|

市場調查報告書

商品編碼

1811815

潛水艇的全球市場:2025年~2035年Global Submarine Market 2025 - 2035 |

||||||

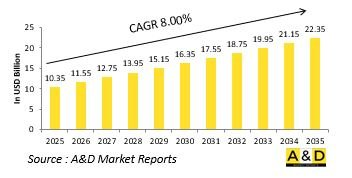

預計2025年全球潛艦市場規模將達到103.5億美元,到2035年預計將成長至223.5億美元,2025年至2035年的複合年增長率 (CAGR) 為8.00%。

潛水艇市場簡介

防禦性潛艦市場是海軍防禦中最具戰略意義的領域之一,因為潛艦為各國提供了無與倫比的隱身、威懾和力量投射能力。與水面艦隊不同,潛艇具有隱蔽性,能夠在不被發現的情況下執行偵察、情報收集和精確打擊任務。潛艇在現代海戰中的作用超越了傳統的戰鬥。保衛海上航線、維護海上邊界安全以及充當特種作戰平台也至關重要。潛艇市場正受到在地區和全球舞台上日益強調的水下優勢的影響。潛水艇,尤其是配備先進武器系統和長航時設計的潛水艇,具有重要的威懾作用。它們能夠長時間保持隱蔽,這為海軍在衝突和和平時期巡邏中提供了顯著優勢。許多海域的力量平衡日益取決於潛艦能力,促使各國透過先進的推進系統、消音技術和增強的生存能力來升級其艦隊。這反映了水下平台在保護國家安全和在爭議海域施加影響力方面的持久重要性。

科技對潛艦市場的影響

技術從根本上重新定義了潛艦在國防行動中的設計、性能和戰略重要性。推進系統的創新,尤其是不依賴空氣推進系統和核子技術的進步,顯著提高了潛艦的續航力和作戰範圍。這些發展使潛艇能夠更長時間地潛航,並增強了其隱身性能,使其更難被發現。消音技術是另一個關鍵的進步領域。潛艇擴大採用船體塗層、降噪推進器和減振系統來最大限度地降低其聲學特徵。這使得對手更難追蹤它們,從而增強了隱蔽潛艇在海戰中的作用。除了隱身之外,先進聲吶陣列和感測器套件的整合也顯著提高了態勢感知能力,使潛艇能夠保持隱蔽並在更遠的距離探測威脅。數位化和網路化能力也徹底改變了潛艦的作戰方式。現代平台建構了互聯互通的海底網絡,能夠與水面艦艇、飛機和指揮中心進行即時資訊交換。此外,遠程巡航導彈和魚雷等武器系統的進步正在擴大潛艇的進攻能力。無人水下航行器作為補充資產的應用進一步重塑了潛艇的作戰範圍,顯示技術如何不斷提升其作為海軍力量決定性工具的地位。

潛水艇市場的關鍵驅動因素

國防領域對潛艦的需求受到戰略需求、安全課題和技術機會的共同驅動。各國將潛艦視為確保海上優勢和保護與海上航線和近海資源相關的經濟利益的重要資產。潛水艇的隱身能力對於在競爭日益激烈的海上環境中進行威懾、力量投射和情報收集至關重要。地緣政治衝突和主要水道的領土爭端進一步加速了潛艇的需求。潛艇使海軍能夠監視敵方活動、維護海上利益,並在無需目視接觸的情況下投射力量,從而提供戰略優勢。隨著海上航線爭議地區緊張局勢加劇,對潛艦能力的投資成為國防規劃的核心。對現有艦隊進行現代化升級也是關鍵驅動因素。許多海軍強國正在逐步淘汰老舊平台,並以融合先進推進、隱身和武器技術的潛艇取而代之。此外,由於潛艦能夠同時執行常規和核威懾任務,其在國家安全戰略中的價值日益提升。除了衝突場景外,潛艦還參與非戰鬥任務,例如監視、研究和海底基礎設施保護,確保其在多個作戰領域中持續發揮重要作用。

