|

市場調查報告書

商品編碼

1665419

交通堵塞輔助系統市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Traffic Jam Assist System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

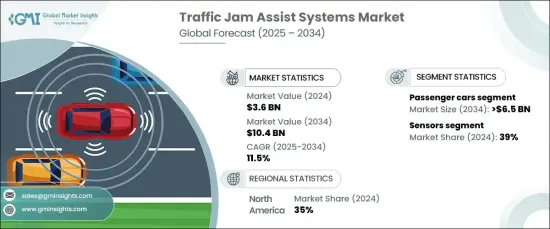

2024 年全球交通堵塞輔助系統市場價值為 36 億美元,預計 2025 年至 2034 年期間的複合年成長率為 11.5%。車輛擁有量的增加和有限的基礎設施進一步加劇了交通問題,導致通勤時間更長、壓力更大。交通堵塞輔助系統旨在透過在交通堵塞時自動執行加速、煞車和轉向等關鍵駕駛功能來緩解這種情況。這些功能不僅可以減少駕駛疲勞,還可以透過更平穩的駕駛模式提高燃油效率。對更安全、更便利的城市交通解決方案的需求日益成長,推動了其採用,特別是在面臨嚴重交通堵塞挑戰的地區。隨著製造商將先進的駕駛輔助技術融入車輛,TJA 系統作為現代移動移動關鍵組成部分的作用變得更加明顯。

汽車製造商擴大加入自適應巡航控制和車道維持輔助等功能,這些功能對於 TJA 功能至關重要。這些系統結合了各種技術來處理緩慢行駛的交通,同時確保駕駛者的安全。隨著政府執行更嚴格的安全法規,先進駕駛輔助系統的採用正在加速。消費者對更聰明、半自動駕駛汽車的興趣進一步凸顯了 TJA 系統在當今市場的相關性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 36億美元 |

| 預測值 | 104億美元 |

| 複合年成長率 | 11.5% |

市場按車型細分,2024 年乘用車將佔據 70% 以上的市場佔有率。隨著城市交通的日益緊張,消費者越來越重視能夠提升駕駛體驗的技術,這促使製造商在中檔和豪華車型中配備TJA系統。向半自動駕駛的轉變使得這些功能成為許多高階汽車的標準配置,吸引了精通技術的買家。

按組件分類,感測器在 2024 年的市佔率約為 39%。感測器融合技術的整合將來自多個來源的輸入結合在一起,增強了即時決策能力,使得 TJA 系統更加可靠,對使用者更具吸引力。

2024 年北美將引領市場,佔據全球約 35% 的佔有率。監管要求和消費者對具有先進功能的高檔汽車日益成長的需求推動了 TJA 系統的採用。該地區的汽車製造商正在積極將這些系統整合到豪華和中檔汽車中,以滿足不斷變化的安全性和便利性期望。

目錄

第 1 章:方法論與範圍

- 研究設計

- 研究方法

- 資料收集方法

- 基礎估算與計算

- 基準年計算

- 市場估計的主要趨勢

- 預測模型

- 初步研究和驗證

- 主要來源

- 資料探勘來源

- 市場範圍和定義

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 原物料供應商

- 零件供應商

- 軟體開發者

- 技術提供者

- 售後市場供應商

- 最終用戶

- 供應商概況

- 利潤率分析

- 技術與創新格局

- 成本明細分析

- 價格分析

- 專利分析

- 重要新聞及舉措

- 監管格局

- 各地區交通壅塞統計數據

- 衝擊力

- 成長動力

- 城市交通壅塞推動自動駕駛系統的需求

- 政府安全法規正在推動 ADAS 功能的採用

- 感測器、攝影機和人工智慧的進步正在提高 TJA 的可靠性

- 消費者更重視日常通勤的舒適性和便利性

- 產業陷阱與挑戰

- 整合成本高

- 惡劣天氣和複雜路況下的系統效能問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 感應器

- 雷達

- LiDAR

- 超音波

- 其他

- ECU

- 執行器

- 相機

- 其他

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- SUV

- 商用車

- 輕型商用車 (LCV)

- 重型商用車 (HCV)

第 7 章:市場估計與預測:按自動化水平,2021 - 2034 年

- 主要趨勢

- 2 級

- 3 級

- 4 級

第 8 章:市場估計與預測:按方法,2021 - 2034 年

- 主要趨勢

- 車道追蹤系統

- 車輛偵測及防撞系統

- 自動轉向和速度控制系統

- V2X 通訊整合

- 其他

第 9 章:市場估計與預測:按通訊方式,2021 - 2034 年

- 主要趨勢

- 車對車 (V2V)

- 車輛到基礎設施 (V2I)

- 基於蜂窩網路

- 專用短程通訊 (DSRC)

第 10 章:市場估計與預測:按銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第 11 章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東及非洲

