|

市場調查報告書

商品編碼

1665225

非骨水泥全膝關節系統 (TKS) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cementless Total Knee Systems (TKS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

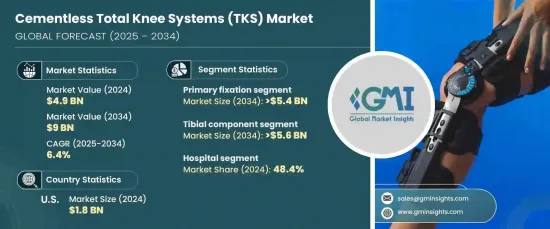

2024 年全球無骨水泥全膝關節系統市場價值為 49 億美元,預計 2025 年至 2034 年期間將以 6.4% 的複合年成長率強勁成長。與傳統的骨水泥植入物相比,非骨水泥膝關節系統因其出色的耐用性、更快的恢復時間和更低的併發症風險而越來越受到青睞。

骨關節炎的發生率不斷上升,尤其是在老年族群中,這持續推動全膝關節置換術的需求。隨著全球人口老化,對非骨水泥系統等先進、微創解決方案的需求日益增加。這些植入物具有促進更快的骨整合、增強長期穩定性和最大限度地降低術後風險的優勢,成為外科醫生和患者的首選。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 49億美元 |

| 預測值 | 90億美元 |

| 複合年成長率 | 6.4% |

市場根據注視類型分為主要注視和混合注視。其中,初級固定由於其無需使用骨水泥就能提供增強的初始穩定性和改善的骨整合而處於領先地位。這種方法可以使植入物直接與骨頭結合,促進更快癒合並確保長期耐用性。手術工具和技術的技術創新進一步推動了初級固定系統的採用。

就零件而言,市場分為脛骨部件和股骨部件。脛骨組件佔有相當大的市場佔有率,預計在預測期內將穩定成長。它在支撐體重和維持關節穩定性方面發揮著至關重要的作用,使其成為膝關節置換系統中必不可少的元素。模組化設計的最新進展提高了脛骨部件的性能,減少了植入物鬆動並改善了患者的治療效果。

2024 年,美國非骨水泥全膝關節系統市場產值達到 18 億美元。對實現更好的手術結果和減少恢復時間的關注繼續推動全國非骨水泥系統的應用。

目錄

第 1 章:方法論與範圍

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 全球骨關節炎和類風濕性關節炎盛行率上升

- 微創手術技術的應用日益廣泛

- 非骨水泥固定方法的技術進步

- 老年人口不斷成長,易患關節疾病

- 產業陷阱與挑戰

- 非骨水泥膝關節系統成本高

- 成長動力

- 成長潛力分析

- 監管格局

- 報銷場景

- 技術格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未來市場趨勢

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第 5 章:市場估計與預測:按固定方法,2021 年至 2034 年

- 主要趨勢

- 初級注視

- 混合固定

第6章:市場估計與預測:按組件,2021 – 2034 年

- 主要趨勢

- 脛骨組件

- 股骨假體

第 7 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 骨科中心

- 其他最終用途

第 8 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Aesculap

- Conformis

- Corin Group

- Dentsply Sirona

- DePuy Synthes

- Enovis

- Episurf Medical

- Exactech

- Medacta International

- MicroPort Orthopedics

- Smith & Nephew

- Stryker

- United Orthopedic

- Waldemar Link

- Zimmer Biomet

The Global Cementless Total Knee Systems Market was valued at USD 4.9 billion in 2024 and is projected to experience robust growth at a CAGR of 6.4% from 2025 to 2034. This growth is fueled by the rising prevalence of osteoarthritis and rheumatoid arthritis alongside an aging population worldwide. Cementless knee systems are increasingly favored due to their exceptional durability, faster recovery times, and reduced risk of complications compared to traditional cemented implants.

The growing incidence of osteoarthritis, particularly among older adults, continues to drive the demand for total knee replacements. As the global population ages, there is an escalating need for advanced and minimally invasive solutions such as cementless systems. These implants offer the advantage of promoting faster bone integration, enhancing long-term stability, and minimizing post-operative risks, making them the preferred choice for both surgeons and patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $9 Billion |

| CAGR | 6.4% |

The market is segmented by fixation type into primary fixation and hybrid fixation. Among these, primary fixation leads the segment due to its ability to provide enhanced initial stability and improved osseointegration without the need for bone cement. This approach allows the implant to bond directly with the bone, fostering faster healing and ensuring long-term durability. Technological innovations in surgical tools and techniques have further boosted the adoption of primary fixation systems.

In terms of components, the market is categorized into tibial and femoral components. The tibial component holds a significant market share and is expected to witness steady growth over the forecast period. Its vital role in supporting body weight and maintaining joint stability makes it an essential element in knee replacement systems. Recent advancements in modular designs have enhanced the performance of tibial components, reducing implant loosening and improving patient outcomes.

The U.S. cementless total knee systems market generated USD 1.8 billion in 2024. This growth is driven by a large aging population, an increasing number of knee replacement surgeries, and advancements in healthcare infrastructure. The focus on achieving better surgical outcomes and reducing recovery times continues to fuel the adoption of cementless systems across the country.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of osteoarthritis and rheumatoid arthritis globally

- 3.2.1.2 Increasing adoption of minimally invasive surgical techniques

- 3.2.1.3 Technological advancements in cementless fixation methods

- 3.2.1.4 Growing geriatric population prone to joint disorders

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with cementless knee systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Fixation Method, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Primary fixation

- 5.3 Hybrid fixation

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Tibial component

- 6.3 Femoral component

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Orthopedic centers

- 7.4 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aesculap

- 9.2 Conformis

- 9.3 Corin Group

- 9.4 Dentsply Sirona

- 9.5 DePuy Synthes

- 9.6 Enovis

- 9.7 Episurf Medical

- 9.8 Exactech

- 9.9 Medacta International

- 9.10 MicroPort Orthopedics

- 9.11 Smith & Nephew

- 9.12 Stryker

- 9.13 United Orthopedic

- 9.14 Waldemar Link

- 9.15 Zimmer Biomet