潛水艇市場的區域趨勢

國防潛艦市場的區域動態受地區、安全環境和戰略重點的影響。擁有漫長海岸線和關鍵海上通道的海洋國家優先發展潛艦艦隊,以確保其領海安全,並向遠離海岸的地方投射力量。沿海防禦、反介入戰略以及對地區對手的威懾都推動著這些地區的潛艇採購。先進的海軍強國優先發展核潛艇,投資能夠長期部署和全球覆蓋的平台。這些艦艇是戰略威懾的關鍵,既支援常規作戰,也支援二次核打擊。相較之下,預算有限的地區往往更青睞配備最新推進和感測器技術的柴電潛艦,以平衡成本和作戰效能。地緣政治熱點,例如有爭議的海峽和有爭議的水域,進一步擴大了地區需求。部署潛艇是為了保持持續的水下存在,監視敵方動向,並確保對關鍵水道的控制。工業能力也會影響趨勢。一些國家優先考慮自主建造潛艇以提高自力更生的能力,而另一些國家則尋求透過合作和合資企業來獲取先進的平台。雖然這種地理多樣性引發了全球對潛艇的廣泛興趣,但每個細分市場都體現了與地區、資源和安全課題相關的獨特區域優先事項。

大型潛水艇計畫

馬札岡船塢造船公司已與德國蒂森克虜伯海洋系統公司(TKMS)就一項大型潛艦計畫展開正式合約談判。 TKMS已正式開始與印度採購部門的談判,這標誌著印度與德國在海軍領域的合作夥伴關係的開始。截至6月30日,TKMS的訂單儲備已達185億歐元,其中部分原因是正在進行的談判。雖然工程細節仍保密,但馬扎岡船塢的積極參與彰顯了印度海上國防工業的戰略重要性。該協議顯著增強了馬扎岡船塢的訂單儲備,並增強了其對印度海軍能力現代化的貢獻。

目錄

潛水艇市場報告定義

潛水艇市場區隔

各類型

各用途

各地區

未來10年潛艦市場分析

本章詳細概述了潛艦市場的成長、變化趨勢、技術採用概況和市場吸引力。

潛艦市場的市場技術

本部分討論了預計將影響該市場的十大技術,以及這些技術可能對整體市場產生的潛在影響。

全球潛艦市場預測

本報告對未來10年潛艦市場進行了詳細的預測,涵蓋了上述各個細分市場。

各地區潛艦市場趨勢及預測

本部分涵蓋各地區潛艦市場趨勢、驅動因素、限制因素、課題以及政治、經濟、社會和技術層面。此外,也提供詳細的區域市場預測和情境分析。最終的區域分析包括主要公司概況、供應商格局和公司基準分析。目前市場規模是基於常規情境進行估算。

北美

驅動因素、限制因素與課題

PEST(害蟲防治)

市場預測與情境分析

主要公司

供應商層級結構

公司基準測試

歐洲

中東

亞太地區

南美洲

潛水艇市場國家分析

本章涵蓋該市場的主要國防項目以及該市場的最新新聞和專利申請。本章也提供國家層級的10年市場預測和情境分析。

美國

國防計畫

最新消息

專利

該市場目前的技術成熟度

市場預測與情勢分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

潛水艇市場機會矩陣

機會矩陣幫助讀者了解該市場中高機會細分市場。

潛水艇市場報告方面的專家見解

針對該市場的潛在分析提供專家意見。

結論

關於調查公司

The Global Submarine market is estimated at USD 10.35 billion in 2025, projected to grow to USD 22.35 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 8.00% over the forecast period 2025-2035.

Introduction to Submarine Market:

The defense submarine market represents one of the most strategic areas within naval defense, as submarines provide nations with unmatched capabilities in stealth, deterrence, and force projection. Unlike surface fleets, submarines operate covertly, enabling them to conduct surveillance, intelligence gathering, and precision strike missions while remaining undetected. Their role in modern naval warfare extends beyond traditional combat; they are also crucial for protecting sea lanes, securing maritime borders, and serving as platforms for special operations. The market is shaped by the growing emphasis on undersea dominance in both regional and global theaters. Submarines serve as critical tools of deterrence, especially when equipped with advanced weapon systems and long-endurance designs. Their ability to remain hidden for extended periods gives naval forces a significant advantage, both in times of conflict and during peacetime patrols. The balance of power in many maritime regions is increasingly influenced by submarine capabilities, prompting nations to modernize fleets with advanced propulsion systems, acoustic quieting technologies, and enhanced survivability features. This makes the submarine market a central focus of naval procurement programs, reflecting the enduring importance of undersea platforms in safeguarding national security and projecting influence across contested waters.

