|

市場調查報告書

商品編碼

1706589

防彈背心的全球市場:2025年~2035年Global Bullet Proof Vests Market 2025-2035 |

||||||

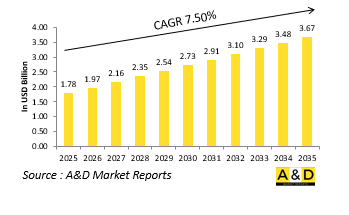

2025 年全球防彈背心市場規模估計為 17.8 億美元,預計到 2035 年將增長到 36.7 億美元,2025-2035 年預測期內的複合年增長率 (CAGR) 為 7.50%。

防彈背心市場簡介:

防彈背心,也稱為防彈衣或防彈衣,是軍事防護裝備的基本組成部分。這些背心旨在保護士兵免受彈道威脅、破片和彈片的傷害,在提高作戰行動中的生存能力方面發揮著至關重要的作用。現代戰爭的強度和複雜性不斷增加,推動著全球軍用防彈衣市場的發展,其中不對稱威脅、城市作戰和高速彈對地面部隊構成了越來越大的風險。

與民用或執法防彈衣相比,軍用防彈衣通常設計用於更高水準的防護和操作適應性。它們通常包含軟裝甲板(由先進的芳綸纖維或聚乙烯製成)和硬陶瓷或複合板,可防禦步槍子彈和穿甲彈。除了防彈之外,軍用背心還在不斷研發,以支援模組化承重系統、整合通訊設備並優化重量分佈,從而提高機動性和耐用性。隨著世界各地的國防官員轉向多領域戰爭,為步兵配備下一代防彈衣已成為當務之急。無論是在反恐行動中面對叛亂勢力,或是在常規戰場上,士兵越來越依賴先進的防彈衣作為綜合部隊防護戰略的一部分。

科技對防彈背心市場的影響:

技術進步正在推動現代軍用防彈衣的設計、材料和功能發生重大變化。從傳統的凱夫拉材料到超高分子量聚乙烯 (UHMWPE) 和碳奈米材料的轉變使得裝甲系統更輕、更堅固、更靈活。這些材料以極低的重量提供同等或更好的防彈保護,減輕了戰場士兵的疲勞並提高了作戰耐力。碳化矽和碳化硼等複合陶瓷已得到改進,可用於硬質裝甲鍍層,使它們能夠以最小的剝落和創傷擊穿穿甲彈。這些陶瓷打擊表面與先進的背襯層相結合,使背心能夠滿足 III 級和 IV 級防護標準,同時仍保持符合人體工學的擴展。

不僅材料,穿戴式電子設備和感測器的整合也增加了防彈背心的實用性。一些軍隊目前正在部署配備生命徵象監測器、GPS定位器和可直接與指揮系統介面的通訊模組的智慧背心。這些穿戴式科技系統能夠實現即時健康追蹤和態勢感知,縮短傷患後送和醫療分類的反應時間。溫度調節技術也被引入背心設計。相變材料和被動通風系統等創新有助於散發積聚的熱量,這在高溫操作環境中至關重要。同樣,承重外骨骼介面和模組化重量平衡等人體工學增強功能可以延長佩戴時間並提高舒適度。

另一個創新領域是自適應和可擴展裝甲系統的出現。該背心現在可以配置可拆卸面板和升級板,從而可以根據任務風險評估進行動態威脅適應。其他設計採用了液體裝甲技術,在受到撞擊時會立即變硬,從而提供靈活的解決方案,以適應使用者的動作並保持保護。

防彈背心市場的主要推動因素:

多種策略、營運和地緣政治因素正在推動全球軍用防彈衣需求的成長和演變。

隨著世界各地衝突和城市戰爭的增加,個人防護變得至關重要。從東歐到中東和非洲部分地區,常規戰爭和叛亂活動死灰復燃,使前線部隊處於小型武器和爆炸物威脅猖獗的高風險環境中。這就是為什麼軍事規劃人員優先考慮廣泛使用高性能防彈衣。現代化和士兵殺傷力計劃是另一個關鍵推動因素。世界各國都在投資下一代步兵項目,如美國陸軍的士兵防護系統(SPS)、法國的FELIN和印度的F-INSAS,其中防彈背心是模組化作戰裝備的核心部分。這些項目旨在為士兵配備整合的、高度機動的裝甲系統,同時支援技術增強和任務客製化。

