|

市場調查報告書

商品編碼

1838158

中口徑彈藥的全球市場(2025年~2035年)Global Medium Caliber Ammunition Market 2025-2035 |

||||||

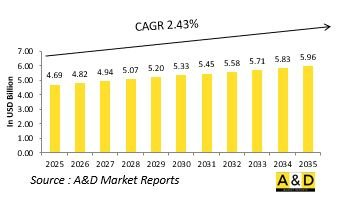

預計2025年全球中口徑彈藥市場規模將達到46.9億美元,到2035年將達到59.6億美元,2025年至2035年的複合年增長率為2.43%。

技術對中口徑彈藥市場的影響

技術創新正在改變國防中口徑彈藥市場,設計、材料和製造技術的進步提高了彈藥的性能、安全性和操作靈活性。現代彈藥採用智慧引信機制和可編程功能,讓操作員可以根據作戰需求選擇空爆、點撞擊和延遲引爆等起爆方式。這種適應性提高了對陸地和空中目標的打擊精度和有效性。輕質合金和複合材料殼體等先進材料的加入,在保持結構完整性和能源效率的同時,減輕了系統重量。精密工程和數位模擬工具能夠優化彈丸的空氣動力學和彈道性能,提高命中率並減少附帶損傷。自動化和積層製造也正在影響生產,使其能夠以更低的成本更快、更穩定地進行生產。彈藥管理系統與數位化火控架構的整合正在改善戰場後勤、可追溯性和即時態勢追蹤。此外,對環保推進劑和無毒底火的研究正在塑造下一代環境永續彈藥。這些技術進步正在重新定義作戰準備狀態,使現代軍隊能夠在多種作戰環境中以更高的效率、精度和戰術靈活性部署中口徑彈藥。

中口徑彈藥市場的關鍵驅動因素

國防中口徑彈藥市場的發展動力源自於對可靠、適應性強且有效火力的持續需求,以應對現代戰爭的挑戰。對裝甲車輛現代化、海上防禦和空對地攻擊能力的投資不斷增長,推動了對先進彈藥系統的持續需求。對精確瞄準和遠程作戰的重視推動了智慧可編程彈藥的發展,這與致力於最大限度地提高殺傷力並最大限度地減少附帶損害的國防戰略相一致。日益加劇的地緣政治緊張局勢、領土爭端以及維和行動的不斷擴大,不斷要求各國加強彈藥儲備。此外,常規威脅和非對稱威脅並存的混合戰爭的出現,凸顯了中口徑彈藥對於快速反應和持續作戰的重要性。國防組織也優先考慮互通性和標準化,以使多國部隊能夠在盟軍平台上無縫部署相容彈藥。另一個關鍵驅動因素是用旨在提高安全性、可靠性和惡劣條件下性能的新型彈藥替換老化的庫存彈藥。持續的研發投入以及國防工業和政府機構之間的合作確保了穩定的技術創新,使中口徑彈藥成為在不斷變化的全球國防形勢中取得戰術優勢的關鍵推動因素。

中口徑彈藥市場的區域趨勢

受軍事現代化優先事項、工業能力和安全環境的影響,國防中口徑彈藥市場的區域趨勢呈現出多樣化的模式。大型國防國家優先使用精確導引彈藥和可編程彈藥升級其現有的彈藥庫存,以保持其技術優勢。相較之下,發展中地區則優先考慮本地生產和具有成本效益的採購,以提高自力更生能力並減少對進口的依賴。沿海國家和島國正在投資海軍防禦彈藥以加強海上安全,而陸基國家則正在透過改進中口徑火力來增強其裝甲車和步兵的作戰能力。聯合防禦計劃和多邊訓練促進了盟軍使用標準化口徑和可互操作彈藥系統。這種協調一致有助於提高聯合行動中的後勤效率和作戰協調。此外,該地區的國防工業正在建立公私合作夥伴關係,以促進創新並維持長期供應鏈。新興市場的經濟成長和國防預算的增加進一步刺激了生產和出口潛力。同時,技術轉移協議和聯合發展策略使當地工業能夠獲得製造高品質彈藥的專業知識。總體而言,區域戰略體現了現代化、可用性和戰備狀態的平衡方法,確保中口徑彈藥在全球防禦態勢中仍然至關重要。

