|

市場調查報告書

商品編碼

1667119

異麥芽低聚醣市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Isomalto-oligosaccharide Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

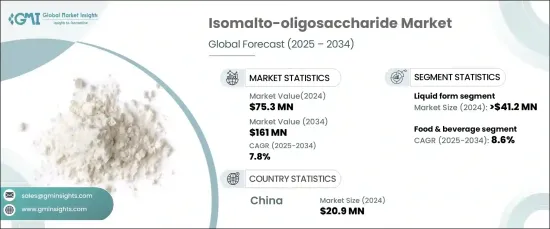

2024 年全球異麥芽寡糖市場價值為 7,530 萬美元,預計 2025 年至 2034 年的複合年成長率為 7.8%。 IMO 以低熱量甜味劑和益生元纖維而聞名,在這種背景下越來越受歡迎。與生活方式相關的健康問題(包括消化問題和肥胖症)日益普遍,推動了對 IMO 等功能性成分的需求。此外,烘焙食品、乳製品和膳食補充劑等類別向更健康、功能性的食品轉變正在加速市場成長。然而,製造商必須滿足複雜的監管要求,包括不同地區不同的標準。遵守這些規定至關重要,特別是在產品標籤和健康聲明方面。不符合這些規定可能會阻礙IMO在食品業的廣泛使用,並減緩市場採用。

從形式來看,IMO 市場的液體部分在 2024 年的收入超過 4,120 萬美元,預計複合年成長率為 8.6%。異麥芽寡糖的液態形式具有多功能性和便利性,使其成為食品和飲料製造商的首選。液態 IMO 可以輕鬆加入糖漿、飲料和液體營養補充品等各種產品中,因此廣受歡迎。此外,液態 IMO 可以使產品配方更加一致,對成分劑量的控制也更加精確,這對於保持最終產品的風味和質地至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7,530 萬美元 |

| 預測值 | 1.61億美元 |

| 複合年成長率 | 7.8% |

食品和飲料行業是異麥芽低聚醣的最大應用領域,2024 年該領域的收入將超過 4560 萬美元。 IMO 還具有益生元功效,有助於腸道健康,因此成為注重健康的消費者的熱門選擇。由於其用途廣泛,因此可以用於各種食品,包括糖果、乳製品、烘焙食品以及飲料。

由於玉米的廣泛供應和加工基礎設施的完善,預計預測期內玉米基異麥芽寡糖將顯著成長。玉米衍生的 IMO 為製造商提供了一種經濟可行的選擇,並且由於其中性的味道而受到青睞,這使得它們可以輕鬆地融入各種食品和飲料應用中。

以中國和日本等國為首的亞太地區是IMO市場的主要地區,無論從生產量或消費量來看。由於對清潔標籤產品和保健品的需求不斷成長,北美和歐洲也經歷了強勁成長。特別是亞太地區長期以來在食品中使用天然成分的傳統,這項傳統在IMO被從傳統糖果到現代飲料等各種食品應用廣泛接受的過程中發揮了關鍵作用。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 增強健康意識

- 不斷擴大的功能性食品市場

- 食品配方創新

- 產業陷阱與挑戰

- 監管挑戰和標籤問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場規模與預測:依形式,2021-2034 年

- 主要趨勢

- 液體

- 粉末

- 其他

第 6 章:市場規模與預測:按來源,2021-2034 年

- 主要趨勢

- 玉米

- 小麥

- 馬鈴薯

- 木薯

- 其他

第 7 章:市場規模與預測:依技術,2021-2034 年

- 主要趨勢

- 食品和飲料

- 功能性食品

- 乳製品

- 嬰兒配方奶粉

- 其他

- 膳食補充劑

- 體重減輕

- 運動營養

- 整體幸福感

- 其他

- 動物飼料添加劑

- 家禽

- 豬

- 牛

- 水產養殖

- 寵物食品

- 馬

- 其他

- 其他

第 8 章:市場規模與預測:按地區,2021-2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Nikon Shikuhin KaKo Co., Ltd.

- BioNeutra North America

- Baolingbao Biology Co., Ltd.

- Luzhou Bio-chem Technology Co., Ltd.

- Shandong Bailong Chuangyuan Bio-Tech Co., Ltd.

- Shandong Tianmei Bio-Tech Co., Ltd.

