|

市場調查報告書

商品編碼

1822644

醫院資訊系統市場機會、成長動力、產業趨勢分析及2025-2034年預測Hospital Information System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

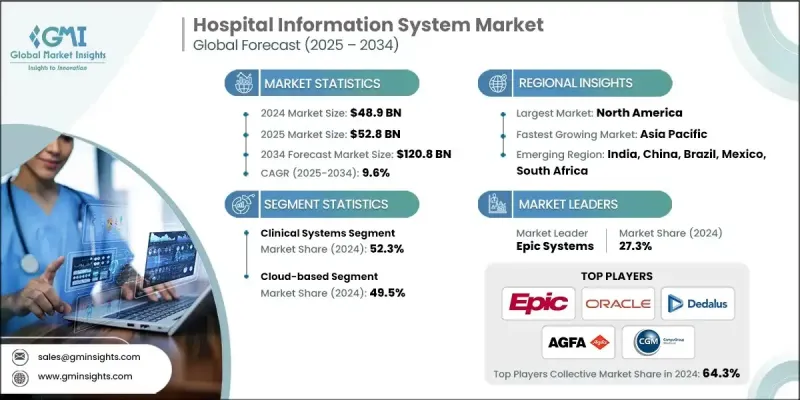

根據 Global Market Insights, Inc. 發布的最新報告,2024 年全球醫院資訊系統 (HIS) 市場價值為 489 億美元,預計將從 2025 年的 528 億美元成長到 2034 年的 1,208 億美元,複合年成長率為 9.6%。

醫療保健數位化的不斷發展、對可互通解決方案日益成長的需求以及對最佳化臨床工作流程日益成長的需求,正在推動全球範圍內 HIS 的採用。越來越多的醫院選擇整合軟體系統來處理病歷、臨床資訊、醫療帳單和法規遵循。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 489億美元 |

| 預測值 | 1208億美元 |

| 複合年成長率 | 9.6% |

關鍵促進因素:

1.綜合臨床和行政資料管理的要求:醫院正在實施HIS,以便整合跨部門的不同工作流程。

2.慢性病負擔加重和人口老化:有效的患者追蹤和最佳化治療需要先進的健康資訊平台。

3.基於雲端和人工智慧的系統的採用:雲端的採用因其較低的 IT 基礎設施費用、靈活性和遠端存取而變得越來越流行。

4.合規性和資料安全:國際和地區法規迫使醫院實施合規、安全和可審計的系統。

關鍵參與者:

- Epic 將在 2024 年佔據醫院資訊系統市場的主導地位,市佔率為 27.3%。

- Oracle 正在利用其收購 Cerner 的既有 HIS/EHR 地位以及其在雲端運算、資料分析和人工智慧方面的優勢。

- Dedalus 是歐洲市場領導者,高度重視互通性和開放的數位健康生態系統。

主要挑戰:

- 互通性限制: HIS 與遺留系統、實驗室、成像和第三方平台的整合仍然具有挑戰性。

- 高昂的培訓和實施費用:客製化、遷移和員工入職的初始投資可能很高。

- 安全和資料隱私威脅:人們對健康資料外洩和勒索軟體的擔憂日益加劇,推動了合規性和安全雲端部署的提高。

1. 依系統組件分類-臨床系統正在興起

2024年,臨床系統組件佔據HIS市場的最大佔有率,約66%。以EMR、CPOE、LIS、RIS為代表的臨床系統組件是醫院日常運作的堅實基礎。

2. 按部署-基於雲端的解決方案正在興起

由於可擴展性增強、基礎設施建設資本支出降低以及遠端應用程式存取能力增強,基於雲端的 HIS 部署正在加速。各地區的醫院正在部署雲端解決方案,以改善營運、協作和持續護理。

3. 按地區分類-北美依然強勁

2024年,北美繼續佔據最大市場佔有率,憑藉強大的政府支持、極高的數位素養以及公立和私立醫院的強勁成長,北美保持了其在醫院資訊系統市場的主導地位。憑藉強大的醫療基礎設施、電子病歷(EHR)的廣泛採用、HIPAA和HITECH等政府法規的實施以及日益成長的基於雲端的醫療IT解決方案,北美在醫院資訊系統市場保持了主導地位。美國醫院和醫療網路正在迅速將臨床決策支援、人口健康分析和遠距護理模組整合到其核心醫院系統中。

醫院資訊系統市場的一些主要參與者包括 AGFA Healthcare、CAMBIO、ChipSoft、CompuGroup Medical、Dedalus、Docaposte、Engineering Ingegneria Informatica、Epic Systems、InterSystems、Meierhofer AG、NextGen、Nexus、Oracle、SECTRA 和 Veradigm。

市場上主要的 HIS 參與者正在利用雲端整合、向其他地區擴展、支援 AI 的模組以及與醫療保健領導者達成的合作協議來打造競爭優勢。 Epic Systems 繼續引領北美市場,與表現最佳的醫療系統達成長期協議。 Dedalus 和 InterSystems 正在擴展其雲端平台並添加互通功能。 CompuGroup Medical 和 AGFA Healthcare 正在將決策支援功能整合到其 HIS 平台中。甲骨文在收購 Cerner 後,正在整合其整合的雲端和資料分析功能,最終為 EHR 和人口健康提供更有價值的模組。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 數位健康解決方案的採用率不斷提高

