|

市場調查報告書

商品編碼

1665261

眼科放大鏡市場機會、成長動力、產業趨勢分析與 2025 - 2034 年預測Ophthalmic Loupes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

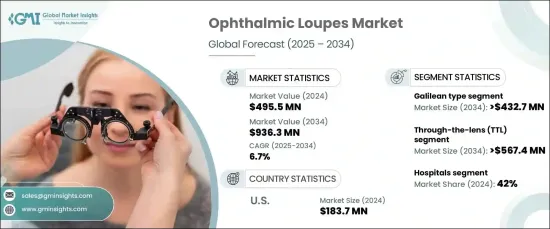

2024 年全球眼科放大鏡市場價值為 4.955 億美元,預計 2025 年至 2034 年期間複合年成長率將達到 6.7%。隨著眼部護理程序變得越來越複雜,醫療保健專業人員正在轉向使用眼科放大鏡等高精度儀器來提高手術準確性並降低風險。

人們對微創手術的日益青睞也大大促進了眼科放大鏡的普及。這些程式需要卓越的清晰度和精確度,現代放大鏡透過先進的放大技術可以提供這些功能。 LED 照明、輕質材料和人體工學設計等創新進一步提高了舒適性和可用性,鞏固了其作為醫療專業人員必備工具的地位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.955億美元 |

| 預測值 | 9.363 億美元 |

| 複合年成長率 | 6.7% |

根據產品類型,市場包括伽利略放大鏡、棱鏡放大鏡和板式放大鏡。其中,伽利略式預計將以 6.8% 的複合年成長率實現顯著成長,到 2034 年將產生 4.327 億美元的市場價值。伽利略放大鏡具有兩個或三個鏡頭的簡單光學結構,可提供清晰的放大效果,同時確保使用者在長時間使用時的舒適度。

市場還根據設計類型進行分類,包括鏡頭透照 (TTL) 設計和翻轉設計。 TTL 放大鏡預計將以 6.4% 的複合年成長率穩步成長,到 2034 年將達到 5.674 億美元。它們的人體工學特點可最大限度地減少延長手術過程中的壓力,從而提高效率和使用者滿意度。對精密工具的需求不斷成長,特別是微創眼科手術的需求,持續推動TTL領域的擴張。

2024 年美國眼科放大鏡市場規模為 1.837 億美元,預計 2025 年至 2034 年期間的複合年成長率為 6.2%。這些情況需要精確的診斷和手術干預,從而增加了對眼科放大鏡等專用工具的需求。此外,人口老化以及糖尿病和慢性病發病率的上升進一步凸顯了美國對先進眼科解決方案的需求

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 眼科疾病盛行率不斷上升

- 眼科手術數量不斷增加

- 放大鏡的技術進步

- 微創手術需求不斷成長

- 轉向符合人體工學和可自訂的設計

- 產業陷阱與挑戰

- 高級放大鏡成本高

- 客製化和適配方面的挑戰

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按產品類型,2021 年至 2034 年

- 主要趨勢

- 伽利略型

- 棱柱型

- 平板放大鏡類型

第6章:市場估計與預測:依設計類型,2021 – 2034 年

- 主要趨勢

- 鏡頭拍攝 (TTL)

- 向上翻轉

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 眼科診所

- 門診手術中心 (ASC)

- 其他最終用戶

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- DentLight

- Designs for Vision

- ErgonoptiX

- Heine Optotechnik

- Keeler

- Lumadent

- NEITZ

- Ocutech

- Orascoptic

- Q-Optics

- Rudolf Riester

- SHEERVISION

- SurgiTel

- Univet

- ZEISS

The Global Ophthalmic Loupes Market was valued at USD 495.5 million in 2024 and is forecasted to grow at an impressive CAGR of 6.7% from 2025 to 2034. This robust growth is fueled by the rising demand for precision tools in ophthalmic surgeries. As eye care procedures become increasingly intricate, healthcare professionals are turning to high-precision instruments like ophthalmic loupes to enhance surgical accuracy and reduce risks.

The growing preference for minimally invasive surgeries has also significantly contributed to the adoption of ophthalmic loupes. These procedures demand exceptional clarity and precision, which modern loupes provide through advanced magnification technologies. Innovations such as LED lighting, lightweight materials, and ergonomic designs have further enhanced comfort and usability, solidifying their position as essential tools for medical professionals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $495.5 Million |

| Forecast Value | $ 936.3 Million |

| CAGR | 6.7% |

By product type, the market includes galilean, prismatic, and plate loupes. Among these, the galilean type is expected to witness remarkable growth at a CAGR of 6.8%, generating USD 432.7 million by 2034. Its widespread appeal lies in its affordability, ease of use, and lightweight design, making it an excellent choice for routine ophthalmic tests and surgeries. Featuring a straightforward optical structure with two or three lenses, galilean loupes provide clear magnification while ensuring user comfort during prolonged use.

The market is also categorized by design type, including through-the-lens (TTL) and flip-up designs. TTL loupes are projected to experience steady growth at a CAGR of 6.4%, reaching USD 567.4 million by 2034. Renowned for their custom-built design, TTL loupes offer unparalleled optical clarity tailored to individual needs. Their ergonomic features minimize strain during extended procedures, enhancing both efficiency and user satisfaction. The rising demand for precision tools, particularly in minimally invasive eye surgeries, continues to propel the expansion of the TTL segment.

The U.S. ophthalmic loupes market accounted for USD 183.7 million in 2024 and is anticipated to grow at a CAGR of 6.2% between 2025 and 2034. Factors driving this growth include the increasing prevalence of ophthalmic conditions such as cataracts, glaucoma, diabetic retinopathy, and macular degeneration. These conditions require precise diagnostic and surgical interventions, elevating the demand for specialized tools like ophthalmic loupes. Additionally, an aging population and the growing incidence of diabetes and chronic diseases further underscore the need for advanced ophthalmic solutions in the U.S.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of ophthalmic disorders

- 3.2.1.2 Rising number of ophthalmic surgeries

- 3.2.1.3 Technological advancements in loupes

- 3.2.1.4 Growing demand for minimally invasive procedures

- 3.2.1.5 Shift toward ergonomic and customizable designs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced loupes

- 3.2.2.2 Challenges in customization and fit

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Galilean type

- 5.3 Prismatic type

- 5.4 Plate loupe type

Chapter 6 Market Estimates and Forecast, By Design Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Through-the-lens (TTL)

- 6.3 Flip up

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ophthalmic clinics

- 7.4 Ambulatory surgical centers (ASCs)

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 DentLight

- 9.2 Designs for Vision

- 9.3 ErgonoptiX

- 9.4 Heine Optotechnik

- 9.5 Keeler

- 9.6 Lumadent

- 9.7 NEITZ

- 9.8 Ocutech

- 9.9 Orascoptic

- 9.10 Q-Optics

- 9.11 Rudolf Riester

- 9.12 SHEERVISION

- 9.13 SurgiTel

- 9.14 Univet

- 9.15 ZEISS