|

市場調查報告書

商品編碼

1714096

表面材料測試:全球 2025-2035Global Surface material testing Market 2025-2035 |

||||||

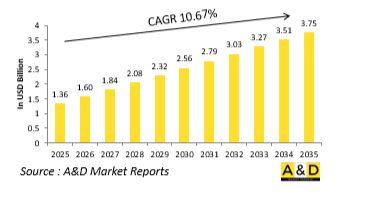

全球表面材料測試市場規模預計將從 2025 年的 13.6 億美元增長到 2035 年的 37.5 億美元,預測期內的複合年增長率為 10.67%。

表面材料測試市場:簡介

國防表面材料測試在認證陸地、海洋、空中和太空領域使用的軍事資產的耐用性、生存力和任務準備度方面發揮著至關重要的作用。任何平台的性能和安全性,無論是裝甲車、飛機機身、海軍艦船船體或飛彈船體,在很大程度上取決於材料在極端環境、機械和戰鬥壓力下的行為。表面測試評估抗腐蝕、耐磨、抗熱降解、抗彈衝擊、抗化學腐蝕和抗疲勞性能,以確保塗層和建築材料符合嚴格的國防規範。該評估還擴展到特殊表面處理,例如隱形塗料、防反射塗層、雷達吸波材料 (RAM) 和用於高溫環境的熱障塗層。軍事平台在惡劣的環境中運行,包括高度腐蝕的海上環境、塵土飛揚的沙漠、寒冷的北極條件和高速空域,材料故障不僅代價高昂,而且可能致命。因此,表面材料測試貫穿國防產品的整個生命週期,從開發和原型設計階段,到現場驗證,再到操作和維持階段,是性能鑑定和生命週期保證計劃的核心要素。

表面材料測試市場:技術的影響

技術的進步從根本上改變了國防部門表面材料測試的方式,使其更加準確、高效和可預測。例如,超音波相控陣成像、數位射線照相和渦流掃瞄等先進的無損檢測 (NDT) 技術能夠在不損壞材料的情況下對塗層和基材進行詳細的內部檢查。同時,利用雷射燒蝕和掃瞄電子顯微鏡(SEM)進行微觀表面分析可以揭示操作條件下的降解機制和微觀結構變化,幫助國防工程師更深入地瞭解材料。此外,機器學習演算法被納入表面測試系統,以自動識別人眼可能錯過的磨損、腐蝕和裂縫模式,從而實現預防性維護計劃。同時,實驗室配備了自動化測試台和機械手臂,以確保在磨損、黏附和抗衝擊測試中一致地施加負載、壓力和暴露循環。此外,能夠複製極端高溫、潮濕、鹽霧和沙塵暴等惡劣環境的模擬環境室已成為加速降解分析的標準設備。這些技術進步與表面處理部件的數位孿生相結合,可以模擬不同作戰環境和氣候條件下的長期材料行為。因此,確保國防系統表面完整性的方法變得更加數據驅動和動態,同時支援準備和持久性。

表面材料測試市場:關鍵推動因素

多種戰略、營運和監管因素正在推動全球國防計畫對錶面材料測試的需求不斷增加。其中一個主要因素是現代戰爭越來越注重生存力和隱身性。這對錶面塗層和飾面提出了極其嚴格的要求。隨著雷達、紅外線、可見光和其他探測技術變得越來越複雜,軍事平台越來越依賴先進的表面處理技術,例如雷達吸波材料 (RAM)、啞光塗層和隱形複合材料,以保持低可探測性,對這些技術的測試也急劇增加。下一個問題是多環境相容性的需求日益增長。軍事裝備必須在各種地形和氣候條件下可靠運行,從高鹽度的海洋環境到炎熱的沙漠地區和冰凍的極地地區。這使得全面的測試對於確保耐腐蝕性、耐熱性和抗顆粒磨損性至關重要。此外,新型複合材料和奈米塗層的出現要求相應的監管和性能驗證流程也隨之發展,需要實施新的或修訂的測試協議。此外,國防採購政策正在發生變化,越來越要求在生產或出口批准之前對錶面性能進行嚴格的驗證。這使得表面測試成為合約執行過程中的一個重要里程碑。最後,延長傳統平台生命週期的趨勢也推動了對長期使用過程中表面退化測試的需求。這樣可以實現具有成本效益的升級而不是大修,從而優化可維護性和使用壽命。

