|

市場調查報告書

商品編碼

1665032

裝袋機市場機會、成長動力、產業趨勢分析與 2024 - 2032 年預測Bagging Machines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

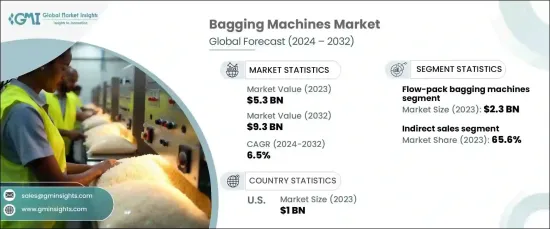

2023 年全球裝袋機市場價值為 53 億美元,預計在 2024 年至 2032 年期間將以 6.5% 的強勁複合年成長率成長。市場依產品類型細分,包括流動包裝袋裝機、條狀包裝袋裝機、重量包裝袋裝機、真空包裝袋裝機等。

2023 年,流動包裝袋裝機引領市場,為總市場價值貢獻了 23 億美元。預計到 2032 年,這一領域的複合年成長率將達到 6.6%,這得益於其在處理不同包裝需求方面的適應性和效率。這些機器對於包裝從食品到醫療設備等各種產品至關重要,它們使用可實現客製化設計的靈活材料。它們的高速和可靠性使其成為大規模生產的理想選擇,而自動化和物聯網整合的進步進一步增強了它們的功能,滿足了對智慧包裝解決方案日益成長的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2023 |

| 預測年份 | 2024-2032 |

| 起始值 | 53億美元 |

| 預測值 | 93億美元 |

| 複合年成長率 | 6.5% |

市場也按分銷管道分類,包括直接銷售和間接銷售。 2023年,間接銷售領域佔據主導地位,佔約65.6%的市場。預計預測期內該部分的複合年成長率為 6.6%。分銷商、經銷商和第三方供應商等中間商在彌合製造商和最終用戶之間的差距方面發揮關鍵作用,尤其是在新興市場。透過管理物流、提供在地化專業知識和客戶支持,這些管道使製造商能夠專注於生產和創新,同時接觸更廣泛的客戶群。

2023 年,美國裝袋機市場規模達 10 億美元,預計到 2032 年複合年成長率將達到 6.6%。自動化程度的不斷提高,加上對客製化、高效和永續包裝解決方案的需求不斷成長,推動了這一成長。物聯網機械的引入和環保材料的使用進一步增強了市場的發展軌跡。作為全球裝袋機領域的領導者,美國不斷提供不同應用的創新解決方案,確保符合監管標準和不斷變化的消費者偏好。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測參數

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 自動化和工業 4.0 整合

- 包裝商品需求不斷成長

- 機器效率和客製化的進步

- 產業陷阱與挑戰

- 初期資本投入高

- 維護和停機問題

- 成長動力

- 成長潛力分析

- 技術概覽

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按產品類型,2021 年至 2032 年

- 主要趨勢

- 流動包裝袋裝機

- 條形袋裝機

- 稱重裝袋機

- 真空袋裝機

- 其他

第6章:市場估計與預測:依資料,2021 – 2032 年

- 主要趨勢

- 塑膠袋

- 紙袋

- 聚丙烯袋

- 編織袋

第 7 章:市場估計與預測:按自動化,2021 年至 2032 年

- 主要趨勢

- 手動裝袋機

- 半自動裝袋機

- 全自動裝袋機

第 8 章:市場估計與預測:按應用,2021 年至 2032 年

- 主要趨勢

- 食品和飲料

- 藥品

- 化學品

- 建造

- 消費品

- 其他

第 9 章:市場估計與預測:按配銷通路,2021 年至 2032 年

- 主要趨勢

- 直接銷售

- 間接銷售

第 10 章:市場估計與預測:按地區,2021 年至 2032 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第 11 章:公司簡介

- BEUMER Group GmbH & Co. KG

- Cemen Tech, Inc.

- CFT SpA

- Duravant LLC

- FLSmidth & Co. A/S

- Haver & Boecker OHG

- Meyer Industries, Inc.

- MULTIVAC Sepp Haggenmüller SE & Co. KG

- Niverplast BV

- Pakona Engineers (I) Pvt. Ltd.

- Premier Tech Ltd.

- Robatech AG

- Schneider Packaging Equipment Co., Inc.

- Tetra Pak International SA

- Waldner Holding GmbH & Co. KG

The Global Bagging Machines Market, valued at USD 5.3 billion in 2023, is poised to grow at a robust CAGR of 6.5% from 2024 to 2032. This growth is fueled by increasing demand for automation and efficiency in packaging processes across various industries. The market is segmented by product type, encompassing flow-pack bagging machines, stick pack bagging machines, weight bagging machines, vacuum bagging machines, and others.

