|

市場調查報告書

商品編碼

1951131

全球國防拖曳陣列聲納市場:2026-2036Global Defense Towed Array Sonars Market 2026-2036 |

||||||

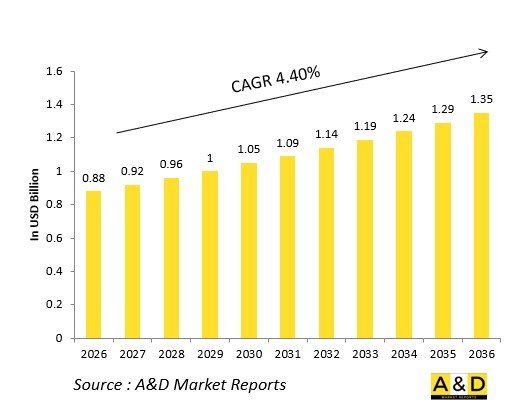

全球國防拖曳陣列聲納市場預計將從2026年的8.8億美元成長到2036年的13.5億美元,2026年至2036年的年複合成長率(CAGR)為4.40%。

引言:

受水下戰術日益複雜化以及反潛作戰戰略重要性不斷提升的推動,全球國防拖曳陣列聲納市場正經歷強勁成長。安裝在水面艦艇和潛水艇上的拖曳陣列聲納在遠程聲學探測、威脅追蹤和戰術態勢感知方面發揮著非常重要的作用。隨著海上強國不斷擴充其海軍艦隊,對彈性、高性能聲納系統的需求持續成長。數位訊號處理、光纖技術和低雜訊換能器陣列的進步顯著提高了偵測距離和可靠性。將這些系統與作戰管理網路整合,可以實現平台間的即時資料共享,強化網路化海軍作戰的概念。隨著各國將海上態勢感知和水下安全置於優先地位,在廣泛的國防現代化計劃以及對聲學情報和水下威懾日益重視的推動下,拖曳陣列聲納市場預計將穩步成長。

國防拖曳陣列聲納的技術影響

新興技術重塑國防拖曳陣列聲納系統的設計和功能。現代系統採用先進的水聽器陣列、數位波束成形和機器學習演算法來提高探測精度並減少誤報。光纖感測和改進的連接性實現了即時資料傳輸,並將訊號損耗降至最低,增強了深水和淺水區域的監視能力。小型化和模組化設計趨勢提高了部署靈活性,使其能夠整合到多種艦艇類型和無人水面航行器上。開放式架構框架的採用簡化了系統升級,並提高了與其他海軍感測器和聲學平台的互通性。降噪技術和自適應訊號濾波確保即使在高流量海域環境中也能保持穩定的性能。隨著國防機構大力推進多靜態分散式感測網路的建設,拖曳陣列聲納作為下一代海軍架構中核心水下態勢感知資產的作用日益凸顯。

國防拖曳陣列聲納的關鍵驅動因素

多項戰略和作戰因素推動全球拖曳陣列聲納市場的成長。潛艇數量的不斷增加和敵方海軍隱身能力的提升,使得能夠遠距離探測的先進系統變得非常重要。現代海軍戰術強調持續的水下監視和快速反應,這促使人們投資於高靈敏度的聲學陣列。水面艦艇和潛水艇的持續現代化也推動了拖曳式聲納技術的穩定應用。資料融合和網路中心戰戰術日益重要,推動了聲納陣列與作戰系統和自主水下航行器(AUV)的整合。此外,政府主導的促進國內感測器生產和技術轉移協議的舉措,也促使新興市場產業參與度不斷提高。對海上態勢感知能力的日益成長的需求,以及更安靜、性能更強的聲納設計的研發,預計將繼續推動全球海軍防禦戰略對拖曳式聲納解決方案的需求。

