|

市場調查報告書

商品編碼

1904995

全球國防線束市場(2026-2036)Global Defense Cables and Harness Market 2026-2036 |

||||||

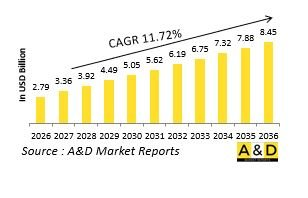

據估計,2026年全球國防線束市場規模為27.9億美元,預計到2036年將達到84.5億美元,2026年至2036年的複合年增長率(CAGR)為11.72%。

國防電纜線束市場簡介

全球國防電纜線束市場涵蓋用於在軍事平台上傳輸電力、數據和訊號的專用佈線系統,這些系統構成連接感測器、處理器、顯示器、控制器和執行器的神經系統。這些並非現成的電纜;它們是經過精心設計的系統,旨在承受軍事行動中遇到的極端溫度、振動、潮濕、化學物質、電磁幹擾和物理損傷。線束組件將數百根單獨的電線捆綁成受保護的結構,從而可以在狹小空間內有效地安裝和維護。其應用範圍涵蓋整個國防領域,從飛機和地面車輛到船艦和士兵系統。需求範圍從軍用級電力傳輸到感測器網路的高速資料鏈路。隨著平台電氣化和網路化程度的提高,電纜和線束系統的複雜性、密度和重要性也相應增加,使其成為國防能力中至關重要但又常被忽視的組成部分。

科技對國防電纜及線束市場的影響

國防電纜的技術進步著重於減輕重量、提高資料吞吐量和增強耐用性。光纖電纜正日益成為高頻寬資料傳輸的補充或替代銅線,同時也能抵抗電磁幹擾並減輕重量。先進的複合材料和奈米技術塗層在最大限度地減少品質的同時,也能增強電纜的保護性能。連接器設計正朝著更高密度、快速斷開和盲插功能的方向發展,從而便於在狹小空間內進行維護。無線平台內通訊雖然減少了部分佈線需求,但也帶來了安全性和可靠性的新挑戰。整合在電纜中的健康監測功能可在故障導致系統失效之前檢測到早期故障。機器人自動化線束製造提高了一致性,並縮短了複雜配置的生產時間。這些創新滿足了平台電氣系統對更高性能、更高可靠性和更低生命週期成本的相互衝突的需求。

國防電纜和線束市場的主要驅動因素

平台電氣化(從飛機電氣化到作戰車輛)的趨勢顯著增加了配電需求,並推動了高容量電纜系統的發展。現代平台上感測器和執行器的激增使數據傳輸需求呈指數級增長,對頻寬和電磁防護提出了更高的要求。所有行動平台對輕量化設計的需求推動了先進材料的應用以及線束佈線和配置的最佳化。對高效維護的需求推動了相關設計的發展,這些設計旨在簡化檢查、測試和更換流程,而無需對平台進行大規模拆卸。針對傳統平台的淘汰管理,持續需要複製已停產的電纜類型和連接器設計。此外,在惡劣環境下運行,例如沙漠的高溫或船舶的鹽霧環境,需要不斷改進防護材料和密封技術,以確保即使在極端條件下也能保持長期可靠性。

國防電纜與線束市場區域趨勢

區域電纜和線束產能通常與當地的平台製造能力和軍事工業生態系統密切相關。北美擁有大量專業供應商,這些供應商已融入主要承包商的供應鏈,為大型專案提供服務。歐洲的產業在航空航天應用領域尤其強大,跨國供應商同時服務民用和軍用飛機市場。在亞太地區,產能正在擴張,尤其是在那些擁有自主平台開發專案的國家,因為它們需要建立完整的供應鏈。以色列的產業在傳統系統升級和獨特平台配置等專業應用方面表現出色。中東國家越來越需要本地化的電纜系統維護和維修能力,以縮短平台週轉時間。全球標準化工作與專有技術相互競爭,平台類型和客戶偏好的差異導致不同地區和應用領域的採用模式各不相同。

