|

市場調查報告書

商品編碼

1667013

阻隔材料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Barrier Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

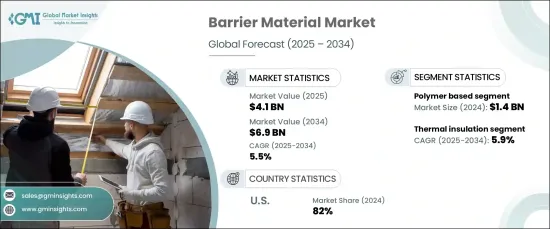

2024 年全球阻隔材料市場價值為 41 億美元,預計在 2025 年至 2034 年期間的複合年成長率為 5.5%。由於這些產業優先保護其產品和結構免受外部威脅,對阻隔材料的依賴持續上升。

阻隔材料對於防止濕氣侵入、熱波動和聲音滲透至關重要,對於提高各種應用的耐用性和效率至關重要。隨著監管機構對永續性的審查日益嚴格,企業正在轉向環保、可回收和高性能材料,以滿足現代行業標準。此外,技術進步和研發努力正在推動創新,提供滿足特定產業需求的尖端解決方案,最終擴大市場潛力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 41億美元 |

| 預測值 | 69億美元 |

| 複合年成長率 | 5.5% |

根據材料類型,市場分為金屬基、礦物基、聚合物基和其他類別。 2024 年聚合物基市場價值為 14 億美元,預計到 2035 年複合年成長率將達到 5.6%。 聚合物基材料以其卓越的防滲水能力而聞名,是屋頂、地下室和地基系統的首選,可解決人們日益成長的水損害問題。這些材料對於新建建築和改造工程來說已成為不可或缺的材料,能夠為抵禦環境因素提供可靠的保護。同時,金屬基材料在極端天氣條件下的環境中至關重要,例如沿海地區或容易受到高污染的工業區,使其成為結構彈性的重要組成部分。

依功能分類,市場包括防潮、隔熱、隔音、防火等部分。 2024 年,隔熱材料將佔據 41% 的市場佔有率,預計在預測期內的複合年成長率為 5.9%。不斷上升的能源成本和嚴格的能源效率法規增加了對先進熱障的需求。這些材料有助於減少熱量損失和最佳化能源消耗,特別是在加熱和冷卻系統中,符合全球對永續性和具有成本效益的能源解決方案的關注。

在美國,阻隔材料市場在 2024 年佔據了 82% 的區域佔有率。為滿足具有環保意識的消費者的需求,企業擴大採用可生物分解、低碳足跡的材料,包括可回收多層薄膜、生物聚合物基塑膠和可堆肥包裝。這一轉變體現了對環境管理的承諾,並使產業能夠按照永續發展目標繼續成長。

目錄

第 1 章:方法論與範圍

- 市場範圍和定義

- 基礎估算與計算

- 預測計算

- 資料來源

- 基本的

- 次要

- 付費來源

- 公共資源

第 2 章:執行摘要

第 3 章:產業洞察

- 產業生態系統分析

- 影響價值鏈的因素

- 利潤率分析

- 中斷

- 未來展望

- 製造商

- 經銷商

- 供應商概況

- 利潤率分析

- 重要新聞及舉措

- 監管格局

- 衝擊力

- 成長動力

- 增加建築活動

- 不斷成長的產品創新

- 產業陷阱與挑戰

- 市場飽和,競爭激烈

- 永續性問題

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL 分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 競爭定位矩陣

- 戰略展望矩陣

第 5 章:市場估計與預測:按材料,2021 年至 2035 年

- 主要趨勢

- 聚合物基

- 聚偏二氯乙烯(PVDC)

- 乙烯-乙烯醇 (EVOH)

- 聚萘二甲酸乙二醇酯(PEN)

- 其他

- 金屬基

- 礦物質

- 地工合成黏土襯墊 (GCL)

- 石膏

- 其他(礦物木等)

- 其他(纖維材料類等)

第 6 章:市場估計與預測:按功能,2021 年至 2035 年

- 主要趨勢

- 防潮

- 隔熱

- 隔音

- 防火

- 其他(輻射屏障、密封劑等)

第 7 章:市場估計與預測:按障礙類型,2021 年至 2035 年

- 主要趨勢

- 臨時屏障

- 永久性屏障

第 8 章:市場估計與預測:按建築類型,2021 年至 2035 年

- 主要趨勢

- 新建築

- 改造

第 9 章:市場估計與預測:依最終用途,2021-2035 年

- 主要趨勢

- 住宅

- 商業的

- 工業和倉儲

- 基礎設施設施

第 10 章:市場估計與預測:按配銷通路,2021-2035 年

- 主要趨勢

- 直接的

- 間接

第 11 章:市場估計與預測:按地區,2021 年至 2035 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中東及非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 12 章:公司簡介