國防拖曳式聲納的區域趨勢

拖曳式聲納市場的區域趨勢反映了各地區防禦態勢、工業能力和海上挑戰的差異。在北美,先進的反潛作戰專案強調將拖曳式聲納感測器與水面艦艇和潛艦艦隊整合。在歐洲,目的是提高盟國海軍間聲學探測效率和模組化互通性的合作研究計畫蓬勃發展。隨著領土緊張局勢加劇和海軍現代化努力推進,亞太地區各國紛紛擴大水下監視網路,對拖曳陣列聲納的需求強勁。在中東,沿海和深海安全投資非常重要,並與全球系統供應商建立了合作夥伴關係。拉丁美洲和非洲等新興市場正透過對外援助和艦隊升級計畫逐步採用拖曳陣列聲納技術。在所有地區,對一體化水下防禦生態系統的關注持續影響著採購策略,凸顯了拖曳陣列系統在現代海上安全中發揮的關鍵作用。

本報告分析了全球國防拖曳陣列聲納市場,涵蓋關鍵趨勢、市場驅動因素、關鍵技術及其影響、主要地區和國家的市場趨勢以及市場機會分析。

目錄

國防拖曳陣列聲納市場:目錄

國防拖曳陣列聲納市場:報告定義

國防拖曳陣列聲納市場:細分

依地區

依平台

依部署方式

依陣列類型

未來十年國防拖曳陣列聲納市場分析

國防拖曳陣列聲納市場成長、趨勢變化、技術應用概述及市場吸引力詳情

國防拖曳陣列聲納市場:技術

預計將影響市場的十大技術及其對整體市場的潛在影響

全球國防拖曳陣列聲納市場:預測

以上各細分市場均涵蓋了未來十年的市場預測。

國防拖曳陣列聲納市場趨勢與預測:依地區劃分

本報告涵蓋市場趨勢、驅動因素、限制因素、挑戰以及政治、經濟、社會和技術因素。報告還提供了詳細的區域市場預測和情境分析。區域分析最後對主要公司、供應商格局和公司基準進行了概述。目前市場規模是基於通常情況估算的。

北美

驅動因素、限制因素與挑戰

PEST 分析

市場預測與情境分析

主要公司

供應商層級

公司標竿分析

歐洲

中東

亞太地區

南美洲

國防拖曳陣列聲納市場:國家分析

美國

國防計畫

最新資訊

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防拖曳陣列聲納市場:機會矩陣

國防拖曳陣列聲納市場報告的專家觀點

一般討論

關於航空和國防市場報告

The Global defense towed array sonar market is estimated at USD 0.88 billion in 2026, projected to grow to USD 1.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.40% over the forecast period 2026-2036.

Introduction:

The global defense towed array sonar market is experiencing strong momentum driven by the increasing complexity of undersea warfare and the strategic importance of anti-submarine operations. Towed array sonars, mounted on surface vessels and submarines, play a vital role in long-range acoustic detection, threat tracking, and tactical situational awareness. As maritime powers expand their naval fleets, the demand for flexible and high-performance sonar systems continues to rise. Advances in digital signal processing, fiber-optic technology, and low-noise transducer arrays have significantly enhanced detection ranges and reliability. Integration of these systems with combat management networks enables real-time data sharing across platforms, reinforcing the concept of networked naval operations. With nations prioritizing maritime domain awareness and underwater security, the towed array sonar market is set to expand steadily, supported by extensive defense modernization programs and increasing focus on acoustic intelligence collection and undersea deterrence.

Technology Impact in Defense Towed Array Sonars

Emerging technologies are reshaping the design and functionality of defense towed array sonar systems. Modern systems employ advanced hydrophone arrays, digital beamforming, and machine learning algorithms for enhanced detection precision and reduced false alarms. Fiber-optic sensing and improved connectivity allow real-time data transmission with minimal signal loss, strengthening surveillance capabilities in deep and shallow waters alike. Miniaturization and modular design trends have improved deployment flexibility, allowing integration across multiple ship classes and unmanned surface vessels. The adoption of open architecture frameworks simplifies system upgrades and enhances interoperability with other naval sensors and acoustic platforms. Noise reduction technologies and adaptive signal filtering enable sustained performance in high-traffic maritime environments. As defense organizations push for multi-static and distributed sensing networks, the role of towed array sonars as core underwater awareness assets continues to expand in next-generation naval architectures.

