|

市場調查報告書

商品編碼

1684695

資料中心儲能市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Data Center Energy Storage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

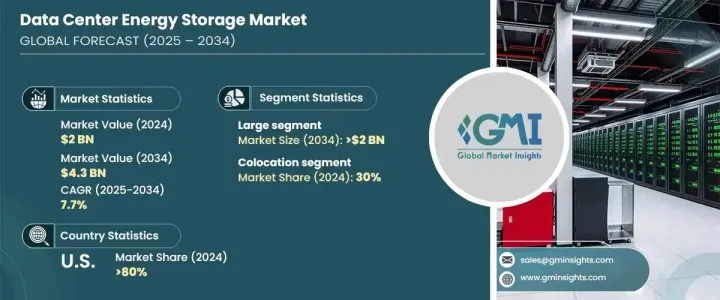

2024 年全球資料中心儲能市場價值為 20 億美元,呈現強勁成長趨勢,預計 2025 年至 2034 年期間的複合年成長率為 7.7%。企業正在擺脫傳統電網,轉而專注於符合永續發展目標並增強營運彈性的先進儲存技術。隨著人們對碳足跡的擔憂日益加劇以及能源成本的上升,對再生能源整合的推動力比以往任何時候都更加強勁。該公司正在利用尖端儲存系統來維持正常運行時間、減少電力支出並支持向更環保的數位基礎設施的轉變。

雲端運算、人工智慧和巨量資料分析的快速擴張加劇了對可擴展能源儲存解決方案的需求。數位交易和資料處理不斷升級,對能夠維持高效能運算的節能系統的依賴性越來越強。世界各地的組織都在投資創新的能源儲存技術,以提高電力可靠性並最大限度地降低停機風險。由於監管框架強調永續性,資料中心正在優先考慮環保能源解決方案,以在不斷發展的市場中保持競爭力。該產業向混合能源儲存的轉變,包括鋰離子電池、飛輪和其他節能系統,進一步強調了向有彈性、永續的基礎設施的轉變。隨著電源管理系統的不斷進步,資料中心在保持高速運算效能的同時,也正在最佳化能源效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 20億美元 |

| 預測值 | 43億美元 |

| 複合年成長率 | 7.7% |

根據資料中心規模,市場細分為小型、中型和大型設施。 2024 年,大型資料中心佔據了 46 %的市場佔有率,預計到 2034 年收入將達到 20 億美元。隨著能源需求的不斷成長,企業正在整合先進的儲存技術來增強系統彈性、減少電源故障並最佳化能源效率。這些大型中心需要強大的儲存基礎設施來支援不斷增加的資料負載,從而推動對能源儲存系統的大量投資。

該市場進一步按應用分類,涵蓋銀行、能源、政府、醫療保健、製造業、IT 和主機託管服務。 2024 年,主機託管中心佔據了 30% 的市場佔有率,反映出人們對共享資料儲存設施的偏好日益成長。利用主機託管服務的企業優先考慮持續的電力供應,使能源儲存解決方案成為其營運策略的重要組成部分。對第三方資料儲存的日益依賴加劇了對節能基礎架構的需求,迫使主機託管供應商實施尖端的電源管理解決方案。先進的儲能技術在保持可靠性的同時確保了經濟高效的營運,進一步推動了整個產業的應用。

2024年美國資料中心儲能市場將佔據全球80%的佔有率,鞏固其作為主要產業驅動力的地位。隨著企業尋求更靈活、更具成本效益的能源消耗策略,該地區在大型基礎設施專案中的領導地位加速了先進儲存解決方案的採用。北美各地的公司正積極加強能源效率舉措,以實現永續發展目標、減少碳排放並提高電力可靠性。對環保基礎設施的高度重視和對能源儲存技術的持續投資使該地區處於市場成長的前沿。隨著實現碳中和的努力不斷加大,北美資料中心正在為能源效率制定新的標準,增強市場擴張和長期生存能力。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 原物料供應商

- 零件供應商

- 製造商

- 技術提供者

- 經銷商

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 專利分析

- 監管格局

- 定價分析

- 衝擊力

- 成長動力

- 整合再生能源以提高效率

- 資料中心對備用電源解決方案的需求

- 採用綠色能源儲存解決方案

- 儲能系統的技術進步

- 產業陷阱與挑戰

- 能源儲存技術的前期成本高

- 大規模部署的技術限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按資料中心規模,2021 - 2034 年

