|

市場調查報告書

商品編碼

1966916

全球防衛防衛防飛濺層(克維拉/玻璃纖維)市場:2026-2036Global Defense Spall Liners (Kevlar/Fiberglass) Market 2026-2036 |

||||||

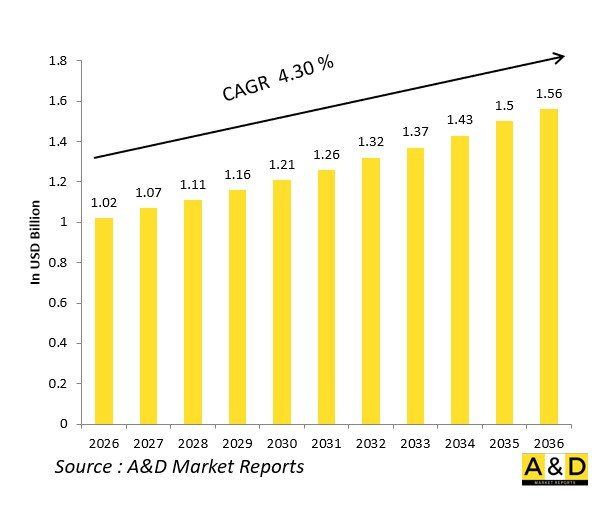

全球防衛防飛濺層(克維拉/玻璃纖維)市場預計將從2026年的10.2億美元成長到2036年的15.6億美元,2026年至2036年的年複合成長率(CAGR)為4.30%。

引言:全球防衛防飛濺層(克維拉/玻璃纖維)市場

全球防衛防飛濺層市場以克維拉和玻璃纖維材料為基礎,在以下方面發揮著非常重要的作用:提高裝甲平台和人員的生存能力。防衛防飛濺層安裝在裝甲車輛內部,用於吸收和阻擋砲彈撞擊外部裝甲產生的彈片,顯著增強乘員防護並減少戰鬥行動中的二次彈片損傷。對乘員生存能力、車輛安全標準和戰場韌性的日益重視,推動了先進防崩襯層解決方案的採用。克維拉爾和玻璃纖維因其高抗拉強度、能量吸收能力和輕量特性而廣泛應用。國防機構正日益將防衛防飛濺層整合到新車輛設計中,並將其納入現有車隊的升級計劃。鑑於現代戰場環境中車輛面臨的各種威脅,防衛防飛濺層已成為全球國防機構綜合裝甲防護系統的重要組成部分。

防衛防飛濺層(克維拉/玻璃纖維):技術影響

技術創新顯著提高了克維拉爾和玻璃纖維防衛防飛濺層的性能和可靠性。材料工程的進步提高了纖維強度、層壓技術和樹脂配方,增強了碎片防護能力和耐久性。先進的編織和黏合技術使防衛防飛濺層能夠在保持柔韌性的同時提供高抗衝擊性。電腦建模和彈道測試最佳化了襯墊的厚度和位置,在不增加過多重量的情況下提供最佳防護。為了平衡成本、性能和耐熱性,結合克維拉和玻璃纖維的混合襯墊設計正被日益採用。改進的阻燃塗層和環境耐受性提高了在惡劣工作環境下的安全性和使用壽命。製造技術的進步也使得精確定制能夠適應各種車輛內裝。這些技術發展使防衛防飛濺層能夠不斷發展,以滿足不斷變化的威脅情況和裝甲車輛的需求。

防衛防飛濺層(克維拉/玻璃纖維):關鍵驅動因素

幾個關鍵因素推動對克維拉和玻璃纖維材料製成的防衛防飛濺層的需求。對士兵和乘員安全的日益關注使得內部裝甲防護成為國防規劃者的優先事項。裝甲車輛面臨彈道威脅、地雷和簡易爆炸裝置(IED)的風險日益增加,進一步凸顯了對有效碎片防護解決方案的需求。裝甲車隊現代化和延壽計畫通常包括防衛防飛濺層升級。輕型裝甲解決方案是保持車輛機動性和燃油效率的首選。滿足更高的安全性和生存能力標準也促進了市場成長。此外,防衛防飛濺層維護需求相對較低且使用壽命長,使其成為經濟高效的投資。國防機構和材料製造商之間日益密切的合作進一步推動了技術創新和應用。這些因素共同維持了全球國防市場對克維拉和玻璃纖維防衛防飛濺層的強勁需求。