本報告研究並分析了全球中口徑彈藥市場,提供了成長動力、10 年展望以及區域市場趨勢和預測的資訊。

目錄

中口徑彈藥市場報告定義

中口徑彈藥市場區隔

按誘導

各類型

各地區

今後10年的中口徑彈藥市場分析

中口徑彈藥市場技術

全球中口徑彈藥市場

預測

中口徑彈藥的市場趨勢與預測:各地區

北美

促進因素,阻礙因素,課題

PEST

市場預測與Scenario分析

主要企業

供應商層級格局

企業基準

歐洲

中東

亞太地區

南美

中口徑彈藥市場國的分析

美國

防衛計劃

最新消息

專利

這個市場上目前技術成熟度

市場預測與Scenario分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

中口徑彈藥市場機會矩陣

中口徑彈藥市場報告相關專家的意見

結論

關於Aviation and Defense Market Reports

The Global Medium Caliber Ammunition market is estimated at USD 4.69 billion in 2025, projected to grow to USD 5.96 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 2.43% over the forecast period 2025-2035.

Introduction to Medium Caliber Ammunition Market:

The defense medium caliber ammunition market occupies a critical position within global military supply chains, supporting a wide array of platforms ranging from armored vehicles and naval guns to aircraft-mounted and infantry weapon systems. Medium caliber ammunition, typically used for automatic cannons and autocannons, bridges the gap between small arms and large artillery, providing armed forces with flexible firepower for both offensive and defensive operations. This segment is essential for modern warfare due to its effectiveness in countering lightly armored targets, suppressing enemy positions, and defending against aerial threats. The market continues to evolve as defense forces seek ammunition with improved range, precision, and lethality. Ongoing modernization of military fleets and the growing need for interoperability across land, naval, and air domains have elevated the strategic value of medium caliber munitions. Increasing focus on cost-effective yet technologically advanced solutions has encouraged manufacturers to enhance performance characteristics such as ballistic stability, penetration capability, and modularity. Moreover, the market benefits from the global trend of upgrading legacy platforms with next-generation weapon systems that rely heavily on refined ammunition standards. As militaries prepare for high-intensity combat and hybrid warfare scenarios, the demand for reliable, efficient, and adaptable medium caliber ammunition remains robust.

Technology Impact in Medium Caliber Ammunition Market:

Technological innovation is transforming the defense medium caliber ammunition market by advancing design, materials, and manufacturing techniques to improve performance, safety, and operational flexibility. Modern ammunition is being engineered with smart fusing mechanisms and programmable capabilities that allow operators to select detonation modes-such as airburst, point impact, or delayed explosion-depending on mission requirements. This adaptability enhances accuracy and effectiveness against both ground and aerial targets. Advanced materials, including lightweight alloys and composite casings, are being incorporated to reduce system weight while maintaining structural integrity and energy efficiency. Precision engineering and digital simulation tools now enable optimization of projectile aerodynamics and ballistic performance, resulting in higher hit probability and reduced collateral damage. Automation and additive manufacturing are also influencing production, allowing faster and more consistent output at lower costs. The integration of ammunition management systems into digital fire-control architectures is improving logistics, traceability, and real-time status tracking on the battlefield. Additionally, research in green propellants and non-toxic primers is shaping the next generation of environmentally sustainable ammunition. Collectively, these technological advancements are redefining operational readiness, ensuring that modern forces can deploy medium caliber ammunition with greater efficiency, precision, and tactical versatility across multiple combat environments.

