|

市場調查報告書

商品編碼

1744375

魚雷的全球市場:2025年~2035年Global Torpedo Market 2025-2035 |

||||||

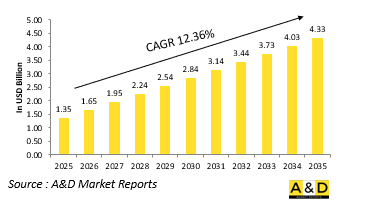

2025年全球魚雷市場規模估計為13.5億美元,預計到2035年將成長至43.3億美元,2025年至2035年的複合年增長率 (CAGR) 為12.36%。

魚雷市場簡介:

魚雷是潛水艇、水面艦艇和飛機用來打擊和化解海上威脅的重要水下武器。這些自航式彈藥旨在透過直接撞擊或近距離引爆來追蹤和摧毀敵方潛艇和水面艦艇。與水雷和深水炸彈不同,魚雷可以使用機載導引系統主動搜尋目標,使其在海上攻防行動中非常有效。它們的應用範圍涵蓋和平時期的威懾、戰時打擊任務和反逼近戰略。隨著海域爭奪日益激烈,魚雷憑藉其隱身、突襲和殺傷力,在水下戰爭中發揮核心作用。現代海軍戰術越來越依賴這種武器來保持水下優勢和戰略威懾,尤其是在喉嚨要道和領海。魚雷可搭載於從柴電潛艦到遠程巡邏機等各種平台,構成海軍力量的重要組成部分。魚雷在保障海上交通線安全以及阻止敵方海軍水面入侵方面也發揮關鍵作用。全球防衛界持續優先發展魚雷,並認識到魚雷在非對稱和高強度衝突場景中的持久價值。魚雷的持續發展反映了向水下優勢和綜合海上戰備的廣泛轉變。

科技對魚雷市場的影響:

技術進步顯著改變了現代魚雷在海上防禦中的能力和作用。推進系統的創新使魚雷更安靜、更快,降低了被發現的風險,同時提高了攻擊精準度。熱力發動機、先進的電動馬達和改進的流體動力學使這些武器能夠在更遠的距離上作戰,並具有更高的隱身性。在導引方面,新型魚雷整合了先進的聲吶、尾流自導感測器和慣性導航系統,使其能夠適應複雜的環境並超越對抗措施。人工智慧和自主瞄準演算法也在不斷湧現,使魚雷能夠以最少的操作員輸入區分誘餌和真實威脅。增強的資料鏈功能允許在發射後進行中途更新,使操作員的控制更加靈活。彈頭設計不斷發展,旨在保持緊湊性和安全性的同時,提供更集中、更有效的殺傷力。此外,模組化架構允許快速升級和針對特定任務的配置。這些技術進步不僅提高了殺傷力,也提高了在日益複雜的反潛戰系統中的生存能力。現代魚雷已融入網路中心海軍作戰,如今在高度競爭的水下環境中既是戰略威懾力量,又是精確打擊武器,為常規和非對稱海上戰區的任務成功提供支援。

魚雷市場的關鍵推動因素:

幾個關鍵因素正在推動現代海軍戰略中魚雷的全球研發和部署。隨著各國尋求確保戰略水道和海洋資源的安全,對水下領域主導地位的競爭日益激烈,這也扮演著重要角色。潛艦在監視和威懾方面的活動日益增多,凸顯了對有效水下攻擊方案的需求。海軍理論的演變優先考慮分層防禦和快速反應能力,這增強了魚雷在攻防態勢中的相關性。無人平台的整合和近海作戰的擴展需要能夠在淺水和狹窄水域中作業的緊湊、高效的魚雷。對區域熱點地區反潛威脅的擔憂推動了對用於對抗各種潛艇和水面對手的魚雷的進一步投資。此外,對遠洋作戰力量投射的重視也刺激了遠程和多用途魚雷的研發。現代海軍也重視自力更生,促使各國加強了自主魚雷設計與生產的研究。戰備狀態和靈活的部署選項仍然是關鍵目標,這促使人們增強發射系統和儲存能力。這些推動因素反映了一種戰略轉變,即在日益激烈的全球安全環境中保持可靠的威懾力,改善海上戰術選擇,並確保海上優勢。