- Shandong Tianjiao Bio-engineering Co., Ltd.

The Global Isomalto-Oligosaccharide Market, valued at USD 75.3 million in 2024, is anticipated to expand at a CAGR of 7.8% from 2025 to 2034. As consumers grow more health-conscious, they increasingly seek products that offer nutritional benefits. IMOs, known for being low-calorie sweeteners and prebiotic fibers, have gained popularity in this context. The rising prevalence of lifestyle-related health issues, including digestive problems and obesity, has fueled the demand for functional ingredients such as IMO. In addition, the shift towards healthier, functional foods in categories such as bakery, dairy, and dietary supplements is accelerating market growth. However, manufacturers must navigate complex regulatory requirements, including varying standards across different regions. Compliance with these regulations is essential, particularly when it comes to product labeling and health claims. Failure to meet these regulations could hinder the widespread use of IMO in the food industry and slow down market adoption.

In terms of form, the liquid segment of the IMO market accounted for over USD 41.2 million in revenue in 2024 and is projected to grow at a CAGR of 8.6%. The liquid form of isomalto-oligosaccharides offers versatility and convenience, which makes it a preferred choice for food and beverage manufacturers. The ease with which liquid IMOs can be incorporated into a range of products, such as syrups, beverages, and liquid nutritional supplements, drives its popularity. Additionally, liquid IMOs allow for better consistency in product formulations and more precise control over ingredient dosages, which is crucial for maintaining flavor and texture in end products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $75.3 Million |

| Forecast Value | $161 Million |

| CAGR | 7.8% |

The food and beverage sector is the largest application for isomalto-oligosaccharides, generating over USD 45.6 million in revenue in 2024. This segment is expected to grow at a CAGR of 8.6% by 2034. As consumers demand healthier options, food manufacturers are increasingly turning to IMO as a low-calorie sweetener that can reduce sugar content without sacrificing taste. IMOs also offer prebiotic benefits, which contribute to gut health, making them a popular choice for health-conscious consumers. Their versatility allows them to be used in a wide variety of food products, including confectionery, dairy, and bakery items, as well as beverages.

Corn-based isomalto-oligosaccharides are expected to experience significant growth during the forecast period due to the widespread availability of corn and the established infrastructure for processing it. Corn-derived IMOs provide an economically viable option for manufacturers and are preferred for their neutral taste, which allows them to be easily integrated into various food and beverage applications.

Asia-Pacific, led by countries such as China and Japan, is the dominant region in the IMO market, both in terms of production and consumption. North America and Europe are also witnessing strong growth, driven by an increasing demand for clean-label products and health supplements. In particular, the Asia-Pacific region's long-standing tradition of using natural ingredients in food has played a key role in the widespread acceptance of IMOs across various food applications, from traditional sweets to modern beverages.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing Health Consciousness

- 3.6.1.2 Expanding Functional Food Market

- 3.6.1.3 Innovation in Food Formulations

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Regulatory Challenges and Labeling Issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Form, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Liquid

- 5.3 Powder

- 5.4 Others

Chapter 6 Market Size and Forecast, By Source, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Corn

- 6.3 Wheat

- 6.4 Potato

- 6.5 Tapioca

- 6.6 Others

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.2.1 Functional food

- 7.2.2 Dairy products

- 7.2.3 Infant formula

- 7.2.4 Others

- 7.3 Dietary supplements

- 7.3.1 Weight loss

- 7.3.2 Sports nutrition

- 7.3.3 General Well-Being

- 7.3.4 Others

- 7.4 Animal feed additives

- 7.4.1 Poultry

- 7.4.2 Swine

- 7.4.3 Cattle

- 7.4.4 Aquaculture

- 7.4.5 Pet Food

- 7.4.6 Equine

- 7.4.7 Others

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Nikon Shikuhin KaKo Co., Ltd.

- 9.2 BioNeutra North America

- 9.3 Baolingbao Biology Co., Ltd.

- 9.4 Luzhou Bio-chem Technology Co., Ltd.

- 9.5 Shandong Bailong Chuangyuan Bio-Tech Co., Ltd.

- 9.6 Shandong Tianmei Bio-Tech Co., Ltd.

- 9.7 Shandong Tianjiao Bio-engineering Co., Ltd.