|

市場調查報告書

商品編碼

1927657

全球國防驅動系統市場(2026-2036)Global Defense Actuation System Market 2026-2036 |

||||||

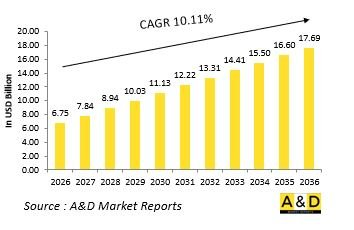

據估計,2026年全球國防驅動系統市場規模為67.5億美元,預計到2036年將達到176.9億美元,2026年至2036年的複合年增長率(CAGR)為10.11%。

全球國防驅動系統簡介

全球國防驅動系統能夠實現受控的機械運動,將電子或手動指令轉化為軍事平台上的實體運動。這些系統在關鍵任務功能中發揮核心作用,包括方向控制、力施加、穩定和關鍵子系統的定位。 其可靠性直接影響平台安全、操作精度和作戰連續性。在現代國防環境中,驅動系統必須在嚴苛的機械應力、惡劣的作戰環境和長時間的部署週期下持續穩定運作。它們支援感測器、控制軟體和機械組件之間的協調交互,確保即使在高速或高負載運行期間也能實現可預測的運行。隨著國防平台朝向整合化和自動化架構演進,驅動系統不再被設計為獨立的機械元件,而是成為精確控制的基礎。它們的作用多種多樣,包括飛機機動、船操舵、陸地車輛機動和武器瞄準。隨著國防平台日益複雜,驅動系統在戰略上的重要性也日益凸顯,成為提升現代軍事力量反應能力、生存能力和整體平台效能的關鍵組成部分。

科技對全球國防驅動系統的影響

技術發展重新定義了國防驅動系統的設計和部署方式。現代解決方案強調數位化指令接口,透過連續回饋控制實現精確的運動執行。 內建感測器的致動器可提供即時效能感知,使系統能夠動態適應不斷變化的運作負載。材料工程的進步支持緊湊型設計,可在減小結構體積的同時提供高力。電動執行器架構提高了效率,並簡化了與自動化控制系統的整合。執行器內建的診斷智慧支援基於狀態的維護,從而提高可用性並減少非計劃性停機時間。增強的訊號完整性和容錯能力提高了在電子乾擾環境下的可靠性。這些技術變革使執行器系統能夠作為智慧運動模組運行,從而提高複雜國防平台的協調性、精度和控制能力。

全球國防執行器系統的關鍵驅動因素

對先進國防執行器系統的需求受到多種作戰和戰略因素的驅動。平台現代化需要適用於數位化和自動化環境的運動控制解決方案。遠端操作和自主系統的日益普及增加了對無需人工直接幹預的可靠機械操作的依賴。國防機構還尋求透過減少維護負擔和延長維護週期來提高作戰準備。空中和陸地平台的重量優化工作正在推動緊湊型高性能執行器的應用。 對目標捕獲、導航和穩定精度的要求進一步加劇了對先進驅動解決方案的需求。此外,供應鏈安全的考量也推動了可靠且可本地維護的驅動技術的發展。總而言之,這些驅動因素表明,人們越來越關注性能可靠性、運作效率和系統韌性。

本報告分析了全球國防驅動系統市場,提供了影響該市場的技術資訊、未來十年的預測以及區域趨勢。

目錄

國防驅動系統市場報告定義

國防驅動系統市場區隔

按應用

按地區

按類型

未來十年國防驅動系統市場分析

國防驅動系統市場技術

全球國防驅動系統市場預測

區域國防驅動系統市場趨勢及預測

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測及情境分析

主要公司

供應商層級概覽

公司基準分析

歐洲

中東

亞太地區

南美洲

國防驅動系統市場概況及國家分析

美國

國防項目

最新資訊

專利

當前市場技術成熟度

市場預測及情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防驅動系統市場機會矩陣

國防驅動系統市場專家意見

結論

關於航空和國防市場報告

The Global Defense Actuation System market is estimated at USD 6.75 billion in 2026, projected to grow to USD 17.69 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 10.11% over the forecast period 2026-2036.

Introduction to Global Defense Actuation Systems

Global defense actuation systems enable controlled mechanical movement that translates electronic or manual commands into physical action across military platforms. These systems operate at the core of motion-critical functions, including directional control, force application, stabilization, and positioning of key subsystems. Their reliability directly influences platform safety, operational accuracy, and mission continuity. In contemporary defense environments, actuation systems must perform consistently under extreme mechanical stress, hostile operating conditions, and prolonged deployment cycles. They support coordinated interaction between sensors, control software, and mechanical assemblies, ensuring predictable behavior during high-speed or high-load operations. As defense platforms evolve toward integrated and automated architectures, actuation systems are increasingly designed as precision control enablers rather than standalone mechanical elements. Their role extends across aircraft maneuvering, naval steering, ground vehicle mobility, and weapon alignment. The growing complexity of defense platforms has elevated the strategic importance of actuation systems, positioning them as essential contributors to responsiveness, survivability, and overall platform effectiveness within modern military forces.

Technology Impact in Global Defense Actuation Systems

Technological development has redefined how defense actuation systems are designed and deployed. Modern solutions emphasize digital command interfaces, enabling precise execution of motion with continuous feedback control. Sensor-embedded actuators provide real-time performance awareness, allowing systems to adjust dynamically to changing operational loads. Advances in materials engineering support compact designs that deliver higher output while reducing structural mass. Electrically driven actuation architectures improve efficiency and simplify integration with automated control systems. Diagnostic intelligence embedded within actuators supports condition-based maintenance, improving availability and reducing unplanned downtime. Enhanced signal integrity and fault tolerance strengthen reliability in electronically challenged environments. These technological shifts allow actuation systems to function as intelligent motion modules that enhance coordination, accuracy, and control across complex defense platforms.