魚雷市場區域趨勢:

魚雷的研發和部署因地區而異,並受其獨特的海洋戰略和威脅認知所影響。在印度-太平洋地區,海軍競爭和領土爭端日益加劇,促使各國對先進魚雷系統進行大規模投資,尤其是那些尋求擴大潛艦艦隊規模並確立水下主導地位的國家。沿海和群島國家正在加強反潛能力,並專注於發展適合淺水和擁擠水域的敏捷魚雷。在歐洲,重點是互通性和現代化,國防計畫通常旨在升級傳統魚雷,使其符合北約標準。該地區重視保護海上航線和應對地區不穩定局勢,這使得對重型和輕型魚雷的需求保持穩定。中東擁有戰略海上交通樞紐,其廣泛的海軍防禦網絡依靠魚雷,旨在保護沿海設施並遏制水面入侵。北美在技術先進性方面繼續保持領先,重點是先進的導引系統和與多域平台的整合。同時,現代化建設和區域合作正在逐步增強南美和非洲部分地區的魚雷能力。這反映出這些地區普遍認識到,有效的水下武器對於海上威懾、艦隊防禦和長期戰略安全規劃至關重要。

主要魚雷項目

印度國防部簽署了兩份旨在顯著提升該國潛艇能力的重要合約。其中一份是與法國海軍集團簽訂的購買先進電子重型魚雷 (EHWT) 的合同,價值 87.7 億盧比。另一份是與位於孟買的馬扎岡船塢造船廠簽訂的一份價值約199億盧比的重大合同,用於整合一套新的不依賴空氣推進系統(AIP)。 AIP技術由印度國防研究與發展組織(DRDO)自主研發,是 "自力更生的印度" (Atmanirbhar Bharat)願景的重大推動力。合併後的合約價值286.7億盧比,這是印度在提升潛艦艦隊續航力、殺傷力和自主能力方面邁出的重要一步。

本報告提供全球魚雷市場相關調查,彙整10年的各分類市場預測,技術趨勢,機會分析,企業簡介,各國資料等資訊。

目錄

魚雷市場報告定義

魚雷市場區隔

各地區

各啟動平台

各類型

未來10年魚雷市場分析

本章詳細概述了魚雷市場的成長、變化趨勢、技術採用概況和市場吸引力,並進行了10年的魚雷市場分析。

魚雷市場技術

本部分涵蓋了預計將影響該市場的十大技術,以及這些技術可能對整體市場產生的影響。

全球魚雷市場預測

本部分詳細介紹了該市場未來十年的魚雷市場預測,涵蓋了上述各個細分市場。

魚雷市場趨勢及各地區預測

本部分涵蓋了各地區魚雷市場的趨勢、推動因素、阻礙因素、課題以及政治、經濟、社會和技術層面。此外,也詳細介紹了區域市場預測和情境分析。區域分析的最後階段包括關鍵公司概況、供應商格局和公司基準分析。目前市場規模是基於正常業務情境估算的。

北美

促進因素,阻礙因素,課題

PEST

市場預測與情勢分析

主要企業

供應商階層的形勢

企業基準

歐洲

中東

亞太地區

南美

魚雷市場國家分析

本章涵蓋了該市場的主要國防項目,以及該市場的最新新聞和專利申請。此外,也提供了各國10年市場預測與情境分析。

美國

防衛計劃

最新消息

專利

這個市場上目前技術成熟度

市場預測與情勢分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

魚雷市場機會矩陣

魚雷市場報告相關專家的意見

結論

關於航空·國防市場報告

The Global Torpedo market is estimated at USD 1.35 billion in 2025, projected to grow to USD 4.33 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 12.36% over the forecast period 2025-2035.

