|

市場調查報告書

商品編碼

1936043

全球機載對抗系統市場:2026-2036Global Airborne Countermeasures System Market 2026-2036 |

||||||

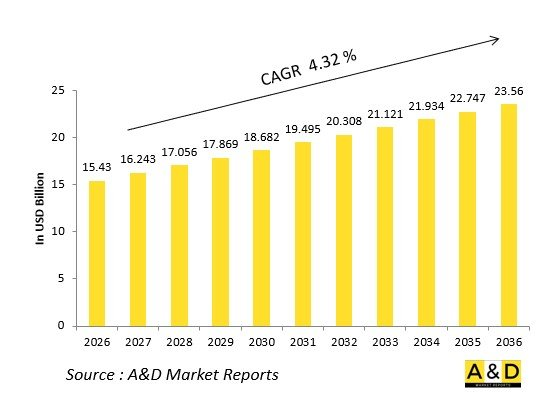

全球機載對抗系統市場預計將從2026年的154.3億美元成長到2036年的235.6億美元,2026年至2036年的複合年增長率(CAGR)為4.32%。

引言

全球機載對抗系統市場旨在保護固定翼和旋翼飛機免受不斷演變的飛彈威脅,將雷達警告接收機、飛彈逼近告警系統和對抗措施投放器整合到無縫的自衛系統中。這些系統能夠探測並識別紅外線、雷達和雷射導引武器,並使用箔條、幹擾彈和電子乾擾將其抵消。

市場成長反映了防空密度的不斷提高,因為系統正從被動式投放器發展到人工智慧驅動的定向效應器。核心組件包括吊艙式乾擾器、拖曳式誘餌和可編程投放器,這些設備可相容於從隱形戰鬥機到VIP專機的各種平台。強調減少附帶損害的城市作戰正在推動調製紅外線對抗措施的發展。

日益緊張的地緣政治局勢正在加速系統升級,並優先考慮聯盟任務中的互通性。開放式架構能夠快速更新威脅庫,而定向能武器的擴散正在推動供應鏈轉型為高可靠性電子設備。競爭日趨激烈,BAE系統公司和薩博公司等主要廠商正引領光纖拖曳陣列的研發。

該市場表明,飛機的生存能力是任務成功的關鍵。

科技對機載對抗系統的影響

技術融合將機載對抗系統轉變為主動防禦系統。多波長飛彈逼近警報系統(紫外線、紅外線和雷射)可偵測來自各個方向的飛彈發射,並透過基於全球交戰資料訓練的人工智慧威脅分類器,在微秒級時間內引導效應器。

定向紅外線對抗(DIRCM)雷射利用調製光束使導引系統失效,無需消耗品即可干擾先進的成像導引飛彈。光纖拖曳誘餌可模擬飛機特徵,同時能承受超音速發射,進而擴大干擾範圍。智慧投放器可根據光譜分析優化箔條和曳光彈的投放。

網路化架構支援整個編隊共享威脅數據,從而實現編隊級防禦。配備氮化鎵放大器的緊湊型乾擾器能夠承受集中乾擾。量子級聯雷射瞄準高光譜導引頭。數位射頻記憶體(DRFM)產生與真實發射器無法區分的虛假目標。

與AESA雷達整合可提供融合態勢感知。這些技術在飛行中部署帶有微型乾擾器的誘餌,可降低目標被解鎖的機率,擴大無逃逸區,並突破綜合防空系統。

機載對抗系統的關鍵驅動因素

便攜式防空飛彈系統(MANPADS)的擴散增加了對高價值飛機的威脅,因此需要多層防護。先進的成像飛彈可對抗傳統的干擾彈,推動空軍採用DIRCM(遠距離紅外線導引飛彈對抗)。

艦隊維護計畫優先考慮提高在衝突地區作戰的老舊運輸機和加油機的生存能力。出口市場需要能夠應付各種威脅庫的交鑰匙系統。

盟軍互通性標準正在加速通用架構的採用。城市地區的近距離空中支援理論要求使用能夠最大限度減少附帶損害的精確導引設備。定向能武器的擴散使得雷射警告接收器的普及勢在必行。

本報告對全球機載對抗系統市場進行了深入分析,全面闡述了關鍵趨勢、市場影響因素、關鍵技術及其影響、主要地區和國家的趨勢以及市場機會。

目錄

機載對抗系統市場:目錄

機載對抗系統市場:報告定義

機載對抗系統市場:細分

依應用

依地區

依類型

未來十年機載對抗系統市場分析

機載對抗系統市場成長、趨勢變化及技術詳情:應用概況及市場吸引力

機載對抗系統市場:技術

預計將影響市場的十大技術及其對整體市場的潛在影響

全球機載對抗系統市場: 預測

機載對抗系統市場趨勢及預測:依地區劃分

本報告涵蓋市場趨勢、驅動因素、限制因素、挑戰以及政治、經濟、社會和技術因素。報告還提供詳細的區域市場預測和情境分析。區域分析最後包括主要公司概況、供應商狀況和公司基準分析。目前市場規模是基於一切照舊情境估算的。

