|

市場調查報告書

商品編碼

2038704

牛奶替代品市場機會、成長要素、產業趨勢分析及2026-2035年預測。Milk Alternatives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

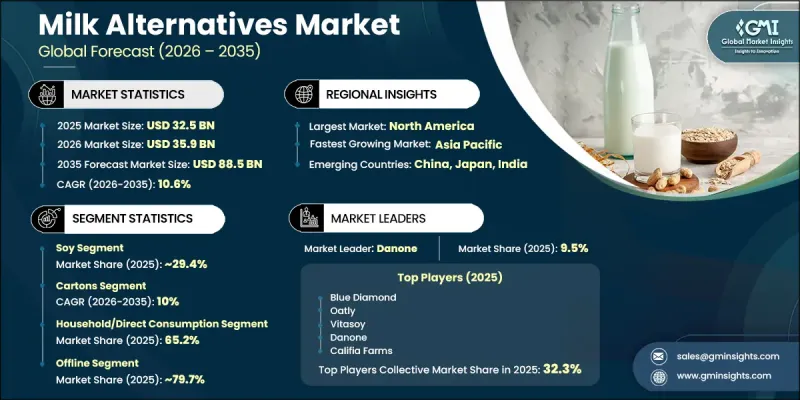

預計到 2025 年,全球牛奶替代品市場價值將達到 325 億美元,並預計以 10.6% 的複合年成長率成長,到 2035 年達到 885 億美元。

受飲食習慣向植物來源營養轉變以及消費者對乳糖不耐症和乳製品過敏意識增強的推動,該市場正經歷強勁且持續的成長。素食主義和彈性素食主義等生活方式的日益普及,進一步提升了全球市場對無乳飲料的需求。人們對傳統乳製品生產環境影響的擔憂,也推動了向永續食品選擇。整體產業前景顯示,在消費者期望的改變和產品多樣化的推動下,消費習慣正穩步向更健康、更永續和更符合倫理的方向轉變。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 325億美元 |

| 預測市場規模 | 885億美元 |

| 複合年成長率 | 10.6% |

牛奶替代品涵蓋了種類繁多的植物來源飲品,旨在取代日常消費中的傳統乳製品。這些產品深受乳糖不耐症、乳製品過敏以及素食者的青睞。同時,它們也受到注重健康的消費者的歡迎,因為他們追求低卡路里和低飽和脂肪的選擇。為了提高其營養價值,生產商正不斷在這些飲品中添加鈣、維生素D和維生素B12等必需營養素,以使其營養成分與牛奶更接近。牛奶替代品的應用範圍也從直接飲用擴展到烹飪、烘焙和飲品調製等領域。咖啡館、餐廳和家庭廚房中牛奶替代品的日益普及,進一步推動了市場滲透率和長期需求的成長。

預計到2025年,豆奶市佔率將達到29.4%,並在2035年之前以10%的複合年成長率成長。豆奶憑藉其高蛋白含量和成本績效,仍然是最成熟的植物性飲品之一。其在市場上的長期地位和穩定的營養成分使其保持了強大的消費者信任。豆奶仍是廣泛普及且用途廣泛的選擇,深受新舊植物性飲品消費者的青睞。

預計到2025年,紙盒包裝市佔率將達到58.8%,並在2026年至2035年間以10%的複合年成長率成長。隨著永續性和便利性日益受到重視,包裝創新在植物奶產業中扮演著至關重要的角色。紙盒包裝憑藉其輕盈的結構、易於儲存以及與環保意識強的消費者趨勢的高度親和性,仍然佔據主導地位。其可回收性和對環境的低影響使其成為永續性的製造商和消費者的首選。包裝設計的不斷進步進一步提升了產品的展示效果和功能性。

預計到2025年,北美牛奶替代品市佔率將達到34.1%。在該地區,消費者對健康、有機和植物來源產品的偏好明顯,這主要得益於人們對健康和永續生活方式的日益重視。生產流程的技術進步,包括自動化和智慧包裝解決方案,正在提高效率並減少對環境的影響。該地區對永續採購慣例和環保包裝的投資也在增加。這些趨勢,加上完善的零售基礎設施和不斷變化的食品偏好,將繼續推動北美市場的成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依原料分類,2022-2035年