Key Drivers in Medium Caliber Ammunition Market:

The defense medium caliber ammunition market is driven by the constant need for reliable, adaptable, and effective firepower to meet the challenges of modern warfare. Growing investments in armored vehicle modernization, naval defense, and air-to-ground strike capabilities have led to sustained demand for advanced ammunition systems. The emphasis on precision targeting and extended-range engagement has encouraged the development of smart and programmable ammunition, aligning with defense strategies focused on minimizing collateral damage while maximizing lethality. Rising geopolitical tensions, territorial disputes, and the expansion of peacekeeping operations continue to push nations to maintain robust ammunition stockpiles. Moreover, the emergence of hybrid warfare, where conventional and asymmetric threats coexist, underscores the importance of medium caliber rounds for both rapid-response and sustained operations. Defense agencies are also prioritizing interoperability and standardization, enabling multinational forces to deploy compatible munitions seamlessly across allied platforms. Another significant driver is the replacement of aging ammunition inventories with new variants designed for enhanced safety, reliability, and performance under extreme conditions. Continuous R&D investment and partnerships between defense industries and government agencies ensure steady innovation, positioning medium caliber ammunition as a vital enabler of tactical superiority in evolving global defense scenarios.

Regional Trends in Medium Caliber Ammunition Market:

Regional trends in the defense medium caliber ammunition market reveal diverse patterns influenced by military modernization priorities, industrial capacity, and security environments. Established defense powers emphasize upgrading existing ammunition inventories with precision-guided and programmable variants to maintain technological superiority. In contrast, developing regions are focusing on localized production and cost-efficient procurement to enhance self-reliance and reduce dependency on imports. Coastal and island nations are investing in naval defense ammunition to strengthen maritime security, while land-centric countries are expanding armored and infantry capabilities supported by improved medium caliber firepower. Collaborative defense programs and multinational training exercises are promoting the use of standardized calibers and interoperable ammunition systems across allied forces. This harmonization facilitates logistics efficiency and operational coordination during joint missions. Additionally, regional defense industries are fostering public-private partnerships to boost innovation and sustain long-term supply chains. Economic growth and increased defense budgets in emerging markets are further stimulating production and export potential. Meanwhile, technological transfer agreements and co-development initiatives are allowing local industries to gain expertise in manufacturing high-quality ammunition. Overall, regional strategies reflect a balanced approach between modernization, affordability, and operational readiness, ensuring that medium caliber ammunition remains integral to global defense preparedness.

Key Medium Caliber Ammunition Program:

MESKO S.A. and the Armament Agency have signed a contract to supply medium-caliber ammunition in 23X152 mm and 30X173 mm calibers to the Polish Armed Forces. Valued at nearly PLN 100 million, the agreement covers deliveries scheduled for 2024-2026 and was finalized on 7 September during the 31st International Defence Industry Exhibition (MSPO) in Kielce. This award continues MESKO's series of orders from the Polish Army for this ammunition type. The 23X152 mm rounds, equipped with BZT armor-piercing incendiary tracer projectiles, are intended for use in ZU-23-2 and ZSU-23-4 family anti-aircraft guns and their variants, as well as in the anti-aircraft components of ZUR-23-2 and ZSU-23-4MP systems. These cartridges are designed to engage low-flying aerial threats such as fixed-wing aircraft and helicopters, and to be effective against lightly armored ground and surface targets.

