|

市場調查報告書

商品編碼

1667064

軍用雷達市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Military Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

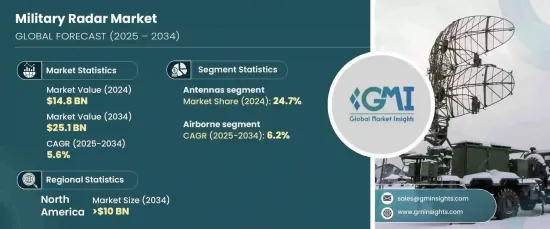

全球軍用雷達市場預計將強勁成長,到 2024 年將達到 148 億美元,預計 2025 年至 2034 年期間的複合年成長率為 5.6%。 隨著各國為應對日益嚴重的安全問題和地緣政治緊張局勢,全球國防預算不斷增加,推動了這一成長。各國政府優先投資先進的雷達系統,以實現國防能力的現代化、增強國家安全、應對新出現的威脅。相控陣和主動電子掃描陣列 (AESA) 系統等下一代雷達技術的日益普及,凸顯了對提高偵測精度、追蹤精度和態勢感知能力的重視。遠程探測和快速威脅識別等增強的功能使雷達技術成為現代軍事戰略的基石。此外,國防承包商和政府之間的合作正在激發創新,推動適應不斷變化的作戰和監視需求的尖端雷達系統的發展。

市場按組件細分,包括天線、發射器、接收器、功率放大器、穩定系統、雙工器、數位訊號處理器、圖形用戶介面等。天線佔據這一領域的主導地位,到 2024 年將佔有 24.7% 的市場佔有率。該能力決定了雷達在偵測、追蹤和瞄準方面的性能,使得天線對於實現卓越的範圍、精度和解析度至關重要。天線技術的創新,例如輕質材料和改進的波束成形技術,進一步提高了其效率和可靠性,鞏固了其在整個雷達生態系統中的重要性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 148億美元 |

| 預測值 | 251億美元 |

| 複合年成長率 | 5.6% |

依平台不同,市場還可分為陸基、海軍、機載和太空系統。其中,機載部分正在成為成長最快的類別,預計預測期內的複合年成長率為 6.2%。戰鬥機、偵察機、無人機等裝備的機載雷達對提升偵察和作戰能力具有重要意義。這些系統在遠程探測和追蹤方面表現出色,使軍隊能夠對抗包括隱形飛機和飛彈系統在內的先進威脅。相控陣與AESA技術的融合,具有更快的掃描速度、更寬的頻率覆蓋範圍和更高的解析度,進一步提升了其能力,顯著提高了複雜戰鬥場景中的作戰效率和態勢感知能力。

北美將主導全球軍用雷達市場,預計到 2034 年將創造 100 億美元的市場價值。該地區優先投資用於監視、預警和作戰管理的現代雷達系統。人工智慧整合等新興技術正在增強雷達能力,使其更適應複雜的軍事行動,並更有效。加拿大也發揮著至關重要的作用,透過先進的雷達開發和旨在加強國防基礎設施的國際合作做出貢獻,進一步推動區域市場的成長。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 增加國防預算和現代化建設力度

- 雷達技術和能力的進步

- 對先進監控系統的需求不斷成長

- 增強威脅偵測和對策需求

- 與人工智慧和自主平台的整合

- 產業陷阱與挑戰

- 先進雷達系統成本高昂

- 監管和出口管制限制

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按組件,2021 年至 2034 年

- 主要趨勢

- 天線

- 拋物面反射天線

- 開槽波導天線

- 相控陣天線

- 多輸入多輸出天線

- 主動掃描陣列天線

- 被動掃描陣列天線

- 發射器

- 微波管發射機

- 固態電子發射器

- 接收器

- 類比接收器

- 數位接收器

- 功率放大器

- 行波管擴大機

- 固態功率放大器

- 砷化鎵

- 氮化鎵

- 碳化矽

- 固態功率放大器

- 行波管擴大機

- 雙工器

- 分支型雙工器

- 平衡型雙工器

- 循環雙工器

- 數位訊號處理器

- 穩定系統

- 圖形使用者介面

- 其他

第6章:市場估計與預測:按波形,2021-2034 年

- 主要趨勢

- 調頻連續波

- 多普勒

- 常規多普勒

- 脈衝多普勒

第 7 章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 軟體定義雷達

- 常規雷達

- 量子雷達

第 8 章:市場估計與預測:按範圍,2021 年至 2034 年

- 主要趨勢

- 短距離(<50 公里)

- 中(50-200 公里)

- 長途(>200 公里)

