|

市場調查報告書

商品編碼

1667022

人工耳蝸市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cochlear Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

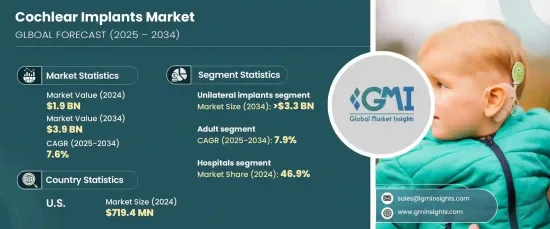

2024 年全球人工耳蝸市場價值為 19 億美元,預計將實現顯著成長,預計 2025 年至 2034 年的複合年成長率為 7.6%。人工耳蝸為患有重度至極重度聽力損失的人提供了變革性的解決方案,越來越被認為是一種改變生活的干涉措施。

由政府、醫療保健組織和非政府組織主導的教育活動正在極大地提高公眾對人工耳蝸的益處和功能的理解。此外,各地區提供補貼和加強保險覆蓋的努力使得這些設備更容易獲得,從而進一步推動市場成長。無線連接和人工智慧驅動的聲音處理等尖端技術的日益融合也有望增強人工耳蝸的功能,確保其持續的吸引力和採用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 19億美元 |

| 預測值 | 39億美元 |

| 複合年成長率 | 7.6% |

市場依植入物類型細分,主要分為兩類:單側植入物和雙側植入物。預計單側植入物將經歷強勁成長,預計複合年成長率為 7.4%,到 2034 年將達到 33 億美元。單側植入物對於單耳聽力損失的人特別有效,可以顯著改善聲音處理和溝通能力。單側植入物的成本效益和目標效益使其成為市場擴張的主要驅動力。

人工耳蝸的最終用途應用包括耳鼻喉診所、醫院和門診手術中心,其中醫院佔據最大的市場佔有率,到 2024 年將達到 46.9%。這些設施確保了精確的植入程序和有效的術後護理,有助於其在市場上佔據主導地位。

美國人工耳蝸市場價值在 2024 年將達到 7.194 億美元,預計在 2025 年至 2034 年期間的複合年成長率為 6.8%。領先的人工耳蝸製造商的存在和全面的保險覆蓋進一步加強了市場的地位,使得人工耳蝸成為美國聽力障礙人士越來越可行的解決方案。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 聽力損失盛行率不斷上升

- 技術進步

- 提高認知和早期診斷

- 政府支持及報銷情況改善

- 產業陷阱與挑戰

- 人工耳蝸費用高

- 缺乏有關聽力損失的知識

- 成長動力

- 成長潛力分析

- 2024 年定價分析

- 報銷場景

- 監管格局

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東及非洲

- 消費者路徑

- 技術格局

- 政策格局

- 風險管理分析

- 研究與開發

- 營運

- 行銷和銷售

- 品質

- 智慧財產

- 監管

- 資訊科技

- 氣候

- 金融的

- 波特的分析

- 差距分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 公司市佔率分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 單側植入

- 雙側植入

第 6 章:市場估計與預測:按病患類型,2021 - 2034 年

- 主要趨勢

- 成人

- 兒科

第 7 章:市場估計與預測:按最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 耳鼻喉診所

- 門診手術中心

第 8 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Cochlear

- Envoy Medical

- MED-EL

- Nurotron

- Sonova

The Global Cochlear Implants Market, valued at USD 1.9 billion in 2024, is poised for remarkable growth, with projections indicating a CAGR of 7.6% from 2025 to 2034. This expansion is fueled by several factors, including the rising prevalence of hearing loss worldwide, advancements in audiology technology, and a growing focus on early diagnosis and treatment. Cochlear implants, which offer a transformative solution for individuals with severe to profound hearing loss, are becoming increasingly recognized as a life-changing intervention.