Technology Impact in Submarine Market:

Technology has fundamentally redefined the design, performance, and strategic importance of submarines in defense operations. Innovations in propulsion systems, particularly air-independent propulsion and advancements in nuclear technology, have significantly extended the endurance and operational range of submarines. These developments allow vessels to remain submerged for longer durations, thereby enhancing stealth and reducing vulnerability to detection. Acoustic quieting technologies are another critical area of progress. Submarines are increasingly designed with hull coatings, noise-reducing propulsors, and vibration isolation systems that minimize their acoustic signature. This makes them more difficult for adversaries to track, bolstering their role as elusive assets in naval warfare. Alongside stealth, the integration of sophisticated sonar arrays and sensor suites has dramatically improved situational awareness, enabling submarines to detect threats at greater distances while remaining hidden themselves. Digitalization and network-enabled capabilities have also transformed submarine operations. Modern platforms can exchange real-time intelligence with surface ships, aircraft, and command centers, creating a connected undersea network. Additionally, advances in weapon systems, including long-range cruise missiles and torpedoes, have expanded the offensive potential of submarines. The adoption of unmanned underwater vehicles as complementary assets is further reshaping their operational scope, demonstrating how technology continues to elevate submarines as decisive instruments of naval power.

Key Drivers in Submarine Market:

The demand for submarines in the defense sector is propelled by a combination of strategic imperatives, security challenges, and technological opportunities. Nations view submarines as vital assets for ensuring maritime dominance and protecting economic interests tied to sea routes and offshore resources. Their ability to operate covertly makes them essential for deterrence, power projection, and intelligence gathering in an increasingly contested maritime environment. Geopolitical rivalries and territorial disputes over key waterways further accelerate demand. Submarines provide a strategic edge by allowing navies to monitor adversary activities, enforce maritime claims, and project force without the visibility of surface fleets. As tensions escalate in regions with contested sea lanes, investments in submarine capabilities become central to defense planning. The modernization of existing fleets is another significant driver. Many naval powers are phasing out older platforms and replacing them with submarines that incorporate advanced propulsion, stealth, and weapons technology. Additionally, the dual capability of submarines to conduct both conventional and nuclear deterrence roles enhances their value in national security strategies. Beyond conflict scenarios, submarines also contribute to non-combat missions such as surveillance, research, and undersea infrastructure protection, ensuring their continued relevance across multiple operational domains.

Regional Trends in Submarine Market:

Regional dynamics in the defense submarine market are shaped by geography, security environments, and strategic priorities. Maritime nations with expansive coastlines and access to vital sea lanes prioritize submarine fleets to secure territorial waters and project power far from their shores. Coastal defense, anti-access strategies, and deterrence against regional adversaries all drive submarine procurement in these areas. Advanced naval powers emphasize nuclear-powered submarines, investing in platforms capable of extended deployments and global reach. These vessels serve as cornerstones of strategic deterrence, supporting both conventional operations and second-strike nuclear capabilities. In contrast, regions with limited budgets often favor diesel-electric submarines equipped with modern propulsion and sensor technologies, balancing cost with operational effectiveness. Geopolitical hotspots such as contested straits and disputed maritime zones further amplify regional demand. Submarines are deployed to maintain a constant undersea presence, monitor adversary movements, and ensure control over vital waterways. Industrial capabilities also influence trends: some nations prioritize indigenous submarine construction to enhance self-reliance, while others pursue partnerships and joint ventures to acquire advanced platforms. This regional diversity ensures that while global interest in submarines is widespread, each market segment reflects localized priorities tied to geography, resources, and security challenges.

Key Submarine Program:

Mazagon Dock Shipbuilders has entered official contract discussions with Germany's ThyssenKrupp Marine Systems (TKMS) for a major submarine initiative. TKMS has formally opened negotiations with Indian procurement authorities, indicating an emerging Indo-German partnership in the naval sector. The company's order backlog reached EUR 18.50 billion as of June 30, with part of this attributed to the ongoing negotiations. Although detailed project specifics remain confidential, Mazagon Dock's active participation showcases its strategic importance within India's maritime defense industry. The agreement's outcome could substantially boost Mazagon Dock's order pipeline and enhance its contribution to the modernization of India's naval capabilities.