Key Drivers in Defense Towed Array Sonars

Several strategic and operational drivers are fueling growth in the global towed array sonar market. Rising submarine proliferation and the increasing stealth capabilities of adversarial navies necessitate advanced detection systems capable of operating across extended ranges. Modern naval doctrines emphasize persistent undersea surveillance and rapid response, encouraging investment in high-sensitivity acoustic arrays. Ongoing modernization of surface fleets and submarines also supports steady adoption of towed sonar technology. The growing importance of data fusion and network-centric warfare drives integration between sonar arrays, combat systems, and autonomous underwater vehicles. Additionally, government initiatives promoting indigenous sensor production and technology transfer agreements are expanding industrial participation across emerging markets. The increasing need for maritime domain awareness, combined with the development of quieter, more capable sonar designs, ensures continued demand for towed array solutions across global naval defense strategies.

Regional Trends in Defense Towed Array Sonars

Regional market patterns in towed array sonars reflect varying defense postures, industrial capabilities, and maritime challenges. In North America, advanced anti-submarine warfare programs emphasize integration of towed array sensors with surface ship and submarine fleets. Europe's focus lies in collaborative research projects aimed at enhancing acoustic detection efficiency and modular interoperability among allied naval forces. The Asia-Pacific region demonstrates strong demand as nations expand their undersea surveillance networks amid rising territorial tensions and naval modernization efforts. In the Middle East, investment centers on coastal and deep-water security, supported by partnerships with global system providers. Emerging markets in Latin America and Africa are gradually adopting towed sonar technologies through foreign assistance and fleet enhancement programs. Across all regions, the emphasis on integrated undersea defense ecosystems continues to shape procurement strategies, highlighting towed array systems as essential components of modern maritime security.

Key Defense Towed Array Sonars Programs

Key defense programs worldwide are advancing the design, production, and deployment of next-generation towed array sonar systems. Major naval forces and industry leaders are collaborating to develop long-range, high-sensitivity arrays integrated with combat management and anti-submarine warfare frameworks. Several upgrade initiatives focus on retrofitting existing vessels with digital processing modules, fiber-optic links, and enhanced hydrophone configurations to improve performance and maintain interoperability. International cooperative programs emphasize shared research and development to reduce costs and accelerate delivery timelines. Many emerging defense nations are pursuing indigenous sonar production capabilities through technology transfer agreements and local manufacturing partnerships. These programs collectively signify a global trend toward resilient, low-drag, and energy-efficient arrays optimized for both manned and unmanned naval platforms. The continuous evolution of these systems underscores their pivotal role in sustaining undersea dominance and maritime strategic deterrence.

Table of Contents

Defense Towed Array Sonars Market - Table of Contents

Defense Towed Array Sonars Market Report Definition

Defense Towed Array Sonars Market Segmentation

By Region

By Platform

By Deployment

By Array Type

Defense Towed Array Sonars Market Analysis for next 10 Years

The 10-year Defense Towed Array Sonars Market analysis would give a detailed overview of Defense Towed Array Sonars Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Towed Array Sonars Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Towed Array Sonars Market Forecast

The 10-year Defense Towed Array Sonars Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Towed Array Sonars Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Towed Array Sonars Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Towed Array Sonars Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Towed Array Sonars Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Array Type, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Array Type, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Towed Array Sonars Market Forecast, 2026-2036

- Figure 2: Global Defense Towed Array Sonars Market Forecast, By Array Type, 2026-2036

- Figure 3: Global Defense Towed Array Sonars Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Towed Array Sonars Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 9: South America, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 10: United States, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Towed Array Sonars Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Towed Array Sonars Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Towed Array Sonars Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Towed Array Sonars Market, By Array Type (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Towed Array Sonars Market, By Array Type (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Towed Array Sonars Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Towed Array Sonars Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Towed Array Sonars Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Towed Array Sonars Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Towed Array Sonars Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Towed Array Sonars Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Towed Array Sonars Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Towed Array Sonars Market, By Array Type, 2026-2036

- Figure 58: Scenario 1, Defense Towed Array Sonars Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Towed Array Sonars Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Towed Array Sonars Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Towed Array Sonars Market, By Array Type, 2026-2036

- Figure 62: Scenario 2, Defense Towed Array Sonars Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Towed Array Sonars Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Towed Array Sonars Market, 2026-2036