|

市場調查報告書

商品編碼

1936040

全球 5G 國防市場:2026-2036年Global 5G in Defense Market 2026-2036 |

||||||

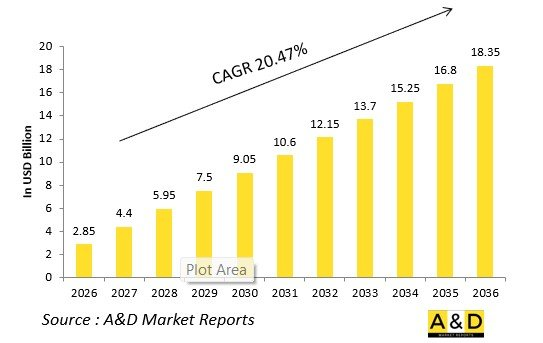

據估計,全球 5G 國防市場在2026年的價值為 28.5億美元,預計到2036年將達到 183.5億美元,2026年至2036年的年複合成長率(CAGR)為20.47%。

引言

全球 5G 國防市場可望徹底改變軍事通信,實現高頻寬、低延遲的通訊鏈路,這對於全局聯合行動非常重要。5G 可部署於空中、陸地和海上平台,支援情報、監視與偵察(ISR)、自主系統和分散式指揮節點的即時資料共享。其抗干擾能力是其優於傳統網路的關鍵所在。

隨著人工智慧、物聯網和邊緣運算的融合,市場發展動力加速,大規模 MIMO 技術可提高頻譜效率,波束成形技術可實現定向訊號傳輸。專用 5G 網路可保護戰術邊緣,而透過衛星進行的非地面擴展將覆蓋偏遠戰區。供應商軟體定義無線電和虛擬化技術方面展開合作,以促進敏捷部署。

地緣政治因素推動 5G 的普及,增強 C4ISR(指揮、控制、通訊、電腦、情報、監視與偵察)能力,以抵禦同儕威脅。互通性標準連接了民用和軍用頻譜。在網路風險日益嚴峻的背景下,供應鏈優先考慮穩健的硬體。競爭日趨激烈,Ericsson和泰雷茲等主要廠商在國防級核心技術領域處於領先地位。

5G 對國防領域的技術影響

5G 將對國防領域產生深遠影響,其延遲可降低至毫秒級,實現即時視訊串流、擴增實境疊加以及在逼真的作戰環境中遠端控制無人機。大規模 MIMO 技術顯著提升了吞吐量,而波束成形技術支援來自多個無人機和地面機器人的感測器融合,並可精確控制波束。

基地台邊緣運算可在本地處理 ISR 資料,最大限度地減少對雲端的依賴,並提高生存能力。網路切片技術可為關鍵任務流量分配頻寬,並將指揮和後勤流量分開。軟體定義網路(SDN)和網路功能虛擬化(NFV)技術可在運作期間實現動態重配置。

衛星回程鏈路將地面 5G 擴展到惡劣地形,並整合 NTN 以實現無處不在的覆蓋。人工智慧最佳化的頻譜共享利用認知無線電技術避免干擾。安全波形可抵禦電子戰攻擊,量子安全加密技術則保護資料鏈路。

擴增實境介面利用高頻寬實現沉浸式訓練和遠端維護。自主車隊可傳輸高解析度影片以進行車隊行動。這些能力透過縮短OODA循環、增強有人/無人協同以及使智慧倉庫能夠擴展物流,重新定義了戰術機動性。

國防領域5G的關鍵驅動因素

對全局聯合指揮的需求推動5G的普及,並需要跨軍種的無縫資料融合。無人機的擴散和自主性要求超視距控制具備超可靠的連接。

現代化計畫優先考慮能夠抵禦反電子戰的彈性網路。在壓力環境下,先進的防禦態勢加速前線基地私有 5G 的部署。從穿戴式裝置到武器,物聯網的普及對裝置處理能力提出了巨大的要求。

與商業生態系統的互通性使得透過商用現貨(COTS)硬體能夠節省成本。邊緣人工智慧的整合使得在戰術邊緣進行資料驅動的決策成為可能。頻譜拍賣強調在競爭性頻譜中進行動態分配。

網路安全需求推動了採用零信任架構的強化型 5G 核心網路的建置。由虛擬實境/擴增實境(VR/AR)模擬驅動的訓練革命充分利用了頻寬。透過盟國標準,出口潛力得以擴展。