第 9 章:市場估計與預測:按平台,2021-2034 年

- 主要趨勢

- 地面

- 固定雷達

- 車載雷達

- 攜帶式雷達

- 海軍

- 艦載雷達

- 沿海雷達

- 無人水面艦艇上安裝的雷達

- 空降

- 載人飛機雷達

- 無人機雷達

- 基於浮空器的雷達

- 空間

- 衛星

- 太空船

第 10 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 空域監控與交通管理

- 防空與飛彈防禦

- 武器導引

- 地面監視和入侵者偵測

- 船舶交通安全與監控

- 航空測繪

- 導航

- 地雷探測與地下測繪

- 地面部隊防護與反制測繪

- 天氣監測

- 地面穿透

- 海上巡邏、搜救

- 邊境安全

- 空間態勢感知

- 其他

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 12 章:公司簡介

- Aselsan AS

- BAE Systems plc

- Boeing Company

- Cobham plc

- FLIR Systems, Inc.

- General Dynamics Corporation

- Hensoldt AG

- Honeywell International

- Israel Aerospace Industries

- L3Harris Technologies, Inc.

- Leonardo SPA

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- Rheinmetall AG

- Saab AB

- Thales Group

The Global Military Radar Market is poised for robust growth, reaching USD 14.8 billion in 2024 and projected to expand at a CAGR of 5.6% between 2025 and 2034. This surge is driven by escalating defense budgets worldwide as nations respond to mounting security concerns and geopolitical tensions. Governments are prioritizing investments in advanced radar systems to modernize their defense capabilities, enhance national security, and counter emerging threats. The growing adoption of next-generation radar technologies, including phased array and active electronically scanned array (AESA) systems, underscores the emphasis on improving detection accuracy, tracking precision, and situational awareness. Enhanced functionality, such as long-range detection and rapid threat identification, positions radar technology as a cornerstone of modern military strategies. In addition, collaborations between defense contractors and governments are spurring innovation, propelling the development of cutting-edge radar systems tailored to evolving combat and surveillance needs.

The market is segmented by components, including antennas, transmitters, receivers, power amplifiers, stabilization systems, duplexers, digital signal processors, graphical user interfaces, and others. Antennas dominate this segment, holding a 24.7% market share in 2024. Their critical role in radar functionality stems from their ability to convert electrical signals into electromagnetic waves and vice versa. This capability determines radar performance in detection, tracking, and targeting, making antennas essential for achieving superior range, accuracy, and resolution. Innovations in antenna technology, such as lightweight materials and improved beamforming techniques, are further enhancing their efficiency and reliability, cementing their importance in the overall radar ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.8 Billion |

| Forecast Value | $25.1 Billion |

| CAGR | 5.6% |

The market is also categorized by platform into ground-based, naval, airborne, and space systems. Among these, the airborne segment is emerging as the fastest-growing category, projected to grow at a CAGR of 6.2% during the forecast period. Airborne radars deployed on fighter jets, surveillance aircraft, and UAVs play a pivotal role in enhancing reconnaissance and combat capabilities. These systems excel in long-range detection and tracking, enabling militaries to counter advanced threats, including stealth aircraft and missile systems. The integration of phased array and AESA technologies further elevates their capabilities by offering faster scanning speeds, wider frequency coverage, and higher resolution, which significantly improve operational efficiency and situational awareness in complex battle scenarios.

North America is set to dominate the global military radar market, expected to generate USD 10 billion by 2034. This leadership, spearheaded by the United States, reflects substantial defense budgets and a strategic focus on technological advancements. The region prioritizes investments in modern radar systems for surveillance, early warning, and combat management. Emerging technologies like AI integration are enhancing radar capabilities, making them more adaptive and effective for sophisticated military operations. Canada also plays a vital role, contributing through advanced radar development and international collaborations aimed at fortifying defense infrastructure, further driving regional market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing defense budgets and modernization efforts

- 3.6.1.2 Advancements in radar technology and capabilities

- 3.6.1.3 Rising demand for advanced surveillance systems

- 3.6.1.4 Enhanced threat detection and countermeasure needs

- 3.6.1.5 Integration with AI and autonomous platforms

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced radar systems

- 3.6.2.2 Regulatory and export control restrictions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Antennas