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測與情境分析

主要公司

供應商層級概覽

公司標竿分析

歐洲

中東

亞太地區

南美洲

機載對抗系統市場:國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

機載對抗系統市場:機會矩陣

機載對抗系統市場:專家意見

結論

關於航空與國防市場報告

The Global Airborne Countermeasures System Market is estimated at USD 15.43 billion in 2026, projected to grow to USD 23.56 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.32% over the forecast period 2026-2036.

Introduction

The global Airborne Countermeasures System market safeguards fixed-wing and rotary aircraft against evolving missile threats, integrating radar warning receivers, missile approach warners, and countermeasure dispensers into seamless self-protection suites. These systems detect, identify, and neutralize infrared, radar, and laser-guided munitions via chaff, flares, and electronic jamming.

Market growth mirrors rising air defense densities, with suites evolving from reactive dispensers to AI-driven directional effectors. Core components include podded jammers, towed decoys, and programmable dispensers compatible across platforms from stealth fighters to VIP transports. Emphasis on low-collateral urban ops drives modulated infrared countermeasures.

Geopolitical flashpoints accelerate retrofits, prioritizing interoperability for coalition missions. Open architectures enable rapid threat library updates. Supply chains focus on resilient electronics amid directed-energy proliferation. Competition features primes like BAE and Saab pioneering fiber-optic towed arrays.

This market underscores aircraft survivability as mission enabler.

Technology Impact in Airborne Countermeasures System

Technological fusion transforms Airborne Countermeasures Systems into proactive shields. Multi-spectral missile approach warners-UV, IR, and laser-based-detect launches from all quadrants, cueing effectors in microseconds via AI threat classifiers trained on global engagement data.

Directional Infrared Countermeasures (DIRCM) lasers dazzle seeker heads with modulated beams, defeating advanced imaging missiles without expendables. Fiber-optic towed decoys extend jamming envelopes, mimicking aircraft signatures while surviving supersonic ejections. Smart dispensers sequence chaff and flares optimally, minimizing signatures via spectral analysis.

Networked architectures share threat data across formations, enabling formation-wide defenses. GaN amplifiers power compact jammers resisting barrage jamming. Quantum cascade lasers target hyperspectral seekers. Digital radio frequency memory (DRFM) creates false targets indistinguishable from real emitters.

Integration with AESA radars provides fused situational awareness. Expendable decoys deploy micro-jammers mid-flight. These innovations slash break-lock probabilities, extend no-escape zones, and enable deep-strike penetrations against integrated air defenses.

Key Drivers in Airborne Countermeasures System

Proliferating man-portable air defense systems expose high-value aircraft to top-attack profiles, mandating layered countermeasures. Advanced imaging missiles counter legacy flares, driving DIRCM adoption across air forces.

Fleet sustainment programs prioritize survivability upgrades for legacy transports and tankers operating in contested zones. Export markets demand turnkey suites compatible with diverse threat libraries.

Coalition interoperability standards accelerate common architectures. Urban close air support doctrines require precision effectors minimizing collateral. Directed-energy weapon proliferation necessitates laser warning receivers.

Budget imperatives favor podded solutions over airframe redesigns. Training revolutions leverage virtual threat injectors. Supply chain resilience counters sanctions via diversified electronics.

Sustainability via reusable lasers reduces expendable logistics. These dynamics position countermeasures as airpower prerequisites.

Regional Trends in Airborne Countermeasures System

North America pioneers DIRCM suites for strategic airlift and fifth-generation fighters, emphasizing towed decoys.

Europe standardizes via NATO frameworks, equipping multirole fleets with fiber-optic jammers for eastern corridors.

Asia-Pacific surges with indigenous development-India's digital RWR, China's modular pods-for maritime patrols.

Middle East fortifies VIP transports against shoulder-fired threats.

Russia advances plasma-based decoys resilient to multimode seekers.

South Korea integrates with K9 howitzers' air cover.

Latin America protects counter-narcotics helos.

Trends favor AI-driven autonomy, Asia-Pacific gaining manufacturing share.

Key Airborne Countermeasures System Programs

AN/ALE-47 dispensers equip coalition fighters with adaptive sequencing against IR/RF threats.

Saab's CMDS integrates with Gripen for sequenced expendables.

BAE's DIRCM suites dazzle advanced seekers on C-130J.