不斷演變的威脅狀況,包括國家和非國家行為者使用穿甲彈,促使軍隊升級其防護標準。傳統的軟質防彈衣在許多作戰情況下已不再適用,因此需要採用結合軟質和硬質防彈衣組件的混合防彈衣系統。部隊部署和維和行動也產生了對輕便、可擴展背心的需求。在海外戰場執行人道或穩定任務的部隊需要能夠提供足夠保護的裝備,而不必承受全套作戰裝備的沉重負擔。這促使具有模組化保護區的適應性背心的採購量增加。

此外,人們越來越重視士兵的生存能力,不僅要保證他們免受彈道威脅,還要保證他們免受鈍性創傷、爆炸超壓和熱應激等二次傷害,這推動了對人體工學和生理防護的研究和開發投資。最後,產業創新和國防合作正在影響供應鏈動態。軍事組織和先進材料科學公司之間的合作正在加速防彈背心的開發步伐,跨國合作正在促進技術轉移和聯合製造。

防彈背心市場的區域趨勢:

美國在軍用防彈衣的研發和部署方面仍然處於世界領先地位。美國陸軍的綜合視覺增強系統 (IVAS) 和增強型小型武器防護插入件 (ESAPI) 等大規模現代化項目反映了對輕量化、模組化和任務適應性背心的持續追求。此外,美國正在探索 "隱形裝甲" 解決方案,為特種作戰部隊和情報部隊提供可隱藏但防護性極強的背心。加拿大也致力於透過針對寒冷氣候和北極地區優化的防護裝備來提高部隊的生存能力。作為北約互操作性目標的一部分,歐洲軍隊正在投資先進的防彈衣並升級其國防。德國、法國和英國正在部署具有增強型創傷防護功能的可擴展系統,而波蘭和波羅的海國家等東歐國家正在迅速升級其步兵裝備以應對地區緊張局勢。歐洲國防工業也正在根據歐盟環境指令開發可持續和可回收的彈道材料。

亞太地區軍用防彈背心市場正快速擴張。中國正積極為其不斷成長的軍隊開發下一代防彈背心,將智慧紡織品和防創傷設計納入標準裝備。印度正在投資自主生產適合高海拔作業的輕型背心,尤其是在其北部邊境。日本和韓國正在對其個人防護設備進行現代化升級,以支持聯盟行動並應對區域威脅。在中東,持續的衝突、不對稱戰爭和邊境安全問題正在推動人們採用該技術。以色列繼續在輕型、高性能裝甲解決方案方面處於領先地位,沙烏地阿拉伯和阿拉伯聯合大公國等國家也為其常規和國內安全部隊採購防彈背心。該地區民間參與國防裝備生產的現像也在增加,防彈背心的生產正在本地化,以減少對進口的依賴。

在非洲,重點是為反叛亂、邊境安全和維和部隊提供裝備。儘管預算限制使得廣泛分發高品質防彈背心變得困難,但尼日利亞、埃及和肯亞等國家正在透過國際防禦援助、聯合國計畫和雙邊軍事夥伴關係對防彈背心進行投資。這些輕便、氣候友善的背心兼具經濟性和防護性,在整個非洲大陸越來越受歡迎。拉丁美洲國家,特別是巴西、哥倫比亞和墨西哥,在軍事和準軍事行動中使用防彈背心。其中包括禁毒運動和打擊國內恐怖主義。防彈背心的重點是低調、多用途的背心,可以在從叢林到城市地區的各種地形中穿著,並提供對彈道和刀刃武器的保護。