Introduction to Torpedo Market:

Torpedoes are essential underwater weapons used primarily by submarines, surface ships, and aircraft to engage and neutralize naval threats. These self-propelled munitions are designed to track and destroy enemy submarines and surface vessels through direct impact or proximity detonation. Unlike naval mines or depth charges, torpedoes can actively seek out targets using onboard guidance systems, making them highly effective in both offensive and defensive maritime operations. Their relevance spans peacetime deterrence, wartime strike missions, and anti-access strategies. As maritime domains become more contested, torpedoes play a central role in undersea warfare by offering stealth, surprise, and lethality. Modern naval tactics increasingly depend on these weapons to maintain underwater superiority and strategic deterrence, especially in choke points and territorial waters. Equipped on a variety of platforms-from diesel-electric submarines to long-range patrol aircraft-torpedoes form a critical layer of naval capability. They are also instrumental in securing sea lines of communication and in deterring surface incursions by hostile navies. The global defense community continues to prioritize torpedo development, recognizing their enduring value in asymmetric and high-intensity conflict scenarios. Their continued evolution reflects a broader shift toward undersea dominance and integrated maritime combat readiness.

Technology Impact in Torpedo Market:

Technological advancements have profoundly reshaped the capabilities and roles of modern torpedoes in maritime defense. Innovations in propulsion systems have led to quieter and faster torpedoes, reducing detection risk while improving strike precision. Thermal engines, advanced electric motors, and improved hydrodynamics enable these weapons to operate over longer distances with greater stealth. In terms of guidance, newer models integrate advanced sonar, wake-homing sensors, and inertial navigation systems, allowing them to adapt to complex environments and outmaneuver countermeasures. Artificial intelligence and autonomous targeting algorithms are also emerging, enabling torpedoes to distinguish between decoys and legitimate threats with minimal operator input. Enhanced data-link capabilities provide mid-course updates, giving operators more control and flexibility after launch. Warhead design has evolved to deliver more focused and effective damage while maintaining compactness and safety. Additionally, modular architecture allows for rapid upgrades and mission-specific configurations. These technological gains are not only boosting lethality but also improving survivability against increasingly sophisticated anti-submarine warfare systems. Combined with integration into network-centric naval operations, modern torpedoes now serve as both strategic deterrents and precision tools in highly contested undersea environments, supporting mission success across both conventional and asymmetric maritime theaters.

Key Drivers in Torpedo Market:

Several critical factors are propelling the global development and deployment of torpedoes in contemporary naval strategies. The growing competition for dominance in undersea domains is a major influence, as nations seek to secure strategic waterways and maritime resources. Increased submarine activity-both for surveillance and deterrence-has underscored the need for effective underwater strike options. Evolving naval doctrines that prioritize layered defense and rapid-response capabilities reinforce the relevance of torpedoes in both offensive and defensive postures. The integration of unmanned platforms and the expansion of littoral operations require compact, efficient torpedoes capable of operating in shallow and confined waters. Concerns over anti-submarine threats in regional hotspots further drive investment in torpedoes designed to counter a variety of submersible and surface adversaries. Additionally, a focus on force projection in blue-water operations encourages the development of long-range and multi-role variants. Modern navies are also emphasizing self-reliance, prompting increased research into indigenous torpedo design and production. Operational readiness and flexible deployment options remain key goals, leading to enhancements in launch systems and storage capabilities. These drivers collectively reflect a strategic shift toward maintaining credible deterrence, improving tactical options at sea, and ensuring maritime superiority in an increasingly contested global security environment.

Regional Trends in Torpedo Market:

Torpedo development and deployment vary by region, shaped by distinct maritime strategies and threat perceptions. In the Indo-Pacific, heightened naval competition and territorial disputes have led to significant investments in advanced torpedo systems, particularly by nations aiming to expand their submarine fleets and assert undersea dominance. Coastal and archipelagic states are enhancing their anti-submarine capabilities, emphasizing agile torpedoes suited for shallow and congested waters. In Europe, the focus is on interoperability and modernization, with defense programs often aimed at upgrading legacy torpedoes to align with NATO standards. The region's emphasis on protecting sea lanes and responding to regional instability contributes to steady demand for both heavy and lightweight variants. The Middle East, with its strategic maritime chokepoints, relies on torpedoes as part of broader naval defense networks aimed at securing coastal installations and deterring surface incursions. North America continues to lead in terms of technological sophistication, emphasizing advanced guidance systems and integration with multi-domain platforms. Meanwhile, in South America and parts of Africa, torpedo capabilities are expanding gradually through modernization efforts and regional cooperation. Across these regions, the trajectory reflects a broader recognition that effective undersea weaponry is central to maritime deterrence, fleet defense, and long-term strategic security planning.

