|

市場調查報告書

商品編碼

1727194

戰鬥機模擬的全球市場:2025年~2035年Global Fighter Aircraft Simulation Market 2025-2035 |

||||||

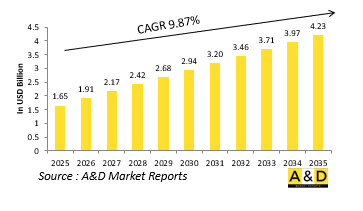

2025年全球戰鬥機模擬市場規模估計為16.5億美元,預計到2035年將增長至42.3億美元,2025-2035年預測期內的複合年增長率 (CAGR) 為9.87%。

戰鬥機模擬市場簡介:

戰鬥機模擬已成為現代空軍訓練和戰備的重要組成部分。這些系統複製了真實的飛行環境、作戰場景和複雜任務,使飛行員無需承擔真實飛行的風險和成本,即可發展和磨練技能。模擬可滿足廣泛的訓練需求,從基礎飛行指導到高階作戰機動、電子戰和聯合部隊協調。這些工具使機組人員能夠在受控環境中反覆練習高風險任務,在提高性能的同時保護設備並確保安全。此外,模擬器還允許團隊在各種威脅條件下演練不同的場景,從而有助於決策和戰術規劃。日益複雜的模擬器現在能夠模擬特定的敵方戰術、空域配置和環境挑戰。這種真實感不僅提升了飛行員的能力,也有助於各級指揮機構的策略思考與任務演練。戰鬥機模擬是部隊戰備的重要組成部分,彌合了理論知識與戰鬥經驗之間的差距。隨著現代空戰技術日益先進,情勢也愈發不可預測,模擬技術對於培養技能嫻熟、適應性強、隨時待命的機組人員而言,依然至關重要。

科技對戰鬥機模擬市場的影響:

技術進步大大擴展了戰鬥機模擬的功能,使其成為一種高保真訓練和作戰規劃工具。增強型視野系統提供了超逼真的3D環境,精準呈現了地形、天氣和空中威脅。運動平台重現了飛行的物理感受,而高解析度駕駛艙顯示器和觸覺控制系統則提供了接近真實場景的沉浸感。人工智慧透過產生逼真的敵方行為,讓受訓人員置身於動態且高度活躍的場景中,進一步增強了模擬效果。與數位孿生模型的集成,可以重現特定的飛機系統,用於技術訓練和性能分析。此外,聯網模擬現在允許多名飛行員和部隊在同步的大規模作戰場景中共同訓練,為聯合和聯軍演習提供支援。擴增實境和虛擬實境應用也正在興起,它們在保持高互動性的同時,實現了經濟高效、便攜的訓練方案。隨著這些系統的互聯互通程度不斷提高,它們越來越多地與即時飛行數據和任務報告工具集成,以支援持續的回饋和改進。這種數位技術的融合正在將模擬從一種補充工具轉變為現代空軍的核心能力。模擬可以增強任務演練,減少飛機磨損,並提高在複雜多變的作戰環境中的適應能力。

戰鬥機模擬市場的關鍵推動因素:

各種作戰、戰略和經濟因素正在推動全球國防部隊越來越重視戰鬥機模擬。其中最具影響力的因素之一是對經濟高效的訓練解決方案的需求。雖然實飛訓練需要大量的資源支出,包括燃料、維護和空域協調,但模擬器可以提供可重複、可擴展的訓練,而無需承擔相同的後勤負擔。模擬提供了一個安全的空間,用於練習緊急程序、作戰機動和複雜機動,避免人員或飛機暴露於真實危險之中。隨著現代空戰擴大採用電子戰套件、超視距飛彈和整合感測器等先進系統,模擬成為訓練飛行員綜合運用這些技術的關鍵平台。它還支援與其他軍種和盟軍進行聯合演習,為多域作戰做好準備。此外,全球威脅的不可預測性要求定期更新訓練並靈活應對各種場景,而模擬可以比真實演習更快地做出回應。最後,模擬在新飛行員的入職和技能提升中發揮關鍵作用,彌合了課堂學習與實際飛行之間的差距。這些綜合壓力已將模擬提升為維持現代空軍戰備和技術能力的戰略重點。

戰鬥機模擬市場的區域趨勢:

戰鬥機模擬系統的區域採用和發展反映了每個地區的國防戰略、訓練理念和技術基礎設施。在北美,尤其是美國,模擬已深深融入飛行員發展和任務演練計劃,重點是整合即時虛擬建構 (LVC) 訓練框架,以實現真實和模擬元素之間的無縫過渡。歐洲國家優先考慮模組化、可互通的系統,培育共享的訓練環境和標準化的任務協議,尤其是在支援北約成員國之間的聯盟行動方面。在亞太地區,空中力量的野心和不斷加劇的地區緊張局勢促使印度、日本和澳洲等國家大力投資先進的模擬器,以複製當地空域和威脅場景。這些系統通常與更廣泛的國防現代化目標一致,包括研發國產飛機。在中東,儘管環境嚴峻,用於實戰訓練的空域有限,但模擬在建立和維持戰備狀態方面發揮關鍵作用。拉丁美洲和非洲對模擬的採用則更具選擇性,通常與特定的現代化計劃以及與外國國防供應商的合作掛鉤。每個地區都在轉向將模擬技術不僅用於訓練,還用於作戰規劃、系統測試以及將未來能力融入不斷發展的作戰理論。

主要戰鬥機模擬項目:

據報道,日本正考慮向澳洲出口其下一代戰鬥機,該戰鬥機由日本與英國和義大利在全球空中作戰計畫 (GCAP) 下聯合研發。上個月,東京也邀請印度加入 GCAP 計畫。 2024 年 3 月,日本內閣放寬了對國防裝備出口的嚴格限制,為未來下一代戰鬥機的出口鋪平了道路。放寬限制的條件是,此類出口僅限於與日本簽訂了國防裝備和技術轉移協議的國家。此外,出口可能性將根據具體情況進行評估,並在執政聯盟內部討論後決定。

本報告提供全球戰鬥機模擬市場相關調查,彙整10年的各分類市場預測,技術趨勢,機會分析,企業簡介,各國資料等資訊。

目錄

戰鬥機模擬市場 - 目錄

戰鬥機模擬市場報告定義

戰鬥機模擬市場區隔

各地區

各技術

各用途

類別

未來十年戰鬥機模擬市場分析

本章透過對戰鬥機模擬市場十年的分析,詳細概述了戰鬥機模擬市場的成長、變化趨勢、技術採用概況以及整體市場吸引力。

戰鬥機模擬市場的市場技術

本部分涵蓋了預計將影響該市場的十大技術,以及這些技術對整體市場可能產生的影響。

全球戰鬥機模擬市場預測

本報告詳細介紹了未來十年該市場在上述細分領域的預測。

戰鬥機模擬市場趨勢及各地區預測

本部分涵蓋了各地區戰鬥機模擬市場的趨勢、推動因素、限制、挑戰以及政治、經濟、社會和技術層面。此外,本部分也詳細分析了各地區的市場預測和情境分析。區域分析包括主要公司概況、供應商格局和公司基準比較。目前市場規模是基於常規情境估算的。

北美

促進因素,阻礙因素,課題

PEST

市場預測與情勢分析

主要企業

供應商階層的形勢

企業基準

歐洲

中東

亞太地區

南美

門禁控制市場國家分析

本章涵蓋該市場的主要國防項目,以及該市場的最新新聞和專利申請。此外,也涵蓋了各國未來10年的市場預測與情境分析。

美國

防衛計劃

最新消息

專利

這個市場上目前技術成熟度

市場預測與情勢分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

戰鬥機模擬市場機會矩陣

戰鬥機模擬市場報告相關專家的意見

結論

關於航空·國防市場報告

The Global Fighter Aircraft Simulation market is estimated at USD 1.65 billion in 2025, projected to grow to USD 4.23 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 9.87% over the forecast period 2025-2035.