- 大豆

- 杏仁

- 椰子

- 燕麥

- 米

- 其他

第6章 市場估價與預測:依包裝類型分類,2022-2035年

- 紙箱

- 玻璃瓶

- 其他

第7章 市場估計與預測:依應用領域分類,2022-2035年

- 食品/飲料加工

- 冰淇淋和冷凍甜點

- 麵包糖果甜點

- 營養飲料與蛋白質奶昔

- 其他

- 餐飲服務業/HoReCa

- 咖啡館和咖啡店

- 餐廳

- 飯店餐飲

- 家庭使用/直接消費

- 飲料

- 烹飪和烘焙

- 可作為麥片或早餐。

第8章 市場估算與預測:依通路分類,2022-2035年

- 線上

- 電子商務

- 品牌官方網站

- 離線

- 超級市場/大賣場

- 專賣店

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- Blue Diamond

- Califia Farms

- Danone

- DREAM Plant Based

- Elmhurst 1925

- Good Karma Foods

- Kikkoman

- milkadamia

- Minor Figures

- Miyoko's Creamery

- nutpods

- Oatly

- Ripple Foods

- Vitasoy

The Global Milk Alternatives Market was valued at USD 32.5 billion in 2025 and is estimated to grow at a CAGR of 10.6% to reach USD 88.5 billion by 2035.

The market has been witnessing strong and sustained growth, driven by shifting dietary preferences toward plant-based nutrition and increasing consumer awareness regarding lactose intolerance and dairy sensitivities. Rising adoption of vegan and flexitarian lifestyles has further strengthened demand for dairy-free beverage options across global markets. Environmental concerns related to traditional dairy production have also contributed to the shift toward sustainable food consumption patterns. The market continues to benefit from continuous product innovation, improved taste profiles, and enhanced nutritional formulations that closely replicate conventional dairy. Expanding retail penetration and foodservice adoption have further supported category growth, making milk alternatives a mainstream dietary choice. The overall industry outlook reflects a steady transition toward healthier, sustainable, and ethically driven consumption habits supported by evolving consumer expectations and product diversification.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $32.5 Billion |

| Forecast Value | $88.5 Billion |

| CAGR | 10.6% |

The milk alternatives category includes a wide range of plant-based beverages designed to replace traditional dairy products in everyday consumption. These products are widely used by individuals who are lactose intolerant, allergic to dairy, or following vegan and vegetarian diets. They also appeal to health-conscious consumers seeking lower-calorie and reduced saturated fat options. Manufacturers increasingly fortify these beverages with essential nutrients, including calcium, vitamin D, and vitamin B12, to improve their nutritional equivalence to cow's milk. Beyond direct consumption, these products are extensively used in cooking, baking, and beverage preparation, further expanding their application scope. Their growing adoption across cafes, restaurants, and household kitchens continues to reinforce market penetration and long-term demand.

The soy segment accounted for 29.4% share in 2025 and is projected to grow at a CAGR of 10% through 2035. Soy-based milk remains one of the most established plant-based alternatives, supported by its high protein content and cost-effectiveness. Its long-standing presence in the market and consistent nutritional profile have helped maintain strong consumer trust. Soy milk continues to serve as a widely accessible and versatile option, making it a preferred choice among both new and existing consumers of plant-based beverages.

The cartons segment held a 58.8% share in 2025 and is expected to grow at a CAGR of 10% during 2026 to 2035. Packaging innovation plays a crucial role in the milk alternatives industry, with increasing emphasis on sustainability and convenience. Carton packaging remains dominant due to its lightweight structure, ease of storage, and strong alignment with environmentally responsible consumption trends. Its recyclability and reduced environmental footprint make it a preferred choice among manufacturers and consumers focused on sustainability. Continued advancements in packaging design are further enhancing product shelf appeal and functionality.