Flow-pack bagging machines led the market in 2023, contributing USD 2.3 billion to the total market value. This segment is projected to grow at a CAGR of 6.6% through 2032, driven by its adaptability and efficiency in handling diverse packaging needs. These machines are essential for packaging a wide range of products, from food items to medical equipment, using flexible materials that enable customized designs. Their high speed and reliability make them ideal for large-scale production, while advancements in automation and IoT integration have further enhanced their functionality, meeting the growing demand for intelligent packaging solutions.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $5.3 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 6.5% |

The market is also categorized by distribution channels, including direct and indirect sales. In 2023, the indirect sales segment dominated, capturing approximately 65.6% of the market share. This segment is expected to grow at a CAGR of 6.6% over the forecast period. Intermediaries such as distributors, resellers, and third-party vendors play a pivotal role in bridging the gap between manufacturers and end-users, particularly in emerging markets. By managing logistics, providing localized expertise, and offering customer support, these channels enable manufacturers to focus on production and innovation while reaching a broader customer base.

The U.S. bagging machines market accounted for USD 1 billion in 2023 and is set to expand at an estimated CAGR of 6.6% through 2032. The market thrives on strong demand from industrial and consumer goods sectors, particularly in the food, beverage, pharmaceutical, and e-commerce industries. Increasing adoption of automation, coupled with a growing need for customized, efficient, and sustainable packaging solutions, drives this growth. The incorporation of IoT-enabled machinery and the use of eco-friendly materials further bolster the market's trajectory. As a leader in the global bagging machines sector, the U.S. continues to deliver innovative solutions tailored to diverse applications, ensuring compliance with regulatory standards and evolving consumer preferences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Automation and industry 4.0 integration

- 3.6.1.2 Rising demand for packaged goods

- 3.6.1.3 Advancements in machine efficiency and customization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial capital investment

- 3.6.2.2 Maintenance and downtime issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Technological overview

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 – 2032, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Flow-pack bagging machines

- 5.3 Stick pack bagging machines

- 5.4 Weight bagging machines

- 5.5 Vacuum bagging machines

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021 – 2032, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic bags

- 6.3 Paper bags

- 6.4 Polypropylene bags

- 6.5 Woven bags

Chapter 7 Market Estimates & Forecast, By Automation, 2021 – 2032, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual bagging machines

- 7.3 Semi-automatic bagging machines

- 7.4 Fully automatic bagging machines

Chapter 8 Market Estimates & Forecast, By Application, 2021 – 2032, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.3 Pharmaceuticals

- 8.4 Chemicals

- 8.5 Construction

- 8.6 Consumer goods

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 – 2032, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2032, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 BEUMER Group GmbH & Co. KG

- 11.2 Cemen Tech, Inc.

- 11.3 CFT S.p.A.

- 11.4 Duravant LLC

- 11.5 FLSmidth & Co. A/S

- 11.6 Haver & Boecker OHG

- 11.7 Meyer Industries, Inc.

- 11.8 MULTIVAC Sepp Haggenmüller SE & Co. KG

- 11.9 Niverplast B.V.

- 11.10 Pakona Engineers (I) Pvt. Ltd.

- 11.11 Premier Tech Ltd.

- 11.12 Robatech AG

- 11.13 Schneider Packaging Equipment Co., Inc.

- 11.14 Tetra Pak International S.A.

- 11.15 Waldner Holding GmbH & Co. KG

全球包裝設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球包裝設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 製袋機市場:依型號、自動化程度、包裝材料、終端用戶產業和袋子尺寸分類-2026-2032年全球市場預測

製袋機市場:依型號、自動化程度、包裝材料、終端用戶產業和袋子尺寸分類-2026-2032年全球市場預測 2026年全球固體包裝機市場報告2026年全球球門袋包裝機市場報告2026年全球聚乙烯袋包裝機市場報告2026年全球袋裝包裝機市場報告2026年全球袋裝填充設備市場報告

2026年全球固體包裝機市場報告2026年全球球門袋包裝機市場報告2026年全球聚乙烯袋包裝機市場報告2026年全球袋裝包裝機市場報告2026年全球袋裝填充設備市場報告 包裝機械市場規模、佔有率和成長分析(按機器類型、自動化程度、材料、產能和地區分類)-2026-2033年產業預測

包裝機械市場規模、佔有率和成長分析(按機器類型、自動化程度、材料、產能和地區分類)-2026-2033年產業預測 2025-2035年全球捆紮機市場

2025-2035年全球捆紮機市場 裝袋機市場報告:趨勢、預測和競爭分析(至 2031 年)

裝袋機市場報告:趨勢、預測和競爭分析(至 2031 年)