Educational campaigns led by governments, healthcare organizations, and NGOs are significantly improving public understanding of the benefits and functionality of cochlear implants. Additionally, efforts to provide subsidies and enhance insurance coverage in various regions are making these devices more accessible, further driving market growth. The increasing integration of cutting-edge technologies, such as wireless connectivity and AI-driven sound processing, is also expected to enhance the functionality of cochlear implants, ensuring their continued appeal and adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 7.6% |

The market is segmented by implant type, with two primary categories: unilateral and bilateral implants. Unilateral implants are anticipated to experience robust growth, with a projected CAGR of 7.4%, reaching USD 3.3 billion by 2034. Their affordability compared to bilateral options makes them an attractive choice for patients, particularly in regions with limited reimbursement options. Unilateral implants are particularly effective for individuals with hearing loss in one ear, offering significant improvements in sound processing and communication abilities. The cost-effectiveness and targeted benefits of unilateral implants position them as a key driver of market expansion.

End-use applications for cochlear implants include ENT clinics, hospitals, and ambulatory surgical centers, with hospitals commanding the largest share of the market at 46.9% in 2024. Hospitals are the preferred choice for cochlear implant surgeries due to their access to specialized otolaryngologists, advanced diagnostic tools, and state-of-the-art surgical equipment. These facilities ensure precise implantation procedures and effective post-operative care, contributing to their dominant role in the market.

The US cochlear implants market, valued at USD 719.4 million in 2024, is projected to grow at a CAGR of 6.8% from 2025 to 2034. Increased awareness of hearing loss, greater accessibility to audiological care, and government initiatives promoting hearing healthcare are key factors driving this growth. The presence of leading cochlear implant manufacturers and comprehensive insurance coverage further strengthen the market's position, making cochlear implants an increasingly viable solution for individuals with hearing impairments in the United States.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of hearing loss

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and early diagnosis

- 3.2.1.4 Facilitative government support and improving reimbursement scenario

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cochlear implants

- 3.2.2.2 Lack of knowledge regarding hearing loss

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.7 Market size in terms of volume, 2021 - 2034 (Units)

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Consumer pathway

- 3.9 Technology landscape

- 3.10 Policy landscape

- 3.10.1 Risk management analysis

- 3.10.2 Research and development

- 3.10.3 Operations

- 3.10.4 Marketing and sales

- 3.10.5 Quality

- 3.10.6 Intellectual property rights

- 3.10.7 Regulatory

- 3.10.8 Information technology

- 3.10.9 Climate

- 3.10.10 Financial

- 3.11 Porter's analysis

- 3.12 Gap analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Unilateral implants

- 5.3 Bilateral implants

Chapter 6 Market Estimates and Forecast, By Patient Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 ENT clinics

- 7.4 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cochlear

- 9.2 Envoy Medical

- 9.3 MED-EL

- 9.4 Nurotron

- 9.5 Sonova

2025年全球人工電子耳市場報告

2025年全球人工電子耳市場報告 2025 年至 2033 年人工耳蝸市場報告(按植入類型(單側、雙側)、最終用戶(成人、兒童)和地區分類)

2025 年至 2033 年人工耳蝸市場報告(按植入類型(單側、雙側)、最終用戶(成人、兒童)和地區分類) 人工電子耳市場:2025-2029 年全球市場

人工電子耳市場:2025-2029 年全球市場 人工電子耳市場:按患者類型、最終用戶和地區進行分析和預測(2024 至 2034 年)

人工電子耳市場:按患者類型、最終用戶和地區進行分析和預測(2024 至 2034 年) 全球部分聽小骨置換假體市場研究報告 - 產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球部分聽小骨置換假體市場研究報告 - 產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 人工電子耳市場按組件類型、植入類型、患者類型、最終用戶和地區分類 - 預測至 2030 年

人工電子耳市場按組件類型、植入類型、患者類型、最終用戶和地區分類 - 預測至 2030 年 人工電子耳市場規模、佔有率和成長分析(按類型、年齡層、嚴重程度、配銷通路、最終用途和地區)- 行業預測 2025-2032

人工電子耳市場規模、佔有率和成長分析(按類型、年齡層、嚴重程度、配銷通路、最終用途和地區)- 行業預測 2025-2032 人工電子耳:市場洞察·競爭環境·市場預測 (~2030年)

人工電子耳:市場洞察·競爭環境·市場預測 (~2030年) 人工電子耳市場:依配件類型、最終用戶分類 - 2025-2030 年全球預測全球人工耳蝸市場規模:依人工耳蝸類型、最終用戶、地區、範圍和預測

人工電子耳市場:依配件類型、最終用戶分類 - 2025-2030 年全球預測全球人工耳蝸市場規模:依人工耳蝸類型、最終用戶、地區、範圍和預測