- 政府措施和法規

- 醫療保健支出不斷增加

- 全面醫療保健系統需求激增

- 產業陷阱與挑戰

- 實施和維護成本高

- 資料安全和隱私問題

- 市場機會

- 政府醫療數位化措施不斷增加

- 對分析和商業智慧工具的需求不斷成長

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 技術格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 消費者行為和趨勢

- 各地區醫院數量

- 醫院數位生態系概述

- 電子病歷(EMR)/電子健康紀錄(EHR)

- 遠距醫療和遠距病人監控

- 網路安全和資料保護

- 波特的分析

- PESTEL分析

- 人工智慧與電子病歷 (EMR) 的整合

- 差距分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲和中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按系統組件,2021 - 2034 年

- 主要趨勢

- 臨床系統

- 電子病歷(EMR)/電子健康紀錄(EHR)

- 放射資訊系統(RIS)

- 藥房資訊系統

- 實驗室資訊系統(LIS)

- 其他臨床系統

- 行政/後台系統

- 財務和計費

- 供應鏈管理

- 設施管理/人力資源

- 作業系統

- 入院、出院及轉院 (ADT)/床位管理系統 (BMS)

- 營運標準支援/調度系統

- 面向患者的技術

- 行動健康應用程式

- 患者門戶

- 整合層

- 介面引擎/API

- 健康資訊交換(HIE)

- 資料和安全

- 臨床資料儲存庫

- 身分和存取管理 (IAM)

- 一般資料保護規範(GDPR)

第6章:市場估計與預測:按部署,2021 - 2034 年

- 主要趨勢

- 基於雲端

- 基於網路

- 本地部署

第7章:市場估計與預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- AGFA Healthcare

- CAMBIO

- ChipSoft

- CompuGroup Medical

- Dedalus

- Docaposte

- Engineering Ingegneria Informatica

- Epic Systems

- InterSystems

- Meierhofer AG

- NextGen

- Nexus

- Oracle

- SECTRA

- Veradigm

The global hospital information system (HIS) market was valued at USD 48.9 billion in 2024 and is projected to grow from USD 52.8 billion in 2025 to USD 120.8 billion by 2034, expanding at a CAGR of 9.6%, according to the latest report published by Global Market Insights, Inc.

Growing healthcare digitization, increasing requirements for interoperable solutions, and mounting need for optimized clinical workflows are driving the adoption of HIS around the world. Hospitals are increasingly opting for integrated software systems to handle patient records, clinical information, medical billing, and regulatory adherence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $48.9 Billion |

| Forecast Value | $120.8 Billion |

| CAGR | 9.6% |

Key Drivers:

1. Requirement for integrated clinical and administrative data management: Hospitals are implementing HIS in order to integrate disparate workflows across departments.

2. Increased burden of chronic diseases and aging population: Effective patient tracking and optimized treatment require advanced health information platforms.

3. Cloud and AI-based systems' adoption: Cloud adoption is becoming popular with lower IT infrastructure expense, flexibility, and remote access.

4. Compliance and data security: International and regional regulations are forcing hospitals to implement compliant, secure, and auditable systems.

Key Players:

- Epic dominates the hospital information system market with a 27.3% market share in 2024.

- Oracle is harnessing its purchase of Cerner's established HIS/EHR position together with its respective strengths in cloud computing, data analytics, and AI.

- Dedalus is a European market leader with a strong focus on interoperability and open digital health ecosystems.

Key Challenges:

- Interoperability constraints: HIS integration with legacy systems, labs, imaging, and third-party platforms continues to be challenging.

- High training and implementation expenses: Initial investments in customization, migration, and employee onboarding can be high.

- Security and data privacy threats: Increasing fears of health data breaches and ransomware are driving increased compliance and secure cloud deployments.

1. By System Component - Clinical Systems on the Rise

Clinical system components made up the largest share of the HIS market at approximately 66% in 2024. The clinical system components represented by EMR, CPOE, LIS, and RIS are the hard-working foundations of daily hospital operations.

2. By Deployment - Cloud-Based Solutions on the Rise

Cloud-based HIS deployability is accelerating due to the increased scalability, lower capital expenditures to support the infrastructure, and increased access to remote applications. The hospitals in the Regions are deploying cloud solutions to improve operations, collaboration, and continuum of care.

3. By Region - North America Remains Strong

North America continued to have the largest market share in 2024, maintaining their lead with strong government support, very high levels of digital literacy, and strong uptake in both public and private hospitals. North America maintains its dominance in the hospital information system market with strong healthcare infrastructure, prevalent adoption of EHR, government regulations like HIPAA and HITECH, and increasing presence of cloud-based health IT solutions. American hospitals and health networks are quickly integrating clinical decision support, population health analytics, and remote care modules into their core hospital systems.