預測性維護和自動補給等物流轉型依賴低延遲通訊。這些驅動因素將使 5G 成為 C4ISR(指揮、控制、通訊、電腦、情報、監視與偵察)的基礎。

國防領域的區域5G趨勢

北美在戰術5G領域處於領先地位,對聯合空中防禦指揮控制(JADC2)進行了大量投資,率先開發了MIMO測試環境和NTN整合。

歐洲正致力於透過部署SDN用於聯盟網路和海軍5G用於航空母艦作戰,來協調其北約框架。

在亞太地區,隨著印太地區競爭的加劇,5G技術取得了快速進展。中國推動用於島嶼防禦的自主5G,而印度則在推動核心網本地化。

在中東,波束成形ISR網路正用來加強基地防禦,以應對非對稱威脅。

俄羅斯開發用於前沿作戰的抗干擾波形。

印太盟國優先考慮衛星輔助5G技術,以增強海上態勢感知能力。

拉丁美洲開始反無人機網路試驗。非洲整合維和通訊。

混合地空架構正成為主流,預計亞洲將佔據相當大的市場佔有率。

國防項目中的關鍵5G技術

美國國防部的 "超越5G創新(IB5G)" 計畫與Nokia貝爾實驗室合作,率先在MHz至GHz頻段應用大規模MIMO技術,以提高戰術吞吐量。

JADC2計畫將5G整合到多域網路中,以實現即時火力支援。

"金色穹頂" 飛彈防禦系統利用5G進行預警和攔截。

海軍的5G到下一代(NextG)過渡演示強化艦載網路。

歐洲5G軍事網路將融合陸地、空中和海上領域。

印太演習測試無人機集群的波束成形技術。

私有5G基地將實現智慧後勤保障。

獵戶座計畫整合了5G和人工智慧技術,以實現邊緣情報、監視和偵察(ISR)。

戰術邊緣節點原型可在前線位置提供強大的5G網路。

這些計畫將為未來的作戰人員建構安全、可擴展的網路。

目錄

國防領域 5G 市場 - 目錄

國防領域 5G 市場 - 定義

國防市場區隔

依平台

依地區

按晶片組

未來十年國防領域 5G 市場分析

本章 詳細概述了國防領域 5G 市場的成長、發展趨勢、技術應用概況以及市場吸引力。

國防領域 5G 市場技術

本部分涵蓋了預計將影響該市場的十大技術及其對整體市場的潛在影響。

全球國防領域 5G 市場預測

以上各部分詳細涵蓋了國防領域 5G 市場未來十年的預測。

國防領域區域 5G 趨勢及預測

本部分涵蓋了區域 5G 市場趨勢、驅動因素、限制因素和挑戰,以及政治、經濟、社會和技術方面。此外,還提供了詳細的區域市場預測和情境分析。區域分析最後包括主要公司概況、供應商狀況和公司基準。目前市場規模是基於 "一切照舊" 情境估算的。

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測與情境分析

主要公司

供應商層級結構

公司標竿分析

歐洲

中東

亞太地區

南美洲

5G國防市場分析:依國家

本章涵蓋該市場的主要國防項目以及最新的新聞和專利申請。此外,本章也提供未來十年各國的市場預測和情境分析。

美國

國防項目

最新消息

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

南非

韓國

日本

馬來西亞

新加坡

巴西

5G國防市場機會矩陣

機會矩陣幫助讀者了解該市場中高機會的細分領域。

5G國防市場專家意見報告

本報告總結了專家對此市場潛力分析的意見。

結論

關於航空與國防市場報告

The Global 5G in Defense Market is estimated at USD 2.85 billion in 2026, projected to grow to USD 18.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 20.47% over the forecast period 2026-2036.

Introduction

The global 5G in defense market revolutionizes military communications, delivering high-bandwidth, low-latency links essential for joint all-domain operations. Deployed across airborne, land, and naval platforms, 5G supports real-time data sharing for ISR, autonomous systems, and distributed command nodes. Resilience against jamming defines its edge over legacy networks.

Market momentum builds on convergence with AI, IoT, and edge computing, enabling massive MIMO for spectrum efficiency and beamforming for directed signals. Private 5G networks secure tactical edges, while non-terrestrial extensions via satellites cover remote theaters. Vendors collaborate on software-defined radios and virtualization for agile deployments.

Geopolitical imperatives drive adoption, fortifying C4ISR against peer threats. Interoperability standards bridge commercial and military spectra. Supply chains prioritize hardened hardware amid cyber risks. Competition intensifies with primes like Ericsson and Thales pioneering defense-grade cores.