防衛防飛濺層(克維拉/玻璃纖維):區域趨勢

防衛防飛濺層市場的區域趨勢反映了不同的作戰需求和國防優先事項。北美地區強調將先進的乘員防護技術整合到下一代裝甲平台中。歐洲各國正致力於升級現有裝甲車輛,以滿足不斷變化的防護標準和盟國互通性需求。在亞太地區,由於國防能力的提升和車輛現代化計畫的推進,防衛防飛濺層的應用不斷成長。中東國防部隊由於其作戰中面臨高彈道和爆炸威脅,因此優先考慮防衛防飛濺層。新興國防市場正透過國際採購計畫和技術轉移協議逐步採用防衛防飛濺層。區域製造能力和政府對國內國防工業的支持會影響材料選擇和生產策略。總體而言,區域趨勢表明,全球正持續努力透過先進的防衛防飛濺層解決方案來增強車輛內部防護和生存能力。 本報告分析了全球防衛防飛濺層(克維拉/玻璃纖維)市場,提供了關鍵趨勢、市場影響因素、關鍵技術及其影響、主要地區和國家的趨勢以及市場機會分析。

目錄

全球防飛濺層(克維拉/玻璃纖維)市場:目錄

全球防飛濺層(克維拉/玻璃纖維)市場:報告定義

全球防飛濺層(克維拉/玻璃纖維)市場:市場區隔

依地區

依平台

依材料類型

依厚度

未來十年全球防飛濺層(克維拉/玻璃纖維)市場:市場分析

防飛濺層(克維拉/玻璃纖維)市場成長、趨勢變化、技術應用概要及市場吸引力詳情

防飛濺層(克維拉/玻璃纖維)市場:技術

預計將影響市場的十大技術及其對整體市場的潛在影響。

全球防衛防飛濺層(克維拉/玻璃纖維)市場:市場預測

報告詳細涵蓋了所有細分市場的十年市場預測。

全球防衛防飛濺層(克維拉/玻璃纖維)市場:區域趨勢與預測

本報告涵蓋市場趨勢、驅動因素、限制因素、挑戰以及政治、經濟、社會和技術因素。報告還提供了詳細的區域市場預測和情境分析。區域分析最後包括主要公司概況、供應商狀況和公司基準分析。目前市場規模是基於一切照舊情境估算的。

北美

驅動因素、限制因素與挑戰

PEST 分析

市場預測與情境分析

主要公司

供應商層級

公司標竿分析

歐洲

中東

亞太地區

南美洲

全球防衛防飛濺層(克維拉/玻璃纖維)市場:國家分析

美國

國防計畫

最新資訊

專利

該市場的當前技術成熟度

市場預測與情境分析分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

全球防衛防飛濺層(克維拉/玻璃纖維)市場:市場機會矩陣

專家對防衛防飛濺層(克維拉/玻璃纖維)市場報告的看法

結論

關於航空與國防市場報告

Global Defense Spall Liners (Kevlar/Fiberglass) Market

The Global Defense Spall Liners (Kevlar/Fiberglass) Market is estimated at USD 1.02 billion in 2026, projected to grow to USD 1.56 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.30% over the forecast period 2026-2036.

Introduction: Global Defense Spall Liners (Kevlar/Fiberglass) Market

The Global Defense Spall Liners Market, based on Kevlar and fiberglass materials, plays a vital role in enhancing the survivability of armored platforms and personnel. Spall liners are installed inside armored vehicles to absorb and contain fragments generated when projectiles impact external armor. By reducing secondary injuries caused by spall, these liners significantly improve crew protection during combat operations. Growing emphasis on crew survivability, vehicle safety standards, and battlefield resilience is driving the adoption of advanced spall liner solutions. Kevlar and fiberglass are widely preferred due to their high tensile strength, energy absorption capability, and lightweight characteristics. Defense forces are increasingly integrating spall liners into new vehicle designs as well as retrofit programs for existing fleets. As modern warfare environments expose vehicles to diverse threats, spall liners have become a critical component of comprehensive armor protection systems across global defense forces.