- 主要趨勢

- 小的

- 中等的

- 大的

第6章:市場估計與預測:依層級,2021 - 2034 年

- 主要趨勢

- 第 1 層

- 第 2 層

- 第 3 級

- 第 4 層

第 7 章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 鋰離子電池

- 鉛酸電池

- 鎳鎘電池

- 飛輪儲能

- 超級電容器

- 液流電池

第 8 章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 金融保險業協會

- 主機託管

- 能源

- 政府

- 衛生保健

- 製造業

- 資訊科技和電信

- 其他

第 9 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第10章:公司簡介

- ABB

- BYD

- Cummins

- Delta

- Eaton

- Generac Power Systems

- Hitachi Energy

- Huawei

- Johnson Controls International

- Legrand

- LG Energy Solution

- Mitsubishi

- Riello Elettronica

- Samsung SDI

- Schneider Electric

- Siemens

- Socomec

- Tesla

- Toshiba

- Vertiv

The Global Data Center Energy Storage Market, valued at USD 2 billion in 2024, is on a strong growth trajectory, with a projected CAGR of 7.7% between 2025 and 2034. As the demand for digital services surges, data centers are under increasing pressure to adopt efficient energy storage solutions that ensure uninterrupted power supply and optimize energy consumption. Businesses are moving away from traditional power grids, focusing instead on advanced storage technologies that align with sustainability goals and enhance operational resilience. With growing concerns over carbon footprints and rising energy costs, the push for renewable energy integration is stronger than ever. Companies are leveraging cutting-edge storage systems to maintain uptime, reduce electricity expenses, and support the shift toward a greener digital infrastructure.

The rapid expansion of cloud computing, artificial intelligence, and big data analytics has intensified the need for scalable energy storage solutions. Digital transactions and data processing continue to escalate, increasing dependency on energy-efficient systems that can sustain high-performance computing. Organizations worldwide are investing in innovative energy storage technologies to improve power reliability and minimize the risk of downtime. As regulatory frameworks emphasize sustainability, data centers are prioritizing eco-friendly energy solutions to remain competitive in the evolving market. The industry's transition toward hybrid energy storage, incorporating lithium-ion batteries, flywheels, and other energy-efficient systems, further underscores the shift toward a resilient, sustainable infrastructure. With the continued advancement of power management systems, data centers are optimizing energy efficiency while maintaining high-speed computing performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 7.7% |

Market segmentation by data center size includes small, medium, and large facilities. In 2024, large data centers accounted for 46% of the market share, with revenue projections reaching USD 2 billion by 2034. High-capacity data centers depend on sophisticated energy storage solutions to ensure seamless operations, preventing disruptions in critical computing environments. As energy demands rise, businesses are integrating advanced storage technologies to enhance system resilience, reduce power failures, and optimize energy efficiency. These large-scale centers require robust storage infrastructure to support increasing data loads, driving significant investments in energy storage systems.

The market is further categorized by application, covering banking, energy, government, healthcare, manufacturing, IT, and colocation services. In 2024, colocation centers held a 30% market share, reflecting the growing preference for shared data storage facilities. Businesses utilizing colocation services prioritize continuous power availability, making energy storage solutions an essential component of their operational strategy. The increasing reliance on third-party data storage has intensified the demand for energy-efficient infrastructure, compelling colocation providers to implement cutting-edge power management solutions. Advanced energy storage technology ensures cost-effective operations while maintaining reliability, further driving adoption across the sector.

The US data center energy storage market accounted for 80% of the global share in 2024, solidifying its position as a major industry driver. The region's leadership in large-scale infrastructure projects has accelerated the adoption of advanced storage solutions as businesses seek more flexible and cost-effective energy consumption strategies. Companies across North America are actively enhancing energy efficiency initiatives to meet sustainability targets, reducing carbon emissions, and improving power reliability. The strong focus on eco-friendly infrastructure and continuous investment in energy storage technologies have positioned the region at the forefront of market growth. With increasing efforts to achieve carbon neutrality, North American data centers are setting new standards for energy efficiency, reinforcing market expansion and long-term viability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Distributors

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Integration of renewable energy sources for efficiency

- 3.8.1.2 Demand for backup power solutions in data centers

- 3.8.1.3 Adoption of green energy storage solutions

- 3.8.1.4 Technological advancements in energy storage systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High upfront costs of energy storage technologies

- 3.8.2.2 Technological limitations in large-scale deployments

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Data Center Size, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Small

- 5.3 Medium

- 5.4 Large

Chapter 6 Market Estimates & Forecast, By Tier, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Tier 1

- 6.3 Tier 2

- 6.4 Tier 3

- 6.5 Tier 4

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Lithium-ion batteries

- 7.3 Lead-acid batteries

- 7.4 Nickel-cadmium batteries

- 7.5 Flywheel energy storage

- 7.6 Supercapacitors

- 7.7 Flow batteries

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Colocation

- 8.4 Energy

- 8.5 Government

- 8.6 Healthcare

- 8.7 Manufacturing

- 8.8 IT & telecom

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 BYD

- 10.3 Cummins

- 10.4 Delta

- 10.5 Eaton

- 10.6 Generac Power Systems

- 10.7 Hitachi Energy

- 10.8 Huawei

- 10.9 Johnson Controls International

- 10.10 Legrand

- 10.11 LG Energy Solution

- 10.12 Mitsubishi

- 10.13 Riello Elettronica

- 10.14 Samsung SDI

- 10.15 Schneider Electric

- 10.16 Siemens

- 10.17 Socomec

- 10.18 Tesla

- 10.19 Toshiba

- 10.20 Vertiv