Technology Impact in 5G in Defense

5G profoundly impacts defense by slashing latencies to milliseconds, enabling real-time video feeds, AR overlays, and teleoperated drones in contested environments. Massive MIMO multiplies throughput, supporting sensor fusion from swarms of UAVs and ground robots via beamformed precision beams.

Edge computing at base stations processes ISR data locally, minimizing cloud dependency and enhancing survivability. Network slicing partitions bandwidth for mission-critical traffic, isolating command from logistics streams. Software-defined networking (SDN) and virtualization (NFV) allow dynamic reconfiguration mid-operation.

Satellite backhaul extends terrestrial 5G to austere zones, integrating NTNs for ubiquitous coverage. AI-optimized spectrum sharing evades jamming through cognitive radios. Secure waveforms resist electronic warfare, while quantum-safe encryption safeguards data links.

Augmented reality interfaces leverage high bandwidth for immersive training and remote maintenance. Autonomous convoys stream HD feeds for convoy ops. These capabilities compress OODA loops, empower manned-unmanned teaming, and scale logistics via smart warehouses, redefining tactical agility.

Key Drivers in 5G in Defense

Demand for joint all-domain command drives 5G adoption, requiring seamless data fusion across services. Proliferating drones and autonomy necessitate ultra-reliable connectivity for beyond-line-of-sight control.

Modernization programs prioritize resilient networks against peer electronic warfare. High defense postures amid tensions accelerate private 5G deployments for forward bases. IoT proliferation-from wearables to munitions-demands massive device handling.

Interoperability with commercial ecosystems cuts costs via COTS hardware. Edge AI integration enables data-driven decisions at the tactical edge. Spectrum auctions favor dynamic allocation for contested bands.

Cybersecurity mandates spur hardened 5G cores with zero-trust architectures. Training revolutions via VR/AR simulations leverage bandwidth. Export potentials expand through allied standards.

Logistics transformation-predictive maintenance, automated resupply-relies on low-latency links. These drivers embed 5G as C4ISR backbone.

Regional Trends in 5G in Defense

North America leads with massive investments in tactical 5G for JADC2, pioneering MIMO testbeds and NTN integrations.

Europe harmonizes via NATO frameworks, deploying SDN for coalition networks and naval 5G for carrier ops.

Asia-Pacific surges amid Indo-Pacific rivalries, with China advancing sovereign 5G for island defenses and India localizing cores.

Middle East fortifies bases with beamformed ISR nets against asymmetric threats.

Russia develops jamming-resistant waveforms for frontline use.

Indo-Pacific allies emphasize satellite-augmented 5G for maritime domain awareness.

Latin America pilots counter-drone networks. Africa integrates for peacekeeping comms.

Trends favor hybrid terrestrial-space architectures, with Asia capturing supply shares.

Key 5G in Defense Programs

DoD's Innovate Beyond 5G (IB5G) pioneers Massive MIMO from MHz to GHz, boosting tactical throughput with Nokia Bell Labs.

JADC2 initiatives weave 5G into multi-domain webs for real-time fires.

Golden Dome missile defense leverages 5G for alerts and intercepts.

Naval 5G-to-NextG demos harden shipboard networks.

European 5G military networks fuse land-air-sea slices.

Indo-Pacific exercises test beamforming for drone swarms.

Private 5G base camps enable smart logistics.

ORION program integrates 5G with AI for edge ISR.

Tactical Edge Node prototypes deliver resilient 5G at forward positions.

These programs forge secure, scalable nets for future warfighters.

Table of Contents

5G in Defense Market - Table of Contents

5G in Defense Market Report Definition

5G in Defense Market Segmentation

By Platform

By Region

By Chipset

5G in Defense Market Analysis for next 10 Years

The 10-year 5G in Defense Market analysis would give a detailed overview of 5G in Defense Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of 5G in Defense Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global 5G in Defense Market Forecast

The 10-year 5G in defense market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional 5G in Defense Market Trends & Forecast

The regional 5G in Defense Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of 5G in Defense Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for 5G in Defense Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on 5G in Defense Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type, 2026-2036