Table of Contents

Medium Caliber Ammunition Market Report Definition

Medium Caliber Ammunition Market Segmentation

By Guidance

By Type

By Region

Medium Caliber Ammunition Market Analysis for next 10 Years

The 10-year Medium Caliber Ammunition Market analysis would give a detailed overview of Medium Caliber Ammunition Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Medium Caliber Ammunition Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Medium Caliber Ammunition Market

Forecast

The 10-year Medium Caliber Ammunition Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Medium Caliber Ammunition Market Trends & Forecast

The regional Medium Caliber Ammunition Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Medium Caliber Ammunition Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Medium Caliber Ammunition Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Guidance, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Guidance, 2025-2035

List of Figures

- Figure 1: Global Medium Caliber Ammunition Market Forecast, 2025-2035

- Figure 2: Global Medium Caliber Ammunition Market Forecast, By Region, 2025-2035

- Figure 3: Global Medium Caliber Ammunition Market Forecast, By Type, 2025-2035

- Figure 4: Global Medium Caliber Ammunition Market Forecast, By Guidance, 2025-2035

- Figure 5: North America, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 6: Europe, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 8: APAC, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 9: South America, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 10: United States, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 11: United States, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 12: Canada, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 14: Italy, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 16: France, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 17: France, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 18: Germany, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 24: Spain, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 30: Australia, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 32: India, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 33: India, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 34: China, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 35: China, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 40: Japan, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Medium Caliber Ammunition Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Medium Caliber Ammunition Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Medium Caliber Ammunition Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Medium Caliber Ammunition Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Medium Caliber Ammunition Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Medium Caliber Ammunition Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Medium Caliber Ammunition Market, By Guidance (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Medium Caliber Ammunition Market, By Guidance (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Medium Caliber Ammunition Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Medium Caliber Ammunition Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Medium Caliber Ammunition Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Medium Caliber Ammunition Market, By Region, 2025-2035

- Figure 58: Scenario 1, Medium Caliber Ammunition Market, By Type, 2025-2035

- Figure 59: Scenario 1, Medium Caliber Ammunition Market, By Guidance, 2025-2035

- Figure 60: Scenario 2, Medium Caliber Ammunition Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Medium Caliber Ammunition Market, By Region, 2025-2035

- Figure 62: Scenario 2, Medium Caliber Ammunition Market, By Type, 2025-2035

- Figure 63: Scenario 2, Medium Caliber Ammunition Market, By Guidance, 2025-2035

- Figure 64: Company Benchmark, Medium Caliber Ammunition Market, 2025-2035

中口徑彈藥市場報告:趨勢、預測及競爭分析(至2035年)

中口徑彈藥市場報告:趨勢、預測及競爭分析(至2035年) 2026年30毫米近程反無人機彈藥全球市場報告2026年全球武器引信市場報告

2026年30毫米近程反無人機彈藥全球市場報告2026年全球武器引信市場報告 大口徑彈藥市場:按類型、口徑、材料、導引系統、終端用戶產業和分銷管道分類-2026年至2032年全球預測全球30毫米中口徑彈藥市場(2026-2036)

大口徑彈藥市場:按類型、口徑、材料、導引系統、終端用戶產業和分銷管道分類-2026年至2032年全球預測全球30毫米中口徑彈藥市場(2026-2036) 大口徑彈藥市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、材料類型、最終用戶和安裝類型分類

大口徑彈藥市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、材料類型、最終用戶和安裝類型分類 大口徑彈藥市場-全球產業規模、佔有率、趨勢、機會、預測:依口徑類型、最終用戶、地區和競爭格局分類,2021-2031年60-120毫米口徑彈藥市場:依彈頭類型、口徑範圍、應用、彈殼材質、發射藥類型和引信類型分類-2026-2032年全球預測中大口徑彈藥市場按彈藥類型、運載平台、推進方式、口徑類別、平台和最終用戶分類 - 全球預測(2026-2032 年)大口徑彈藥的全球市場:2025年~2035年

大口徑彈藥市場-全球產業規模、佔有率、趨勢、機會、預測:依口徑類型、最終用戶、地區和競爭格局分類,2021-2031年60-120毫米口徑彈藥市場:依彈頭類型、口徑範圍、應用、彈殼材質、發射藥類型和引信類型分類-2026-2032年全球預測中大口徑彈藥市場按彈藥類型、運載平台、推進方式、口徑類別、平台和最終用戶分類 - 全球預測(2026-2032 年)大口徑彈藥的全球市場:2025年~2035年