本報告對全球國防線束市場進行研究和分析,提供影響該市場的技術資訊、未來十年的預測以及區域趨勢。

目錄

國防線束市場報告定義

國防線束市場區隔

按地區

按平台

按類型

未來十年國防線束市場分析

國防線束市場技術

全球國防線束市場預測

區域國防線束市場趨勢及預測

北美美洲

驅動因素、限制因素與挑戰

PEST分析

市場預測與情境分析

主要公司

供應商層級概覽

公司標竿分析

歐洲

中東

亞太地區

南美洲

國防電纜和線束市場趨勢和預測

北美

驅動因素、限制因素與挑戰

PEST分析

市場預測與情境分析

主要公司

供應商層級概覽

公司基準分析

歐洲

中東

亞太地區

南美洲市場國家分析

美國

國防項目

最新消息

專利

當前市場技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非洲

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防線束市場機會矩陣

專家對國防線束市場報告的意見

結論

關於航空和國防市場報告

The Global Defense Cables and Harness market is estimated at USD 2.79 billion in 2026, projected to grow to USD 8.45 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 11.72% over the forecast period 2026-2036.

Introduction to Defense Cables and Harness Market:

The Global Defense Cables and Harness Market encompasses the specialized wiring systems that transmit power, data, and signals throughout military platforms, forming the nervous system that connects sensors, processors, displays, controls, and effectors. These are not commercial cables but engineered systems designed to withstand extreme temperatures, vibration, moisture, chemicals, electromagnetic interference, and physical abuse encountered in military operations. Harness assemblies organize hundreds of individual wires into bundled, protected configurations that can be efficiently installed and maintained in confined spaces. Applications span all defense domains-from aircraft and ground vehicles to ships and soldier systems-with requirements varying from mil-spec power transmission to high-speed data links for sensor networks. As platforms become more electrified and networked, the complexity, density, and criticality of cable and harness systems increase correspondingly, making them essential yet often overlooked components of defense capability.

Technology Impact in Defense Cables and Harness Market:

Technological advancement in defense cabling focuses on weight reduction, data capability, and durability. Fiber optic cables increasingly supplement or replace copper for high-bandwidth data transmission while offering immunity to electromagnetic interference and reduced weight. Advanced composite materials and nanotechnology coatings enhance cable protection while minimizing mass. Connector designs evolve toward higher density, quick-disconnect, and blind-mate capabilities for easier maintenance in confined spaces. Wireless intra-platform communication reduces some cabling requirements but introduces new challenges in security and reliability. Integrated health monitoring capabilities within cables detect incipient faults before they cause system failures. Automated harness fabrication using robotics improves consistency and reduces production time for complex configurations. These innovations address the competing demands for higher performance, increased reliability, and reduced lifecycle costs in platform electrical systems.

Key Drivers in Defense Cables and Harness Market:

Platform electrification trends-from more electric aircraft to electric combat vehicles-substantially increase power distribution requirements, driving development of higher-capacity cabling systems. The proliferation of sensors and effectors on modern platforms creates exponential growth in data transmission needs, necessitating both higher bandwidth and more robust electromagnetic protection. Weight reduction imperatives across all mobile platforms favor advanced materials and optimization of harness routing and configuration. Maintenance efficiency requirements drive designs that facilitate easier inspection, testing, and replacement without extensive platform disassembly. Obsolescence management for legacy platforms creates sustained demand for reproduction of discontinued cable types and connector designs. Additionally, harsh environment operation-from desert heat to shipboard salt spray-mandates continuous improvement in protective materials and sealing technologies to ensure long-term reliability despite extreme conditions.

Regional Trends in Defense Cables and Harness Market:

Regional cable and harness capabilities often align with indigenous platform manufacturing capacity and military-industrial ecosystems. North America maintains extensive specialized suppliers integrated with prime contractor supply chains for major programs. European industry shows particular strength in aerospace applications, with multinational suppliers serving both civil and military aircraft markets. The Asia-Pacific region demonstrates growing capability, particularly in countries with developing indigenous platform programs that require complete supply chain development. Israeli industry excels in specialized applications for upgraded legacy systems and unique platform configurations. Middle Eastern nations increasingly seek localized maintenance and repair capabilities for cable systems to reduce turnaround times for platform servicing. Global standardization initiatives compete with proprietary approaches, with different platform types and customer preferences driving varied adoption patterns across regions and applications.

Key Defense Cables and Harness Program:

Reliance Defence & Engineering's June 2025 joint venture with U.S.-based Coastal Mechanics Inc. at MIHAN, Nagpur, secures MRO and upgrade contracts for land systems wiring harnesses and cables, starting with L-70 40mm air defense guns. The 10-year deal, worth multi-crore annually, modernizes electrical harnesses for reliability in harsh terrains, reducing downtime by 30%. It includes indigenous cable production using MIL-SPEC standards, integrating with Army's 100k+ vehicle fleet predictive maintenance AI pilots. This offsets import dependency, creates 500 jobs, and extends to BMP-II infantry vehicles. Phased rollout covers 500+ L-70 units by 2027, boosting layered air defense amid LAC tensions.