- 阿拉伯聯合大公國

- 南非

- 沙烏地阿拉伯

第 12 章:公司簡介

- Aptiv PLC

- Bosch

- Continental

- Denso

- Harman

- Hitachi Astemo

- Hyundai Mobis

- Infineon Technologies

- Magna International

- Marelli

- Mercedes-Benz

- Mobileye

- NVIDIA

- NXP Semiconductors

- Renesas Electronics

- Texas Instruments

- Valeo

- Veoneer

- Volkswagen

- ZF Friedrichshafen

The Global Traffic Jam Assist System Market was valued at USD 3.6 billion in 2024 and is projected to grow at a CAGR of 11.5% from 2025 to 2034. This growth stems from worsening traffic congestion in urban areas due to rapid population growth and urbanization. Increasing vehicle ownership and limited infrastructure further exacerbate traffic problems, making commutes longer and more stressful. Traffic jam assist systems aim to alleviate this by automating key driving functions like acceleration, braking, and steering in heavy traffic. These features not only reduce driver fatigue but also enhance fuel efficiency through smoother driving patterns. The growing demand for safer and more convenient urban mobility solutions is driving adoption, particularly in regions facing severe congestion challenges. As manufacturers integrate advanced driver-assistance technologies into vehicles, the role of TJA systems as a key component of modern mobility is becoming more pronounced.

Automakers are increasingly incorporating features like adaptive cruise control and lane-keeping assistance, which are essential for TJA functionality. These systems combine various technologies to handle slow-moving traffic while ensuring driver safety. As governments enforce stricter safety regulations, the adoption of advanced driver-assistance systems is accelerating. Consumer interest in smarter, semi-autonomous vehicles further underscores the relevance of TJA systems in today's market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 11.5% |

The market is segmented by vehicle type, with passenger cars accounting for over 70% of the market share in 2024. This segment is expected to exceed USD 6.5 billion by 2034, fueled by a growing preference for advanced safety and convenience features in vehicles. As urban traffic intensifies, consumers are prioritizing technologies that enhance driving experiences, prompting manufacturers to include TJA systems in mid-range and luxury models. The shift toward semi-autonomous driving has made these features standard in many high-end vehicles, appealing to tech-savvy buyers.

When categorized by components, sensors held a market share of approximately 39% in 2024. Technological advancements in radar, LiDAR, and cameras are improving system accuracy, enabling vehicles to detect objects and navigate complex traffic scenarios with precision. The integration of sensor fusion technologies, which combine inputs from multiple sources, enhances decision-making in real-time, making TJA systems more reliable and appealing to users.

North America led the market in 2024, capturing around 35% of the global share. Regulatory requirements and growing consumer demand for premium vehicles with advanced features have driven the adoption of TJA systems. Automakers in the region are actively integrating these systems into luxury and mid-range vehicles to meet evolving expectations for safety and convenience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Software developers

- 3.1.4 Technology providers

- 3.1.5 Aftermarket providers

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Cost breakdown analysis

- 3.6 Price analysis

- 3.7 Patent analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Traffic congestion statistics, by region

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Urban traffic congestion is driving demand for automated driving systems

- 3.11.1.2 Government safety regulations are increasing the adoption of ADAS features

- 3.11.1.3 Advancements in sensors, cameras, and AI are improving the reliability of TJA

- 3.11.1.4 Consumers are prioritizing comfort and convenience in daily commutes

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High integration costs

- 3.11.2.2 System performance issues in adverse weather and complex road conditions

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Sensors

- 5.2.1 Radar

- 5.2.2 LiDAR

- 5.2.3 Ultrasonic

- 5.2.4 Others

- 5.3 ECUs

- 5.4 Actuators

- 5.5 Cameras

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Level of Automation, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Level 2

- 7.3 Level 3

- 7.4 Level 4

Chapter 8 Market Estimates & Forecast, By Method, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lane tracking system

- 8.3 Vehicle detection and collision avoidance system

- 8.4 Auto steering and speed control system

- 8.5 V2X communication integration

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Communication, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Vehicle-to-Vehicle (V2V)

- 9.3 Vehicle-to-Infrastructure (V2I)

- 9.4 Cellular network-based

- 9.5 Dedicated Short-Range Communication (DSRC)

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Aptiv PLC

- 12.2 Bosch

- 12.3 Continental

- 12.4 Denso

- 12.5 Harman

- 12.6 Hitachi Astemo

- 12.7 Hyundai Mobis

- 12.8 Infineon Technologies

- 12.9 Magna International

- 12.10 Marelli

- 12.11 Mercedes-Benz

- 12.12 Mobileye

- 12.13 NVIDIA

- 12.14 NXP Semiconductors

- 12.15 Renesas Electronics

- 12.16 Texas Instruments

- 12.17 Valeo

- 12.18 Veoneer

- 12.19 Volkswagen

- 12.20 ZF Friedrichshafen