Key Torpedo Program:

India's Ministry of Defence has signed two major contracts aimed at significantly strengthening the country's submarine capabilities. One agreement, valued at ₹877 crore, was signed with France's Naval Group for the acquisition of advanced Electronic Heavy Weight Torpedoes (EHWT). The second and larger contract, worth approximately ₹1,990 crore, was signed with Mumbai-based Mazagon Dock Shipbuilders for the integration of a new Air Independent Propulsion (AIP) system. The AIP technology, developed indigenously by the Defence Research and Development Organisation (DRDO), is a major boost under the 'Atmanirbhar Bharat' (self-reliant India) initiative. Together, the contracts total ₹2,867 crore and mark a significant step forward in enhancing the endurance, lethality, and self-reliance of India's submarine fleet.

Table of Contents

Torpedo Market Report Definition

Torpedo Market Segmentation

By Region

By Launch Platform

By Type

Torpedo Market Analysis for next 10 Years

The 10-year torpedo market analysis would give a detailed overview of torpedo market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Torpedo Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Torpedo Market Forecast

The 10-year torpedo market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Torpedo Market Trends & Forecast

The regional torpedo market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Torpedo Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Torpedo Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Torpedo Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Launch Platform, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Launch Platform, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Torpedo Market Forecast, 2025-2035

- Figure 2: Global Torpedo Market Forecast, By Region, 2025-2035

- Figure 3: Global Torpedo Market Forecast, By Launch Platform, 2025-2035

- Figure 4: Global Torpedo Market Forecast, By Type, 2025-2035

- Figure 5: North America, Torpedo Market, Market Forecast, 2025-2035

- Figure 6: Europe, Torpedo Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Torpedo Market, Market Forecast, 2025-2035

- Figure 8: APAC, Torpedo Market, Market Forecast, 2025-2035

- Figure 9: South America, Torpedo Market, Market Forecast, 2025-2035

- Figure 10: United States, Torpedo Market, Technology Maturation, 2025-2035

- Figure 11: United States, Torpedo Market, Market Forecast, 2025-2035

- Figure 12: Canada, Torpedo Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Torpedo Market, Market Forecast, 2025-2035

- Figure 14: Italy, Torpedo Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Torpedo Market, Market Forecast, 2025-2035

- Figure 16: France, Torpedo Market, Technology Maturation, 2025-2035

- Figure 17: France, Torpedo Market, Market Forecast, 2025-2035

- Figure 18: Germany, Torpedo Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Torpedo Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Torpedo Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Torpedo Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Torpedo Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Torpedo Market, Market Forecast, 2025-2035

- Figure 24: Spain, Torpedo Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Torpedo Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Torpedo Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Torpedo Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Torpedo Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Torpedo Market, Market Forecast, 2025-2035

- Figure 30: Australia, Torpedo Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Torpedo Market, Market Forecast, 2025-2035

- Figure 32: India, Torpedo Market, Technology Maturation, 2025-2035

- Figure 33: India, Torpedo Market, Market Forecast, 2025-2035

- Figure 34: China, Torpedo Market, Technology Maturation, 2025-2035

- Figure 35: China, Torpedo Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Torpedo Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Torpedo Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Torpedo Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Torpedo Market, Market Forecast, 2025-2035

- Figure 40: Japan, Torpedo Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Torpedo Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Torpedo Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Torpedo Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Torpedo Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Torpedo Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Torpedo Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Torpedo Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Torpedo Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Torpedo Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Torpedo Market, By Launch Platform (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Torpedo Market, By Launch Platform (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Torpedo Market, By Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Torpedo Market, By Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Torpedo Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Torpedo Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Torpedo Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Torpedo Market, By Region, 2025-2035

- Figure 58: Scenario 1, Torpedo Market, By Launch Platform, 2025-2035

- Figure 59: Scenario 1, Torpedo Market, By Type, 2025-2035

- Figure 60: Scenario 2, Torpedo Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Torpedo Market, By Region, 2025-2035

- Figure 62: Scenario 2, Torpedo Market, By Launch Platform, 2025-2035

- Figure 63: Scenario 2, Torpedo Market, By Type, 2025-2035

- Figure 64: Company Benchmark, Torpedo Market, 2025-2035