本報告調查了全球表面材料測試市場,並總結了當前的市場狀況、技術趨勢、市場影響因素分析、市場規模趨勢和預測、按地區進行的詳細分析、競爭格局以及主要公司的概況。

目錄

國防領域的世界表面材料測試:目錄

國防領域的世界表面材料測試:報告定義

全球國防部門表面材料測試

按地區

按類型

按引擎型別

依用途

未來10年國防領域全球表面材料測試分析

全球表面材料測試市場在國防部門的技術

國防部門全球表面材料測試預測

全球各地區國防部門表面材料測試趨勢及預測

北美

促進因素、阻礙因素與課題

抑制因子

市場預測與情境分析

主要公司

供應商層級結構

企業基準

歐洲

中東

亞太地區

南美洲

全球國防表面材料測試國家分析

美國

國防計畫

最新消息

專利

目前技術成熟度

市場預測與情境分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

國防部門的全球表面材料測試:機會矩陣

全球國防部門表面材料測試:專家意見

概述

關於航空和國防市場報告

The Global Surface material testing market is estimated at USD 1.36 billion in 2025, projected to grow to USD 3.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 10.67% over the forecast period 2025-2035.

Introduction to Surface material testing Market:

Surface material testing in the defense sector plays a pivotal role in certifying the durability, survivability, and mission-readiness of military assets across air, land, sea, and space domains. The performance and safety of platforms-ranging from armored vehicles and aircraft fuselages to naval hulls and missile casings-depend heavily on how materials behave under extreme environmental, mechanical, and combat-related stressors. Surface testing involves evaluating resistance to corrosion, abrasion, thermal degradation, ballistic impact, chemical exposure, and fatigue, ensuring that coatings and structural materials meet rigorous defense specifications. These assessments extend to specialized surface treatments like stealth coatings, anti-reflective finishes, radar-absorbing materials (RAM), and thermal barrier coatings used in high-temperature environments. With defense platforms often operating in corrosive maritime settings, sand-laden deserts, arctic cold, or high-speed aerial regimes, material failure is not just costly-it can be catastrophic. Therefore, surface material testing is integrated into every stage of the defense product lifecycle, from development and prototyping to field validation and sustainment, forming a critical component of performance certification and lifecycle assurance programs.

Technology Impact in Surface material testing Market:

Technological progress is revolutionizing the way surface material testing is conducted in defense applications, introducing greater precision, efficiency, and predictive capability. Advanced non-destructive testing (NDT) techniques such as ultrasonic phased-array imaging, digital radiography, and eddy current scanning now enable detailed inspection of coatings and substrates without compromising material integrity. In parallel, laser ablation and scanning electron microscopy (SEM) provide micro-level surface analysis, helping defense engineers understand degradation mechanisms and microstructural changes under operational conditions. Machine learning algorithms are increasingly embedded into surface testing systems to identify patterns of wear, corrosion, or cracking that may escape human detection, allowing for proactive maintenance scheduling. Meanwhile, the adoption of automated test rigs and robotic arms in laboratory environments ensures consistent pressure application and exposure cycles in abrasion, adhesion, and impact resistance tests. Simulated environmental chambers-capable of replicating extreme heat, humidity, salt fog, and sandstorms-have become standard for accelerated aging analysis. These technological upgrades are complemented by digital twins of surface-treated components, allowing defense agencies to simulate long-term material behavior in various combat or climatic scenarios. The result is a more data-rich and dynamic approach to ensuring surface integrity, supporting both readiness and resilience in defense systems.

