escalate as telecom providers roll out more advanced technologies like 5G.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $51.4 Billion |

| Forecast Value | $99.7 Billion |

| CAGR | 7% |

When it comes to end users, the mobile broadband infrastructure market is divided into telecommunications providers, enterprises, and government sectors. Telecom providers, in particular, are expected to experience steady growth, with a projected CAGR of 6% between 2025 and 2034. The demand for greater network capacity, driven by data-heavy activities such as video streaming, IoT integration, and real-time communications, is pushing telecom companies to heavily invest in upgrading their networks. These investments are essential to expanding coverage areas and improving bandwidth capabilities, ensuring that telecom services can meet the rising demands of consumers and businesses alike.

The Asia Pacific region held a dominant 30% market share in 2024, with China playing a leading role. The Chinese government's aggressive investment in advancing its technological infrastructure, particularly in the deployment of 5G networks, has positioned the country as a global leader in network expansion. Chinese technology giants are spearheading the large-scale rollout of 5G base stations, contributing significantly to the region's infrastructure development. This rapid progress has positioned China not only as a key player in its own market but also as a major supplier of mobile broadband infrastructure solutions worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Manufacturers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Mobile internet user penetration rate in major countries, 2024

- 3.7 Cellular network connection statistics, 2024

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for high-speed connectivity due to smart devices and IoT expansion

- 3.9.1.2 Accelerated adoption of 5G networks boosting infrastructure capabilities

- 3.9.1.3 Increased telecom investments in network upgrades and expansion

- 3.9.1.4 Growing reliance on mobile satellite services for remote and underserved regions

- 3.9.1.5 Advances in cloud and edge computing driving robust network requirements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High capital costs for deploying advanced infrastructure

- 3.9.2.2 Regulatory and compliance hurdles delaying technology rollouts

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Antennas & transceivers

- 5.2.2 Remote Radio Units (RRU)

- 5.2.3 Baseband Units (BBU)

- 5.2.4 Filters & duplexers

- 5.2.5 Power amplifiers

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Network management systems

- 5.3.2 Operation Support Systems (OSS)

- 5.3.3 Business Support Systems (BSS)

- 5.3.4 Network Function Virtualization (NFV)

- 5.3.5 Others

- 5.4 Services

- 5.4.1 Network consulting

- 5.4.2 Integration & deployment

- 5.4.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 3G

- 6.3 4G

- 6.4 5G

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Telecommunications providers

- 7.3 Enterprises

- 7.4 Government

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Altiostar Networks

- 9.2 Arista Networks

- 9.3 Aviat Networks

- 9.4 Cambium Networks

- 9.5 Ciena

- 9.6 Cisco Systems

- 9.7 CommScope

- 9.8 Ericsson

- 9.9 FiberHome

- 9.10 Fujitsu

- 9.11 Huawei Technologies

- 9.12 Juniper Networks

- 9.13 Mavenir Systems

- 9.14 NEC

- 9.15 Nokia

- 9.16 Parallel Wireless

- 9.17 Qualcomm

- 9.18 Radwin

- 9.19 Samsung Electronics

- 9.20 ZTE