Introduction to Fighter Aircraft Simulation Market:

Fighter aircraft simulation has become an essential element in the training and operational readiness of modern air forces. These systems replicate real-world flying environments, combat scenarios, and mission complexities, allowing pilots to develop and refine skills without the risks and costs of actual flight. Simulation supports a wide spectrum of training needs-from basic flight instruction to advanced combat maneuvers, electronic warfare, and joint-force coordination. These tools enable aircrews to repeatedly practice high-risk missions in a controlled setting, improving performance while preserving equipment and ensuring safety. Additionally, simulators contribute to decision-making and tactical planning by allowing teams to rehearse various scenarios under different threat conditions. With increasing sophistication, they can now mimic specific enemy tactics, airspace configurations, and environmental challenges. This realism not only enhances pilot competence but also supports strategic thinking and mission rehearsal across all levels of command. Fighter aircraft simulation is a critical component of force preparedness, bridging the gap between theoretical knowledge and live operational experience. As modern air combat grows more technologically advanced and unpredictable, simulation continues to be a key resource for cultivating skilled, adaptive, and mission-ready aircrews worldwide.

Technology Impact in Fighter Aircraft Simulation Market:

Technological advancement has dramatically expanded the capabilities of fighter aircraft simulation, turning it into a high-fidelity training and operational planning tool. Enhanced visual systems now provide ultra-realistic 3D environments, accurately representing landscapes, weather, and aerial threats. Motion platforms replicate the physical sensations of flight, while high-resolution cockpit displays and tactile controls provide immersion that closely mirrors real-world conditions. Artificial intelligence has further improved simulations by generating realistic adversary behaviors, challenging trainees with dynamic, responsive scenarios. Integration with digital twin models enables the replication of specific aircraft systems for technical training and performance analysis. Furthermore, networked simulations now allow multiple pilots and units to train together in synchronized, large-scale combat scenarios, supporting joint and coalition exercises. Augmented and virtual reality applications are also gaining ground, enabling cost-effective, portable training options that retain high interactivity. As these systems become more connected, they are increasingly integrated with live flight data and mission debriefing tools, supporting continuous feedback and improvement. This convergence of digital technologies has transformed simulation from a supplemental tool into a core capability for modern air forces. It enhances mission rehearsal, reduces wear on aircraft, and fosters adaptability in complex, fast-changing combat environments.

Key Drivers in Fighter Aircraft Simulation Market:

A range of operational, strategic, and economic factors is driving the growing emphasis on fighter aircraft simulation across global defense forces. One of the most influential drivers is the need for cost-effective training solutions. Live flight training involves significant resource expenditure, including fuel, maintenance, and airspace coordination, whereas simulators offer repeated, scalable training without the same logistical burden. Safety is another compelling factor; simulation provides a secure space to practice emergency procedures, combat engagements, and complex maneuvers without exposing personnel or aircraft to actual risk. As modern air combat increasingly incorporates advanced systems-such as electronic warfare suites, beyond-visual-range missiles, and integrated sensors-simulation offers a vital platform for pilots to train in using these technologies cohesively. It also supports preparation for multi-domain operations by enabling joint exercises with other branches or allied forces. Additionally, the unpredictability of global threats necessitates regular training updates and scenario flexibility, something simulation can accommodate much faster than real-world exercises. Lastly, simulation plays a crucial role in onboarding and upskilling new pilots, bridging the gap between classroom learning and live flight. These combined pressures have elevated simulation to a strategic priority in sustaining operational readiness and technological competence in modern air forces.

Regional Trends in Fighter Aircraft Simulation Market:

Regional adoption and evolution of fighter aircraft simulation systems reflect each area's defense strategies, training philosophies, and technological infrastructure. In North America, particularly within the United States, simulation is deeply embedded in pilot development and mission rehearsal programs, with a focus on integrating live-virtual-constructive (LVC) training frameworks that allow seamless transition between real and simulated elements. European nations prioritize modular and interoperable systems to support coalition-based operations, especially among NATO members, fostering shared training environments and standardized mission protocols. In the Asia-Pacific region, growing airpower ambitions and regional tensions have led countries like India, Japan, and Australia to invest heavily in advanced simulators that replicate local airspace and threat scenarios. These systems are often aligned with broader defense modernization goals, including indigenous aircraft development. In the Middle East, simulation plays a key role in building and maintaining combat readiness despite challenging environments and limited airspace for live training. Adoption in Latin America and Africa is more selective, often tied to specific modernization programs or partnerships with foreign defense suppliers. Across all regions, there is a growing shift toward using simulation not just for training but also for operational planning, system testing, and integrating future capabilities into evolving combat doctrines.