- 3M

- BASF

- Dow

- Geosynthetics

- Gundle/SLT Environmental

- HB Fuller

- Honeywell International

- Owosso

- Pall Corporation

- Renolit

- Saint-Gobain

- Sika

- Solvay

- TenCate Geosynthetics

- Trelleborg

The Global Barrier Material Market was valued at USD 4.1 billion in 2024 and is poised to grow at a CAGR of 5.5% between 2025 and 2034. This upward trajectory is fueled by surging demand for advanced solutions that enhance safety and security across diverse industries such as construction, automotive, pharmaceuticals, and food packaging. As these sectors prioritize protecting their products and structures from external threats, the reliance on barrier materials continues to rise.

Barrier materials, essential for preventing moisture intrusion, thermal fluctuations, and sound penetration, are critical to improving the durability and efficiency of various applications. With increasing regulatory scrutiny on sustainability, businesses are transitioning toward eco-friendly, recyclable, and high-performance materials to meet modern industry standards. Moreover, technological advancements and R&D efforts are driving innovation, offering cutting-edge solutions tailored to meet specific industry needs, ultimately expanding the market's potential.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 5.5% |

By material type, the market is segmented into metal-based, mineral-based, polymer-based, and other categories. The polymer-based segment, valued at USD 1.4 billion in 2024, is expected to grow at a CAGR of 5.6% through 2035. Renowned for their superior ability to prevent water infiltration, polymer-based materials are the go-to choice for roofing, basement, and foundation systems, addressing the growing concerns about water damage. These materials have become indispensable for both new construction and renovation projects, offering reliable protection against environmental factors. Meanwhile, metal-based materials are vital in environments exposed to extreme weather conditions, such as coastal regions or industrial zones prone to high pollution, making them an essential component for structural resilience.

When categorized by function, the market includes moisture prevention, thermal insulation, soundproofing, fire protection, and other segments. Thermal insulation commanded a significant 41% market share in 2024 and is projected to grow at a 5.9% CAGR during the forecast period. Rising energy costs and stringent energy efficiency regulations have heightened the demand for advanced thermal barriers. These materials are instrumental in reducing heat loss and optimizing energy consumption, particularly in heating and cooling systems, aligning with the global focus on sustainability and cost-effective energy solutions.

In the United States, the barrier material market accounted for 82% of the regional share in 2024. This dominance is driven by robust regulatory frameworks aimed at reducing plastic waste and encouraging sustainable practices. Businesses are increasingly adopting biodegradable, low-carbon-footprint materials, including recyclable multi-layer films, biopolymer-based plastics, and compostable packaging, to cater to eco-conscious consumers. This shift reflects a commitment to environmental stewardship and positions the industry for continued growth in alignment with sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing construction activities

- 3.6.1.2 Growing product innovation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Market saturation and intense competition

- 3.6.2.2 Sustainability concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polymer based

- 5.2.1 Polyvinylidene chloride (PVDC)

- 5.2.2 Ethylene vinyl alcohol (EVOH)

- 5.2.3 Polyethylene naphthalate (PEN)

- 5.3 Others

- 5.4 Metal based

- 5.5 Mineral based

- 5.5.1 Geosynthetic clay liners (GCLs)

- 5.5.2 Gypsum

- 5.6 Others (mineral wood, etc.)

- 5.7 Others (fibrous material based, etc.)

Chapter 6 Market Estimates & Forecast, By Function, 2021-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Moisture prevention

- 6.3 Thermal insulation

- 6.4 Sound proofing

- 6.5 Fire protection

- 6.6 Others (radiation barrier, sealant, etc.)

Chapter 7 Market Estimates & Forecast, By Type of Barrier, 2021-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Temporary barriers

- 7.3 Permanent barriers

Chapter 8 Market Estimates & Forecast, By Type of Construction, 2021-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Retrofit

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial and warehousing

- 9.5 Infrastructure facility

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021-2035 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 BASF

- 12.3 Dow

- 12.4 Geosynthetics

- 12.5 Gundle/SLT Environmental

- 12.6 H.B. Fuller

- 12.7 Honeywell International

- 12.8 Owosso

- 12.9 Pall Corporation

- 12.10 Renolit

- 12.11 Saint-Gobain

- 12.12 Sika

- 12.13 Solvay

- 12.14 TenCate Geosynthetics

- 12.15 Trelleborg