Key Drivers in Global Defense Actuation Systems

The demand for advanced defense actuation systems is driven by multiple operational and strategic factors. Platform modernization initiatives require motion control solutions compatible with digital and automated environments. Increased adoption of remotely operated and autonomous systems places greater reliance on dependable mechanical execution without direct human intervention. Defense organizations also seek improved mission readiness through reduced maintenance burden and longer service intervals. Weight optimization efforts across air and land platforms support adoption of compact, high-performance actuators. Precision requirements in targeting, navigation, and stabilization further reinforce the need for advanced actuation solutions. Additionally, supply security considerations encourage development of trusted and locally supported actuation technologies. These drivers collectively highlight the growing emphasis on performance reliability, operational efficiency, and system resilience.

Regional Trends in Global Defense Actuation Systems

Regional approaches to defense actuation systems reflect differences in platform focus, industrial capability, and operational doctrine. Aerospace-focused regions prioritize lightweight, high-precision actuation for flight control and stability. Naval-oriented regions emphasize resistance to corrosion and sustained performance in maritime conditions. Regions with extensive land force requirements focus on ruggedized solutions designed for shock tolerance and mobility support. Emerging defense markets increasingly adopt modular actuation systems that allow incremental upgrades and cross-platform compatibility. Regional investment in domestic manufacturing and technical partnerships influences system design and lifecycle strategies. These trends demonstrate how actuation systems are adapted to meet localized defense needs while aligning with global priorities for precision, durability, and integration.

Key Defense Defense Actuation System Program:

The Ministry of Defence entered into a contract with Hindustan Aeronautics Limited for the acquisition of 97 Light Combat Aircraft Mk1A for the Indian Air Force, comprising 68 single-seat fighters and 29 twin-seat variants, along with related equipment. Valued at more than ₹62,370 crore, excluding taxes, the agreement was signed on September 25, 2025. Deliveries are scheduled to begin in the 2027-28 timeframe and will be completed over a six-year period. The Mk1A aircraft will feature indigenous content exceeding 64 percent, with 67 additional systems and components incorporated beyond those included in the earlier LCA Mk1A contract signed. The integration of advanced domestically developed technologies, including the UTTAM Active Electronically Scanned Array radar, Swayam Raksha Kavach self-protection suite, and indigenous control surface actuators, will further reinforce India's Aatmanirbhar Bharat objectives in the defense aerospace sector.

Table of Contents

Defense Actuation Systems Market - Table of Contents

Defense Actuation Systems Market Report Definition

Defense Actuation Systems Market Segmentation

By Application

By Region

By Type

Defense Actuation Systems Market Analysis for next 10 Years

The 10-year Defense Actuation Systems Market analysis would give a detailed overview of Defense Actuation Systems Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Actuation Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Actuation Systems Market Forecast

The 10-year Defense Actuation Systems Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Actuation Systems Market Trends & Forecast

The regional Defense Actuation Systems Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Actuation Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Actuation Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Actuation Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Application, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type, 2026-2036

List of Figures

- Figure 1: Global Defense Actuation System Market Forecast, 2026-2036

- Figure 2: Global Defense Actuation System Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense Actuation System Market Forecast, By Application, 2026-2036

- Figure 4: Global Defense Actuation System Market Forecast, By Type, 2026-2036

- Figure 5: North America, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 6: Europe, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 8: APAC, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 9: South America, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 10: United States, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 12: Canada, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 14: Italy, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Actuation System Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Actuation System Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Actuation System Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Actuation System Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Actuation System Market, By Application (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Actuation System Market, By Application (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Actuation System Market, By Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Actuation System Market, By Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Actuation System Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Actuation System Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Actuation System Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Actuation System Market, By Region, 2026-2036

- Figure 58: Scenario 1, Defense Actuation System Market, By Application, 2026-2036

- Figure 59: Scenario 1, Defense Actuation System Market, By Type, 2026-2036

- Figure 60: Scenario 2, Defense Actuation System Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Actuation System Market, By Region, 2026-2036

- Figure 62: Scenario 2, Defense Actuation System Market, By Application, 2026-2036

- Figure 63: Scenario 2, Defense Actuation System Market, By Type, 2026-2036

- Figure 64: Company Benchmark, Defense Actuation System Market, 2026-2036

2026-2030年全球線性致動器市場

2026-2030年全球線性致動器市場 線性致動器市場:2026-2032年全球市場預測(按類型、工作模式、推力、行程長度、控制方式、安裝方式、應用和最終用途行業分類)

線性致動器市場:2026-2032年全球市場預測(按類型、工作模式、推力、行程長度、控制方式、安裝方式、應用和最終用途行業分類) 全球線性致動器市場規模、佔有率、趨勢和成長分析報告(2026-2034)電動線性致動器市場:按致動器類型、馬達類型、材質、安裝類型、等級、應用和銷售管道- 全球預測 2026-2032

全球線性致動器市場規模、佔有率、趨勢和成長分析報告(2026-2034)電動線性致動器市場:按致動器類型、馬達類型、材質、安裝類型、等級、應用和銷售管道- 全球預測 2026-2032 2026年全球液壓和電動線性致動器市場報告2026年全球線性致動器市場報告

2026年全球液壓和電動線性致動器市場報告2026年全球線性致動器市場報告 緊湊型電動線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)小型線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)電動線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

緊湊型電動線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)小型線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031年)電動線性致動器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)