Table of Contents

Submarine Market Report Definition

Submarine Market Segmentation

By Type

By Application

By Region

Submarine Market Analysis for next 10 Years

The 10-year submarine market analysis would give a detailed overview of submarine market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Submarine Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Submarine Market Forecast

The 10-year submarine market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Submarine Market Trends & Forecast

The regional submarine market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Submarine Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Submarine Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Submarine Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Submarine Market Forecast, 2025-2035

- Figure 2: Global Submarine Market Forecast, By Region, 2025-2035

- Figure 3: Global Submarine Market Forecast, By Type, 2025-2035

- Figure 4: Global Submarine Market Forecast, By Application, 2025-2035

- Figure 5: North America, Submarine Market, Market Forecast, 2025-2035

- Figure 6: Europe, Submarine Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Submarine Market, Market Forecast, 2025-2035

- Figure 8: APAC, Submarine Market, Market Forecast, 2025-2035

- Figure 9: South America, Submarine Market, Market Forecast, 2025-2035

- Figure 10: United States, Submarine Market, Technology Maturation, 2025-2035

- Figure 11: United States, Submarine Market, Market Forecast, 2025-2035

- Figure 12: Canada, Submarine Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Submarine Market, Market Forecast, 2025-2035

- Figure 14: Italy, Submarine Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Submarine Market, Market Forecast, 2025-2035

- Figure 16: France, Submarine Market, Technology Maturation, 2025-2035

- Figure 17: France, Submarine Market, Market Forecast, 2025-2035

- Figure 18: Germany, Submarine Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Submarine Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Submarine Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Submarine Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Submarine Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Submarine Market, Market Forecast, 2025-2035

- Figure 24: Spain, Submarine Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Submarine Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Submarine Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Submarine Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Submarine Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Submarine Market, Market Forecast, 2025-2035

- Figure 30: Australia, Submarine Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Submarine Market, Market Forecast, 2025-2035

- Figure 32: India, Submarine Market, Technology Maturation, 2025-2035

- Figure 33: India, Submarine Market, Market Forecast, 2025-2035

- Figure 34: China, Submarine Market, Technology Maturation, 2025-2035

- Figure 35: China, Submarine Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Submarine Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Submarine Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Submarine Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Submarine Market, Market Forecast, 2025-2035

- Figure 40: Japan, Submarine Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Submarine Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Submarine Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Submarine Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Submarine Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Submarine Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Submarine Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Submarine Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Submarine Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Submarine Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Submarine Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Submarine Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Submarine Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Submarine Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Submarine Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Submarine Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Submarine Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Submarine Market, By Region, 2025-2035

- Figure 58: Scenario 1, Submarine Market, By Type, 2025-2035

- Figure 59: Scenario 1, Submarine Market, By Application, 2025-2035

- Figure 60: Scenario 2, Submarine Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Submarine Market, By Region, 2025-2035

- Figure 62: Scenario 2, Submarine Market, By Type, 2025-2035

- Figure 63: Scenario 2, Submarine Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Submarine Market, 2025-2035

2026年全球潛艦作戰系統市場報告2026年全球潛艦市場報告

2026年全球潛艦作戰系統市場報告2026年全球潛艦市場報告 潛艦設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年2026-2034年全球潛艦作戰系統市場規模、佔有率、趨勢及成長分析報告

潛艦設備市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類,並預測至2026-2034年2026-2034年全球潛艦作戰系統市場規模、佔有率、趨勢及成長分析報告 潛艦作戰系統市場-全球產業規模、佔有率、趨勢、機會及預測(依潛艦類型、武器系統、地區及競爭格局分類,2021-2031年)潛艦市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、平台類型、地區和競爭格局分類,2021-2031年

潛艦作戰系統市場-全球產業規模、佔有率、趨勢、機會及預測(依潛艦類型、武器系統、地區及競爭格局分類,2021-2031年)潛艦市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、平台類型、地區和競爭格局分類,2021-2031年 潛水艇模擬市場:全球(2025-2035)

潛水艇模擬市場:全球(2025-2035) 潛艦作戰系統市場規模、佔有率、成長分析(按系統、潛艦類型、按地區)-2025-2032 年產業預測潛水艇救援系統市場:全球2025-2035年

潛艦作戰系統市場規模、佔有率、成長分析(按系統、潛艦類型、按地區)-2025-2032 年產業預測潛水艇救援系統市場:全球2025-2035年 2024年至2032年潛艦作戰系統市場機會、成長動力、產業趨勢分析與預測

2024年至2032年潛艦作戰系統市場機會、成長動力、產業趨勢分析與預測