Key Fighter Aircraft Simulation Program:

Japan is reportedly considering the export of its next-generation fighter aircraft-currently being co-developed with the UK and Italy under the Global Combat Air Programme (GCAP)-to Australia. Last month, Tokyo also extended an invitation to India to join the GCAP initiative. In March 2024, the Japanese cabinet eased the country's strict regulations on defense equipment exports, creating a pathway for the future export of next-gen fighter jets. The relaxation of these rules is based on the condition that such exports will be limited to nations that have existing defense equipment and technology transfer agreements with Japan. Additionally, each potential export will be assessed individually, with decisions made following internal consultations within the ruling coalition.

Table of Contents

Fighter Aircraft SIMULATION Market - Table of Contents

Fighter Aircraft SIMULATION market Report Definition

Fighter Aircraft SIMULATION market Segmentation

By Region

By Technology

By Application

By Type

Fighter Aircraft SIMULATION market Analysis for next 10 Years

The 10-year Fighter Aircraft SIMULATION market analysis would give a detailed overview of Fighter Aircraft SIMULATION market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Fighter Aircraft SIMULATION market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Fighter Aircraft SIMULATION market Forecast

The 10-year Fighter Aircraft SIMULATION market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Fighter Aircraft SIMULATION market Trends & Forecast

The regional Fighter Aircraft SIMULATION market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Fighter Aircraft SIMULATION market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Fighter Aircraft SIMULATION market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Technology, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Technology, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Fighter Aircraft Simulation Market Forecast, 2025-2035

- Figure 2: Global Fighter Aircraft Simulation Market Forecast, By Region, 2025-2035

- Figure 3: Global Fighter Aircraft Simulation Market Forecast, By Type, 2025-2035

- Figure 4: Global Fighter Aircraft Simulation Market Forecast, By Technology, 2025-2035

- Figure 5: Global Fighter Aircraft Simulation Market Forecast, By Application, 2025-2035

- Figure 6: North America, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 7: Europe, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 9: APAC, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 10: South America, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 11: United States, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 12: United States, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 13: Canada, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 15: Italy, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 17: France, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 18: France, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 19: Germany, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 25: Spain, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 31: Australia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 33: India, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 34: India, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 35: China, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 36: China, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 41: Japan, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Fighter Aircraft Simulation Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Fighter Aircraft Simulation Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Fighter Aircraft Simulation Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Fighter Aircraft Simulation Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Fighter Aircraft Simulation Market, By Type (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Fighter Aircraft Simulation Market, By Type (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Fighter Aircraft Simulation Market, By Technology (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Fighter Aircraft Simulation Market, By Technology (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Fighter Aircraft Simulation Market, By Application (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Fighter Aircraft Simulation Market, By Application (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Fighter Aircraft Simulation Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Fighter Aircraft Simulation Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Fighter Aircraft Simulation Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Fighter Aircraft Simulation Market, By Region, 2025-2035

- Figure 61: Scenario 1, Fighter Aircraft Simulation Market, By Type, 2025-2035

- Figure 62: Scenario 1, Fighter Aircraft Simulation Market, By Technology, 2025-2035

- Figure 63: Scenario 1, Fighter Aircraft Simulation Market, By Application, 2025-2035

- Figure 64: Scenario 2, Fighter Aircraft Simulation Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Fighter Aircraft Simulation Market, By Region, 2025-2035

- Figure 66: Scenario 2, Fighter Aircraft Simulation Market, By Type, 2025-2035

- Figure 67: Scenario 2, Fighter Aircraft Simulation Market, By Technology, 2025-2035

- Figure 68: Scenario 2, Fighter Aircraft Simulation Market, By Application, 2025-2035

- Figure 69: Company Benchmark, Fighter Aircraft Simulation Market, 2025-2035

2026-2030年全球軍工及航太半導體市場

2026-2030年全球軍工及航太半導體市場 全球運輸機飛行模擬市場:2026-2036 年軍事航太模擬與訓練市場報告:趨勢、預測及競爭分析(至2035年)

全球運輸機飛行模擬市場:2026-2036 年軍事航太模擬與訓練市場報告:趨勢、預測及競爭分析(至2035年) 無人機培訓市場按培訓模式、平台類型、交付方式、培訓類型和最終用戶分類-全球預測,2026-2032年

無人機培訓市場按培訓模式、平台類型、交付方式、培訓類型和最終用戶分類-全球預測,2026-2032年