Table of Contents

Defense Cables and Harness Market Report Definition

Defense Cables and Harness Market Segmentation

By Region

By Platform

By Type

Defense Cables and Harness Market Analysis for next 10 Years

The 10-year defense cables and harness market analysis would give a detailed overview of defense cables and harness market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Cables and Harness Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Cables and Harness Market Forecast

The 10-year defense cables and harness market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Cables and Harness Market Trends & Forecast

The regional defense cables and harness market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Cables and Harness Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Cables and Harness Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Cables and Harness Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Platform, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Platform, 2025-2035

List of Figures

- Figure 1: Global Defense Cables and Harness Market Forecast, 2025-2035

- Figure 2: Global Defense Cables and Harness Market Forecast, By Region, 2025-2035

- Figure 3: Global Defense Cables and Harness Market Forecast, By Type, 2025-2035

- Figure 4: Global Defense Cables and Harness Market Forecast, By Platform, 2025-2035

- Figure 5: North America, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 9: South America, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 10: United States, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 16: France, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 17: France, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 20: Netherland, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 21: Netherland, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 32: India, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 33: India, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 34: China, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 35: China, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Cables and Harness Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Cables and Harness Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Cables and Harness Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Cables and Harness Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Cables and Harness Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Cables and Harness Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Cables and Harness Market, By Platform (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Cables and Harness Market, By Platform (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Cables and Harness Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Cables and Harness Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Cables and Harness Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Cables and Harness Market, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Cables and Harness Market, By Type, 2025-2035

- Figure 59: Scenario 1, Defense Cables and Harness Market, By Platform, 2025-2035

- Figure 60: Scenario 2, Defense Cables and Harness Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Cables and Harness Market, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Cables and Harness Market, By Type, 2025-2035

- Figure 63: Scenario 2, Defense Cables and Harness Market, By Platform, 2025-2035

- Figure 64: Company Benchmark, Defense Cables and Harness Market, 2025-2035

2026年全球有線電視及其他訂閱節目市場報告

2026年全球有線電視及其他訂閱節目市場報告 鎧裝電纜市場:依鎧裝類型、結構、電壓、材料、安裝和應用分類,全球預測(2026-2032)電氣接線端子市場:依電壓等級、材料類型、絕緣類型、產品類型、線規和最終用途產業分類,全球預測,2026-2032年高速電纜攝影機市場:按系統類型、電纜材料、控制技術、有效載荷能力、安裝方式和應用分類-全球預測,2026-2032年

鎧裝電纜市場:依鎧裝類型、結構、電壓、材料、安裝和應用分類,全球預測(2026-2032)電氣接線端子市場:依電壓等級、材料類型、絕緣類型、產品類型、線規和最終用途產業分類,全球預測,2026-2032年高速電纜攝影機市場:按系統類型、電纜材料、控制技術、有效載荷能力、安裝方式和應用分類-全球預測,2026-2032年 全球電力電纜產業(輸配電),2025-2035年

全球電力電纜產業(輸配電),2025-2035年 全球銅線電纜市場(至3032年)依絕緣類型、電壓類型、安裝方式(地下、架空、海底)、應用(建築用線、電力電纜、通訊、汽車線束)、終端用戶產業及地區分類

全球銅線電纜市場(至3032年)依絕緣類型、電壓類型、安裝方式(地下、架空、海底)、應用(建築用線、電力電纜、通訊、汽車線束)、終端用戶產業及地區分類 DVI連接器市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、設備、最終用戶、安裝類型及解決方案分類中東電纜市場分析及預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、安裝類型、組件、製程、功能高速電纜市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、設備、部署模式及最終用戶分類全球陶瓷電纜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

DVI連接器市場分析及預測(至2035年):依類型、產品、技術、組件、應用、材料類型、設備、最終用戶、安裝類型及解決方案分類中東電纜市場分析及預測(至2035年):類型、產品、技術、應用、材料類型、最終用戶、安裝類型、組件、製程、功能高速電纜市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、材質、設備、部署模式及最終用戶分類全球陶瓷電纜市場規模、佔有率、趨勢和成長分析報告(2026-2034年)