List of Figures

- Figure 1: Global 5G in Defense Market Forecast, 2026-2036

- Figure 2: Global 5G in Defense Market Forecast, By Region, 2026-2036

- Figure 3: Global 5G in Defense Market Forecast, By Platform, 2026-2036

- Figure 4: Global 5G in Defense Market Forecast, By Chipset, 2026-2036

- Figure 5: North America, 5G in Defense Market, Forecast, 2026-2036

- Figure 6: Europe, 5G in Defense Market, Forecast, 2026-2036

- Figure 7: Middle East, 5G in Defense Market, Forecast, 2026-2036

- Figure 8: APAC, 5G in Defense Market, Forecast, 2026-2036

- Figure 9: South America, 5G in Defense Market, Forecast, 2026-2036

- Figure 10: United States, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 11: United States, 5G in Defense Market, Forecast, 2026-2036

- Figure 12: Canada, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 13: Canada, 5G in Defense Market, Forecast, 2026-2036

- Figure 14: Italy, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 15: Italy, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 16: France, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 17: France, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 18: Germany, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 19: Germany, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 22: Belgium, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 24: Spain, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 25: Spain, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 26: Sweden, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 28: Brazil, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 30: Australia, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 31: Australia, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 32: India, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 33: India, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 34: China, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 35: China, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 38: South Korea, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 40: Japan, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 41: Japan, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 44: Singapore, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, 5G in Defense Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, 5G in Defense Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, 5G in Defense Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, 5G in Defense Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, 5G in Defense Market, By Platform (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, 5G in Defense Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, 5G in Defense Market, By Chipset (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, 5G in Defense Market, By Chipset (CAGR), 2026-2036

- Figure 54: Scenario Analysis, 5G in Defense Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, 5G in Defense Market, Global Market, 2026-2036

- Figure 56: Scenario 1, 5G in Defense Market, Total Market, 2026-2036

- Figure 57: Scenario 1, 5G in Defense Market, By Region, 2026-2036

- Figure 58: Scenario 1, 5G in Defense Market, By Platform, 2026-2036

- Figure 59: Scenario 1, 5G in Defense Market, By Chipset, 2026-2036

- Figure 60: Scenario 2, 5G in Defense Market, Total Market, 2026-2036

- Figure 61: Scenario 2, 5G in Defense Market, By Region, 2026-2036

- Figure 62: Scenario 2, 5G in Defense Market, By Platform, 2026-2036

- Figure 63: Scenario 2, 5G in Defense Market, By Chipset, 2026-2036

- Figure 64: Company Benchmark, 5G in Defense Market, 2026-2036

全球國防5G市場(至2035年):依通訊基礎設施類型、網路技術類型、晶片組類型、頻率類型、平台類型、地區、產業趨勢及預測分類

全球國防5G市場(至2035年):依通訊基礎設施類型、網路技術類型、晶片組類型、頻率類型、平台類型、地區、產業趨勢及預測分類 國防領域5G市場:2026-2032年全球市場預測(按組件、頻率、網路類型、部署環境、平台類型、頻率存取模式、技術、應用程式和最終用戶分類)

國防領域5G市場:2026-2032年全球市場預測(按組件、頻率、網路類型、部署環境、平台類型、頻率存取模式、技術、應用程式和最終用戶分類) 2026年全球5G國防市場報告

2026年全球5G國防市場報告 5G市場規模、佔有率、成長及全球國防產業分析:按類型、應用和地區分類的洞察,2026-2034年預測

5G市場規模、佔有率、成長及全球國防產業分析:按類型、應用和地區分類的洞察,2026-2034年預測 國防領域5G市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型及最終用戶分類全球5G市場規模、佔有率、趨勢和成長分析報告(國防領域,2026-2034)

國防領域5G市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、部署類型及最終用戶分類全球5G市場規模、佔有率、趨勢和成長分析報告(國防領域,2026-2034) 國防領域5G市場:全球產業規模、佔有率、趨勢、機會及預測(依通訊基礎設施、核心網路技術、網路類型、工作頻率、最終用途、區域和競爭格局分類),2021-2031年

國防領域5G市場:全球產業規模、佔有率、趨勢、機會及預測(依通訊基礎設施、核心網路技術、網路類型、工作頻率、最終用途、區域和競爭格局分類),2021-2031年 全球5G國防市場,2026-2030年

全球5G國防市場,2026-2030年 5G國防市場規模、佔有率和成長分析(按解決方案、平台、網路類型、工作頻率、部署類型、最終用戶和地區分類)-2026-2033年產業預測

5G國防市場規模、佔有率和成長分析(按解決方案、平台、網路類型、工作頻率、部署類型、最終用戶和地區分類)-2026-2033年產業預測