North America Milk Alternatives Industry accounted for a 34.1% share in 2025. The region demonstrates high consumer preference for health-focused, organic, and plant-based products, supported by increasing awareness of wellness and sustainable living practices. Technological advancements in production processes, including automation and smart packaging solutions, are improving efficiency and reducing environmental impact. The region is also witnessing growing investment in sustainable sourcing practices and eco-friendly packaging initiatives. These developments, combined with strong retail infrastructure and evolving dietary preferences, continue to strengthen market growth across North America.

Key players operating in the Global Milk Alternatives Market include Oatly, Danone, Califia Farms, Blue Diamond, Ripple Foods, Vitasoy, Elmhurst 1925, Good Karma Foods, Minor Figures, Miyoko's Creamery, nutpods, milkadamia, Kikkoman, and DREAM Plant Based. Companies in the Milk Alternatives Market are focusing on product innovation, portfolio expansion, and sustainability-driven strategies to strengthen their competitive position. Manufacturers are investing heavily in research and development to enhance taste, texture, and nutritional profiles, making plant-based beverages more comparable to traditional dairy. Expansion of product lines across multiple plant sources is helping companies cater to diverse consumer preferences. Strategic partnerships with retail chains and foodservice providers are improving product accessibility and market penetration. Brands are also prioritizing sustainable sourcing and eco-friendly packaging solutions to align with environmental expectations. Digital marketing and influencer collaborations are being used to strengthen brand visibility and consumer engagement. Additionally, companies are focusing on regional expansion and pricing strategies to capture emerging demand across both developed and developing markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Packaging type

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soy

- 5.3 Almond

- 5.4 Coconut

- 5.5 Oats

- 5.6 Rice

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cartons

- 6.3 Glass bottles

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage processing

- 7.2.1 Ice cream & frozen desserts

- 7.2.2 Bakery & confectionery

- 7.2.3 Nutritional beverages & protein shakes

- 7.2.4 Others

- 7.3 Food service/HoReCa

- 7.3.1 Cafes & coffee shops

- 7.3.2 Restaurants

- 7.3.3 Hotels & catering

- 7.4 Household/direct consumption

- 7.4.1 Drinking

- 7.4.2 Cooking & baking

- 7.4.3 Cereal & breakfast applications

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Brand websites

- 8.3 Offline

- 8.3.1 Supermarkets/hypermarkets

- 8.3.2 Specialty stores

- 8.3.3 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Blue Diamond

- 10.2 Califia Farms

- 10.3 Danone

- 10.4 DREAM Plant Based

- 10.5 Elmhurst 1925

- 10.6 Good Karma Foods

- 10.7 Kikkoman

- 10.8 milkadamia

- 10.9 Minor Figures

- 10.10 Miyoko's Creamery

- 10.11 nutpods

- 10.12 Oatly

- 10.13 Ripple Foods

- 10.14 Vitasoy

乳製品替代品市場規模、佔有率和成長分析:按產品類型、形式、類別、牲畜種類、通路和地區分類 - 2026-2033 年行業預測

乳製品替代品市場規模、佔有率和成長分析:按產品類型、形式、類別、牲畜種類、通路和地區分類 - 2026-2033 年行業預測 全球代乳品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虎堅果奶全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球代乳品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)虎堅果奶全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 液態奶粉市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、畜牧業、地區和競爭格局分類,2021-2031年全球乳製品替代品市場:預測(2025-2030)

液態奶粉市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、畜牧業、地區和競爭格局分類,2021-2031年全球乳製品替代品市場:預測(2025-2030) 2032 年液態奶替代品市場預測:按產品、類型、配方類型、牲畜、分銷管道和地區進行的全球分析全球乳製品替代品市場,預測到 2030 年:按類型、牲畜、原產地、形式、分銷管道、最終用戶、地區

2032 年液態奶替代品市場預測:按產品、類型、配方類型、牲畜、分銷管道和地區進行的全球分析全球乳製品替代品市場,預測到 2030 年:按類型、牲畜、原產地、形式、分銷管道、最終用戶、地區