Technology Impact in Defense Spall Liners (Kevlar/Fiberglass)

Technological advancements have significantly improved the performance and reliability of defense spall liners made from Kevlar and fiberglass. Material engineering innovations have enhanced fiber strength, layering techniques, and resin formulations, resulting in better fragment containment and durability. Advanced weaving and bonding technologies allow spall liners to maintain flexibility while delivering high impact resistance. Computer-based modeling and ballistic testing have refined liner thickness and placement for optimal protection without adding excessive weight. Hybrid liner designs combining Kevlar and fiberglass are increasingly used to balance cost, performance, and thermal resistance. Improved fire-retardant coatings and environmental resistance features enhance safety and longevity in harsh operational conditions. Manufacturing advancements also enable precise customization to fit different vehicle interiors. These technological developments ensure that spall liners continue to evolve alongside changing threat profiles and armored vehicle requirements.

Key Drivers in Defense Spall Liners (Kevlar/Fiberglass)

Several key factors are driving demand for defense spall liners using Kevlar and fiberglass materials. Rising focus on soldier and crew safety has made internal armor protection a priority for defense planners. Increased exposure of armored vehicles to ballistic threats, mines, and improvised explosive devices has reinforced the need for effective spall mitigation solutions. Modernization and life-extension programs for armored fleets frequently include spall liner upgrades. Lightweight protection solutions are favored to maintain vehicle mobility and fuel efficiency. Compliance with enhanced safety and survivability standards also supports market growth. Additionally, the relatively low maintenance requirements and long service life of spall liners make them a cost-effective investment. Growing collaboration between defense organizations and material manufacturers further accelerates innovation and adoption. Together, these drivers sustain strong demand for Kevlar and fiberglass spall liners across global defense markets.

Regional Trends in Defense Spall Liners (Kevlar/Fiberglass)

Regional trends in the defense spall liners market reflect varying operational requirements and defense priorities. North America emphasizes advanced crew protection technologies integrated into next-generation armored platforms. European countries focus on upgrading existing armored vehicles to meet evolving protection standards and coalition interoperability needs. The Asia-Pacific region shows increasing adoption driven by expanding defense capabilities and vehicle modernization initiatives. Middle Eastern defense forces prioritize spall liners due to high operational exposure to ballistic and explosive threats. Emerging defense markets are gradually incorporating spall liners through international procurement programs and technology transfer agreements. Regional manufacturing capabilities and government support for domestic defense industries influence material selection and production strategies. Overall, regional trends indicate consistent global commitment to enhancing internal vehicle protection and improving survivability through advanced spall liner solutions.

Key Defense Spall Liners (Kevlar/Fiberglass) Program

Key defense spall liner programs focus on strengthening crew protection across a wide range of armored platforms. Vehicle upgrade initiatives commonly include the installation of Kevlar or fiberglass spall liners to improve survivability without altering external armor profiles. Defense ministries collaborate with specialized manufacturers to develop tailored liner solutions compatible with different vehicle interiors. Programs often emphasize modular designs for ease of installation, replacement, and maintenance. Research initiatives support the development of next-generation liner materials with improved energy absorption and reduced weight. Domestic production programs enhance supply chain security and enable faster deployment. Export-focused programs also contribute to the adoption of spall liner technologies among allied nations. Collectively, these programs underscore the strategic importance of internal armor protection as a core element of modern armored vehicle survivability strategies.