Key Drivers in Surface material testing Market:

Multiple strategic, operational, and regulatory factors are driving the demand for robust surface material testing in global defense programs. A primary driver is the increasing emphasis on survivability and stealth in modern combat environments, which places stringent requirements on surface coatings and finishes. As radar, infrared, and visual detection technologies become more advanced, platforms must rely on sophisticated surface treatments to reduce signatures and avoid detection. This has led to a surge in testing for radar-absorbent materials, matte coatings, and low-observable composites. Another key driver is the growing demand for multi-environment versatility, with military assets required to function reliably across diverse terrains-from corrosive saltwater environments to scorching desert theaters and sub-zero polar regions. These varied operational settings necessitate comprehensive testing for corrosion resistance, thermal stability, and particulate abrasion. Furthermore, as new composite materials and nano coatings enter the defense market, regulatory and performance validation processes must catch up, necessitating new or modified testing protocols. Defense procurement policies are also evolving to require more extensive verification of surface performance before full-scale production or export approval, making testing a key milestone in contract fulfillment. In addition, the trend toward lifecycle extension of legacy platforms drives increased testing of surface degradation over time, enabling cost-effective upgrades instead of full replacements.

Regional Trends in Surface material testing Market:

The development and application of surface material testing in defense vary significantly across regions, shaped by distinct operational priorities, threat perceptions, and industrial capacities. In North America, the United States leads in surface testing sophistication, with DoD-backed research institutions and defense OEMs investing heavily in materials for signature reduction, thermal shielding, and corrosion resistance. Facilities across the U.S. support multi-domain testing, including naval testing for anti-fouling coatings and aviation-focused labs for high-velocity erosion analysis. Canada complements this with a strong focus on testing materials for arctic resilience and NATO interoperability. In Europe, nations such as Germany, the UK, and France emphasize high-performance surface treatments for air and ground systems, with extensive research into hybrid coatings that combine camouflage with environmental resistance. European defense consortia often collaborate with universities and advanced materials laboratories, supporting integrated surface testing for multinational programs like Eurofighter and FCAS. Asia-Pacific presents a mixed but rapidly evolving landscape: China is scaling up its testing infrastructure to support its expanding domestic defense manufacturing sector, with particular emphasis on naval coatings, thermal-resistant composites, and stealth materials for its new-generation aircraft and missile systems. India, through DRDO and state-run laboratories, is expanding its capabilities to test surface treatments for a wide range of indigenous platforms including the Tejas fighter and INS-class naval vessels. Japan and South Korea, although more technologically mature, maintain highly specialized testing ecosystems focused on precision coatings and export-compliant materials. In the Middle East, nations like the UAE and Saudi Arabia are rapidly developing in-country testing facilities as part of broader localization agendas. These include corrosion and wear testing centers designed for desert and maritime environments, often developed through partnerships with global defense contractors. Globally, the emphasis on tailored surface testing is increasing as platforms become more complex and versatile, and as countries seek greater autonomy in defense technology development and validation.

Key Defense Surface material testing Program:

BEML has entered into a strategic partnership with Goa Shipyard Limited (GSL) to collaborate on maritime and composite technology projects. Under a newly signed Memorandum of Understanding (MoU), the two state-owned entities will focus on the production of glass fibre-reinforced polymer (GFRP) composite components and assemblies for both defence and commercial applications, along with other specialized marine equipment, BEML announced in a statement. As part of the agreement, BEML will also make use of GSL's ship lift facility and dry dock for the maintenance, repair, and overhaul of yard crafts, tugs, and vessels operated by the Indian Navy, Indian Coast Guard, and merchant fleets. The MoU was formally exchanged by BEML Chairman and Managing Director Shantanu Roy and GSL CMD Brajesh Kumar Upadhyay during Aero India 2025 in Bengaluru.

Table of Contents

Global Surface material testing in defense- Table of Contents

Global Surface material testing in defense Report Definition

Global Surface material testing in defense Segmentation

By Region

By Type

By Engine Type

By Application

Global Surface material testing in defense Analysis for next 10 Years

The 10-year Global Surface material testing in defense analysis would give a detailed overview of Global Surface material testing in defense growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Surface material testing in defense

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Surface material testing in defense Forecast

The 10-year Global Surface material testing in defense forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global Surface material testing in defense Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global Surface material testing in defense

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Surface material testing in defense

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Surface material testing in defense

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Material, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Methods, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Material, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Methods, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Surface Material Testing Market Forecast, 2025-2035