Some of the major players in the hospital information system market are AGFA Healthcare, CAMBIO, ChipSoft, CompuGroup Medical, Dedalus, Docaposte, Engineering Ingegneria Informatica, Epic Systems, InterSystems, Meierhofer AG, NextGen, Nexus, Oracle, SECTRA, and Veradigm.

Key HIS players in the market are employing cloud integration, expansions into other geographies, AI-enabled modules, and collaboration agreements with healthcare leaders to create a competitive edge.;Epic Systems continues to lead the North American market with long-term deals with top-performing health systems. Dedalus and InterSystems are growing their cloud platforms and adding interoperability features. CompuGroup Medical and AGFA Healthcare are integrating decision support capabilities into their HIS platforms. Oracle is incorporating its integrated cloud and data analytics capabilities after acquiring Cerner to ultimately produce more valuable modules for EHR and population health.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 System component trends

- 2.2.3 Deployment trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of digital health solutions

- 3.2.1.2 Government initiatives and regulations

- 3.2.1.3 Rising expenditure on healthcare

- 3.2.1.4 Surging demand for integrated healthcare systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and maintenance costs

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing government healthcare digitization initiatives

- 3.2.3.2 Growing demand for analytics and business intelligence tools

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Consumer behaviour and trends

- 3.8 No. of hospitals, by Region

- 3.9 Overview of hospital digital ecosystem

- 3.9.1 Electronic medical records (EMR)/electronic health records (EHR)

- 3.9.2 Telemedicine and remote patient monitoring

- 3.9.3 Cybersecurity and data protection

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Integration of AI in EMR

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America & MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By System Component, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Clinical systems

- 5.2.1 Electronic medical records (EMR)/electronic health records (EHR)

- 5.2.2 Radiology information system (RIS)

- 5.2.3 Pharmacy information system

- 5.2.4 Laboratory information system (LIS)

- 5.2.5 Other clinical systems

- 5.3 Administrative/back-office systems

- 5.3.1 Finance and billing

- 5.3.2 Supply chain management

- 5.3.3 Facilities management/Human resources

- 5.4 Operational systems

- 5.4.1 Admission, discharge, and transfer (ADT)/bed management systems (BMS)

- 5.4.2 Operational standards support/scheduling systems

- 5.5 Patient-facing technologies

- 5.5.1 Mobile health applications

- 5.5.2 Patient portals

- 5.6 Integration layer

- 5.6.1 Interface engines/APIs

- 5.6.2 Health information exchange (HIE)

- 5.7 Data and security

- 5.7.1 Clinical data repository

- 5.7.2 Identity and access management (IAM)

- 5.7.3 General data protection regulation (GDPR)

Chapter 6 Market Estimates and Forecast, By Deployment, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 Web-based

- 6.4 On-premise

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AGFA Healthcare

- 8.2 CAMBIO

- 8.3 ChipSoft

- 8.4 CompuGroup Medical

- 8.5 Dedalus

- 8.6 Docaposte

- 8.7 Engineering Ingegneria Informatica

- 8.8 Epic Systems

- 8.9 InterSystems

- 8.10 Meierhofer AG

- 8.11 NextGen

- 8.12 Nexus

- 8.13 Oracle

- 8.14 SECTRA

- 8.15 Veradigm

醫院資訊系統市場按組件、類型、醫療機構規模、應用、部署模型和最終用戶分類 - 全球預測 2025-2030

醫院資訊系統市場按組件、類型、醫療機構規模、應用、部署模型和最終用戶分類 - 全球預測 2025-2030 高敏銳度資訊系統市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途、地區和競爭細分,2020-2030 年)

高敏銳度資訊系統市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用途、地區和競爭細分,2020-2030 年) 醫院資訊系統市場規模、佔有率、趨勢及預測(按組件、部署類型、系統類型、最終用戶和地區),2025 年至 2033 年

醫院資訊系統市場規模、佔有率、趨勢及預測(按組件、部署類型、系統類型、最終用戶和地區),2025 年至 2033 年 2025年全球綜合交付網路市場報告

2025年全球綜合交付網路市場報告 全球醫院資訊系統市場(至 2030 年)按組件(服務和軟體)、產品類型(EHR、CDSS、專業、診斷、藥房、品質、SCM、PHM、RCM、資料分析、遠端醫療)、部署(本地和雲端)和地區分類2025年全球先進資訊系統市場報告2025年全球醫院資訊系統市場報告

全球醫院資訊系統市場(至 2030 年)按組件(服務和軟體)、產品類型(EHR、CDSS、專業、診斷、藥房、品質、SCM、PHM、RCM、資料分析、遠端醫療)、部署(本地和雲端)和地區分類2025年全球先進資訊系統市場報告2025年全球醫院資訊系統市場報告 醫療認證系統市場按類型、應用程式、最終用戶、部署和地區分類醫院資訊系統市場:依類型、提供模式、組件和地區2025-2033 年按產品、應用、最終用戶和地區分類的高敏銳度資訊解決方案市場報告

醫療認證系統市場按類型、應用程式、最終用戶、部署和地區分類醫院資訊系統市場:依類型、提供模式、組件和地區2025-2033 年按產品、應用、最終用戶和地區分類的高敏銳度資訊解決方案市場報告