Table of Contents

Global Defense Spall Liners (Kevlar/Fiberglass) Market - Table of Contents

Global Defense Spall Liners (Kevlar/Fiberglass) Market Report Definition

Global Defense Spall Liners (Kevlar/Fiberglass) Market Segmentation

By Region

By Platform

By Material Type

By Thickness

Global Defense Spall Liners (Kevlar/Fiberglass) Market Analysis for next 10 Years

The 10-year Global Defense Spall Liners (Kevlar/Fiberglass) Market analysis would give a detailed overview of Global Defense Spall Liners (Kevlar/Fiberglass) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Defense Spall Liners (Kevlar/Fiberglass) Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Spall Liners (Kevlar/Fiberglass) Market Forecast

The 10-year Global Defense Spall Liners (Kevlar/Fiberglass) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global Defense Spall Liners (Kevlar/Fiberglass) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global Defense Spall Liners (Kevlar/Fiberglass) Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Defense Spall Liners (Kevlar/Fiberglass) Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Defense Spall Liners (Kevlar/Fiberglass) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Material Type, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Material Type, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Spall Liners (Kevlar/Fiberglass) Market Forecast, 2026-2036

- Figure 2: Global Defense Spall Liners (Kevlar/Fiberglass) Market Forecast, By Material Type, 2026-2036

- Figure 3: Global Defense Spall Liners (Kevlar/Fiberglass) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Spall Liners (Kevlar/Fiberglass) Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 9: South America, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 10: United States, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 11: United States, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 13: Canada, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 15: Italy, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 17: France, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 19: Germany, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 21: Netherlands, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 23: Belgium, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 25: Spain, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 27: Sweden, Defense Spall Liners (Kevlar/Fiberglass) Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 29: Brazil, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 31: Australia, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 33: India, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 35: China, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 39: South Korea, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 41: Japan, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 43: Malaysia, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 45: Singapore, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Spall Liners (Kevlar/Fiberglass) Market, Material Type Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Spall Liners (Kevlar/Fiberglass) Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By Material Type(Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By Material Type(CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Spall Liners (Kevlar/Fiberglass) Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Spall Liners (Kevlar/Fiberglass) Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Spall Liners (Kevlar/Fiberglass) Market, By Material Type, 2026-2036

- Figure 58: Scenario 1, Defense Spall Liners (Kevlar/Fiberglass) Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Spall Liners (Kevlar/Fiberglass) Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Spall Liners (Kevlar/Fiberglass) Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Spall Liners (Kevlar/Fiberglass) Market, By Material Type, 2026-2036

- Figure 62: Scenario 2, Defense Spall Liners (Kevlar/Fiberglass) Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Spall Liners (Kevlar/Fiberglass) Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Spall Liners (Kevlar/Fiberglass) Market, 2026-2036

防彈保護市場-2026-2032年全球市場預測

防彈保護市場-2026-2032年全球市場預測 彈道防護市場規模、佔有率和成長分析:按產品、材料、最終用戶、防護等級和地區分類-2026-2033年產業預測

彈道防護市場規模、佔有率和成長分析:按產品、材料、最終用戶、防護等級和地區分類-2026-2033年產業預測 2026年全球模組化防爆掩體市場報告2026年全球防彈保護市場報告2026年全球防彈防護工具市場報告

2026年全球模組化防爆掩體市場報告2026年全球防彈保護市場報告2026年全球防彈防護工具市場報告 全球防彈保護市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球防彈保護市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 防彈防護裝備市場規模、佔有率和趨勢分析報告:按產品類型、材料、最終用途、地區和細分市場分類,預測期為2026-2033年

防彈防護裝備市場規模、佔有率和趨勢分析報告:按產品類型、材料、最終用途、地區和細分市場分類,預測期為2026-2033年 彈道防護裝備市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、最終用戶、功能、安裝類型、設備

彈道防護裝備市場分析及預測(至2035年):類型、產品、服務、技術、應用、材質類型、最終用戶、功能、安裝類型、設備 全球均質軋製裝甲板 (RHA) 市場 (2026-2036)全球防務格柵/籠式裝甲市場:2026-2036

全球均質軋製裝甲板 (RHA) 市場 (2026-2036)全球防務格柵/籠式裝甲市場:2026-2036