- Figure 2: Global Surface Material Testing Market Forecast, By Region, 2025-2035

- Figure 3: Global Surface Material Testing Market Forecast, By Material, 2025-2035

- Figure 4: Global Surface Material Testing Market Forecast, By Methods, 2025-2035

- Figure 5: Global Surface Material Testing Market Forecast, By Type, 2025-2035

- Figure 6: North America, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 7: Europe, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 9: APAC, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 10: South America, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 11: United States, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 12: United States, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 13: Canada, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 15: Italy, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 17: France, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 18: France, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 19: Germany, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 25: Spain, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 31: Australia, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 33: India, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 34: India, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 35: China, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 36: China, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 41: Japan, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Surface Material Testing Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Surface Material Testing Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Surface Material Testing Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Surface Material Testing Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Surface Material Testing Market, By Material (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Surface Material Testing Market, By Material (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Surface Material Testing Market, By Methods (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Surface Material Testing Market, By Methods (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Surface Material Testing Market, By Type (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Surface Material Testing Market, By Type (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Surface Material Testing Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Surface Material Testing Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Surface Material Testing Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Surface Material Testing Market, By Region, 2025-2035

- Figure 61: Scenario 1, Surface Material Testing Market, By Material, 2025-2035

- Figure 62: Scenario 1, Surface Material Testing Market, By Methods, 2025-2035

- Figure 63: Scenario 1, Surface Material Testing Market, By Type, 2025-2035

- Figure 64: Scenario 2, Surface Material Testing Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Surface Material Testing Market, By Region, 2025-2035

- Figure 66: Scenario 2, Surface Material Testing Market, By Material, 2025-2035

- Figure 67: Scenario 2, Surface Material Testing Market, By Methods, 2025-2035

- Figure 68: Scenario 2, Surface Material Testing Market, By Type, 2025-2035

- Figure 69: Company Benchmark, Surface Material Testing Market, 2025-2035

材料測試市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、最終用途產業、地區和競爭格局分類,2021-2031年

材料測試市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、材料、最終用途產業、地區和競爭格局分類,2021-2031年 材料測試市場:依測試類型、材料類型、技術、服務類型、最終用途產業分類,全球預測(2026-2032)冶金測試與分析服務市場:按服務類型、測試方法、材料類型、服務提供者、應用和最終用戶分類-2026-2032年全球預測

材料測試市場:依測試類型、材料類型、技術、服務類型、最終用途產業分類,全球預測(2026-2032)冶金測試與分析服務市場:按服務類型、測試方法、材料類型、服務提供者、應用和最終用戶分類-2026-2032年全球預測 材料測試市場報告:按類型、材料、最終用途行業和地區分類(2026-2034 年)全球通用材料試驗機市場(按機器類型、負載能力、材料、技術、最終用戶和應用分類)—2026-2032年預測奈米顆粒材料表徵服務市場:依表徵技術、材料類型、服務模式、終端用戶產業和應用分類-全球預測,2026-2032年

材料測試市場報告:按類型、材料、最終用途行業和地區分類(2026-2034 年)全球通用材料試驗機市場(按機器類型、負載能力、材料、技術、最終用戶和應用分類)—2026-2032年預測奈米顆粒材料表徵服務市場:依表徵技術、材料類型、服務模式、終端用戶產業和應用分類-全球預測,2026-2032年 全球材料測試市場(至 2030 年)按類型(萬能試驗機、伺服試驗機、硬度試驗機)、材料(金屬、塑膠、橡膠和彈性體)、最終用戶(汽車、建築)和地區分類

全球材料測試市場(至 2030 年)按類型(萬能試驗機、伺服試驗機、硬度試驗機)、材料(金屬、塑膠、橡膠和彈性體)、最終用戶(汽車、建築)和地區分類 全球節能材料市場

全球節能材料市場 材料測試市場:依產品類型、依材料類型、依最終用途產業、按地區日本材料測試市場報告(按類型、材料、最終用途行業和地區)2025-2033

材料測試市場:依產品類型、依材料類型、依最終用途產業、按地區日本材料測試市場報告(按類型、材料、最終用途行業和地區)2025-2033