- 5.2.1 Parabolic reflector antennas

- 5.2.2 Slotted waveguide antennas

- 5.2.3 Phased array antennas

- 5.2.4 Multiple Input-Multiple output antennas

- 5.2.5 Active scanned array antennas

- 5.2.6 Passive scanned array antennas

- 5.3 Transmitters

- 5.3.1 Microwave Tube-Based Transmitters

- 5.3.2 Solid-State electronic transmitters

- 5.4 Receivers

- 5.4.1 Analog receivers

- 5.4.2 Digital receivers

- 5.5 Power amplifiers

- 5.5.1 Traveling wave tube amplifiers

- 5.5.1.1 Solid-State power amplifiers

- 5.5.1.1.1 Gallium arsenide

- 5.5.1.1.2 Gallium nitride

- 5.5.1.1.3 Silicon carbide

- 5.5.1.1 Solid-State power amplifiers

- 5.5.1 Traveling wave tube amplifiers

- 5.6 Duplexers

- 5.6.1 Branch-Type duplexers

- 5.6.2 Balanced-Type duplexers

- 5.6.3 Circulator duplexers

- 5.7 Digital signal processors

- 5.8 Stabilization systems

- 5.9 Graphical user interfaces

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Waveform, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Frequency-Modulated continuous wave

- 6.3 Doppler

- 6.3.1 Conventional doppler

- 6.3.2 Pulse-Doppler

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Software-Defined radars

- 7.3 Conventional radars

- 7.4 Quantum radars

Chapter 8 Market Estimates & Forecast, By Range, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Short (<50 Kms)

- 8.3 Medium (50-200 Kms)

- 8.4 Long (>200 Kms)

Chapter 9 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Ground-Based

- 9.2.1 Fixed radars

- 9.2.2 Vehicle-Based radars

- 9.2.3 Man-Portable radars

- 9.3 Naval

- 9.3.1 Vessel-Based radars

- 9.3.2 Coastal radars

- 9.3.3 USV-Mounted radars

- 9.4 Airborne

- 9.4.1 Manned aircraft radars

- 9.4.2 UAV-Mounted radars

- 9.4.3 Aerostats-Based radar

- 9.5 Space

- 9.5.1 Satellites

- 9.5.2 Spacecraft

Chapter 10 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 Airspace Monitoring & Traffic management

- 10.3 Air & Missile defense

- 10.4 Weapon guidance

- 10.5 Ground Surveillance & Intruder Detection

- 10.6 Vessel Traffic Security & Surveillance

- 10.7 Airborne mapping

- 10.8 Navigation

- 10.9 Mine Detection & Underground mapping

- 10.10 Ground Force Protection & Counter-Mapping

- 10.11 Weather monitoring

- 10.12 Ground penetration

- 10.13 Maritime Patrolling, Search, & Rescue

- 10.14 Border security

- 10.15 Space situational awareness

- 10.16 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Aselsan A.S.

- 12.2 BAE Systems plc

- 12.3 Boeing Company

- 12.4 Cobham plc

- 12.5 FLIR Systems, Inc.

- 12.6 General Dynamics Corporation

- 12.7 Hensoldt AG

- 12.8 Honeywell International

- 12.9 Israel Aerospace Industries

- 12.10 L3Harris Technologies, Inc.

- 12.11 Leonardo S.P.A.

- 12.12 Lockheed Martin Corporation

- 12.13 Northrop Grumman Corporation

- 12.14 Raytheon Technologies Corporation

- 12.15 Rheinmetall AG

- 12.16 Saab AB

- 12.17 Thales Group

軍用雷達市場:按類型、頻段、技術和應用分類-2026-2032年全球市場預測

軍用雷達市場:按類型、頻段、技術和應用分類-2026-2032年全球市場預測 2026年全球軍用攜帶式監視雷達市場報告2026年全球軍用雷達市場報告

2026年全球軍用攜帶式監視雷達市場報告2026年全球軍用雷達市場報告 軍用雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測氮化鎵軍用雷達市場:按頻寬、平台、架構、部署模式和應用分類-2026-2032年全球預測水面雷達市場:按組件、技術、頻段、距離、尺寸和應用分類,全球預測,2026-2032年地面雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測

軍用雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測氮化鎵軍用雷達市場:按頻寬、平台、架構、部署模式和應用分類-2026-2032年全球預測水面雷達市場:按組件、技術、頻段、距離、尺寸和應用分類,全球預測,2026-2032年地面雷達市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並提供2026-2034年的洞察和預測 軍用攜帶式雷達系統市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、範圍、頻段、地區和競爭對手分類,2021-2031年

軍用攜帶式雷達系統市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、範圍、頻段、地區和競爭對手分類,2021-2031年 下一代軍用雷達系統市場:按組件、平台、頻率、距離、應用、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測

下一代軍用雷達系統市場:按組件、平台、頻率、距離、應用、國家和地區分類-全球產業分析、市場規模、市場佔有率及2025-2032年預測 軍用雷達的全球市場:各用途,各平台,各技術,各地區,機會,預測,2018年~2032年

軍用雷達的全球市場:各用途,各平台,各技術,各地區,機會,預測,2018年~2032年