AN/ALQ-214 podded jammers defend legacy platforms.

Next-gen fiber decoys tow behind F-35s.

European MBDA Talios fuses RWR with laser warning.

India's digital integrated RF suite upgrades Su-30MKI.

VIP aircraft receive commercial DIRCM variants.

Export packages bundle with missile warners.

Table of Contents

Airborne Countermeasures System Market - Table of Contents

Airborne Countermeasures System Market Report Definition

Airborne Countermeasures System Market Segmentation

By Application

By Region

By Type

Airborne Countermeasures System Market Analysis for next 10 Years

The 10-year Airborne Countermeasures System Market analysis would give a detailed overview of Airborne Countermeasures System Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Airborne Countermeasures System Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Airborne Countermeasures System Market Forecast

The 10-year Airborne Countermeasures System Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Airborne Countermeasures System Market Trends & Forecast

The regional Airborne Countermeasures System Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Airborne Countermeasures System Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Airborne Countermeasures System Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Airborne Countermeasures System Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Application , 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type , 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Application , 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type , 2026-2036

List of Figures

- Figure 1: Global Airborne Countermeasures System Market Forecast, 2026-2036

- Figure 2: Global Airborne Countermeasures System Market Forecast, By Region, 2026-2036

- Figure 3: Global Airborne Countermeasures System Market Forecast, By Application , 2026-2036

- Figure 4: Global Airborne Countermeasures System Market Forecast, By Type , 2026-2036

- Figure 5: North America, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 6: Europe, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 7: Middle East, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 8: APAC, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 9: South America, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 10: United States, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 11: United States, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 12: Canada, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 14: Italy, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 16: France, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 17: France, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 18: Germany, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 24: Spain, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 30: Australia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 32: India, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 33: India, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 34: China, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 35: China, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 40: Japan, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Airborne Countermeasures System Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Airborne Countermeasures System Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Airborne Countermeasures System Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Airborne Countermeasures System Market, By Application (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Airborne Countermeasures System Market, By Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Airborne Countermeasures System Market, By Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Airborne Countermeasures System Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Airborne Countermeasures System Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Airborne Countermeasures System Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Airborne Countermeasures System Market, By Region, 2026-2036

- Figure 58: Scenario 1, Airborne Countermeasures System Market, By Application , 2026-2036

- Figure 59: Scenario 1, Airborne Countermeasures System Market, By Type , 2026-2036

- Figure 60: Scenario 2, Airborne Countermeasures System Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Airborne Countermeasures System Market, By Region, 2026-2036

- Figure 62: Scenario 2, Airborne Countermeasures System Market, By Application , 2026-2036

- Figure 63: Scenario 2, Airborne Countermeasures System Market, By Type , 2026-2036

- Figure 64: Company Benchmark, Airborne Countermeasures System Market, 2026-2036

2026年全球固定翼無人機市場報告2026年全球小型無人機市場報告2026年全球燃油動力固定翼無人機市場報告

2026年全球固定翼無人機市場報告2026年全球小型無人機市場報告2026年全球燃油動力固定翼無人機市場報告 空中3D雷射掃描系統市場:依產品類型、掃描機制、最終用戶產業和應用分類,全球預測,2026-2032年GPS/INS市場:按技術、平台、分銷管道、應用和最終用戶分類,全球預測,2026-2032年智慧無人機機場市場:按組件、無人機類型、有效載荷能力、航程、技術、最終用戶和應用分類,全球預測(2026-2032年)無人機對接櫃市場:按連接方式、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

空中3D雷射掃描系統市場:依產品類型、掃描機制、最終用戶產業和應用分類,全球預測,2026-2032年GPS/INS市場:按技術、平台、分銷管道、應用和最終用戶分類,全球預測,2026-2032年智慧無人機機場市場:按組件、無人機類型、有效載荷能力、航程、技術、最終用戶和應用分類,全球預測(2026-2032年)無人機對接櫃市場:按連接方式、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 軍用航空雷射器市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、技術類型、平台類型、地區和競爭格局分類,2021-2031年隔音屏障市場按產品類型、材料、安裝方式、高度範圍和應用分類-全球預測,2026-2032年

軍用航空雷射器市場-全球產業規模、佔有率、趨勢、機會、預測:依產品類型、技術類型、平台類型、地區和競爭格局分類,2021-2031年隔音屏障市場按產品類型、材料、安裝方式、高度範圍和應用分類-全球預測,2026-2032年 機載雷射終端市場-全球及區域分析:按最終用戶、解決方案、組件、平台和地區分類-分析與預測(2025-2035)

機載雷射終端市場-全球及區域分析:按最終用戶、解決方案、組件、平台和地區分類-分析與預測(2025-2035)