主要防彈背心項目

印度國防部簽署了一份價值 639 億盧比的合同,為印度陸軍採購 186,000 件自主研發的防彈背心。該合約已與印度國內一家國防製造商敲定,預計將透過促進國防領域的本地生產,為政府的 "印度製造" 計劃提供重大推動。這些先進的防彈衣將為陸軍士兵提供增強的保護,同時彰顯該國對國防製造業自力更生的承諾。

本報告提供全球防彈背心市場相關調查,彙整10年的各分類市場預測,技術趨勢,機會分析,企業簡介,各國資料等資訊。

目錄

全球防彈背心市場報告定義

全球防彈背心市場區隔

各類型

各地區

各終端用戶

未來10年全球防彈背心市場分析

對全球防彈背心市場十多年的分析提供了有關成長、變化趨勢、技術採用概況和市場吸引力的詳細概述。

全球防彈背心市場的市場技術

本部分涵蓋預計將影響該市場的十大技術以及這些技術可能對整個市場產生的影響。

全球防彈背心市場預測

針對該市場未來十年的全球防彈背心市場預測已涵蓋上述各個細分市場。

防彈背心市場趨勢及各地區預測

本部分涵蓋防彈背心市場的區域趨勢、推動因素、阻礙因素、課題以及政治、經濟、社會和技術方面。它還提供了詳細的區域市場預測和情境分析。區域分析包括主要公司概況、供應商格局和公司基準測試。目前市場規模是根據正常業務情境估算的。

北美

促進因素,阻礙因素,課題

PEST

市場預測與情勢分析

主要企業

供應商階層的形勢

企業基準

歐洲

中東

亞太地區

南美

各國防彈背心市場分析

本章重點介紹該市場的主要防禦計劃,並介紹該市場的最新新聞和專利。它還提供國家級的 10 年市場預測和情境分析。

美國

最新消息

專利

這個市場上目前技術成熟度

市場預測與情勢分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

全球防彈背心市場機會矩陣

防彈背心市場報告相關專家的意見

結論

關於航空·國防市場報告

The Global Bullet Proof Vests market is estimated at USD 1.78 billion in 2025, projected to grow to USD 3.67 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 7.50% over the forecast period 2025-2035.

Introduction to Bullet Proof Vests Market:

Bulletproof vests, also referred to as ballistic vests or body armor, are fundamental components of military protective equipment. Designed to shield soldiers from ballistic threats, fragmentation, and shrapnel, these vests play a critical role in enhancing survivability during combat operations. The global market for military bulletproof vests is driven by the increasing intensity and complexity of modern warfare, where asymmetric threats, urban combat, and high-velocity projectiles pose ever-growing risks to ground forces.

In contrast to civilian or law enforcement armor, military-grade vests are typically engineered for higher protection levels and operational adaptability. They often incorporate both soft armor panels (made from advanced aramid fibers or polyethylene) and hard ceramic or composite plates, offering defense against rifle rounds and armor-piercing ammunition. Beyond ballistic protection, military vests are also being developed to support modular load-bearing systems, integrate communication equipment, and optimize weight distribution for mobility and endurance. As global defense establishments reorient toward multi-domain combat readiness, equipping infantry with next-generation protective gear has become a priority. Whether facing insurgents in counter-terror operations or engaging in conventional battlefield scenarios, soldiers increasingly depend on advanced body armor as part of a comprehensive force protection strategy.

Technology Impact in Bullet Proof Vests Market:

Technological innovation is significantly reshaping the design, materials, and functionality of modern military bulletproof vests. The transition from traditional Kevlar to ultra-high-molecular-weight polyethylene (UHMWPE) and carbon nanomaterials has allowed for lighter, stronger, and more flexible armor systems. These materials offer equal or better ballistic protection at a fraction of the weight, reducing fatigue and increasing operational endurance for soldiers in the field. Composite ceramics-such as silicon carbide and boron carbide-are being refined for use in hard armor plates, capable of defeating armor-piercing rounds with minimal spall and trauma. These ceramic strike faces, combined with advanced backing layers, are enabling vests to meet Level III and IV protection standards while remaining ergonomic and scalable.

Beyond materials, the integration of wearable electronics and sensors is enhancing the utility of bulletproof vests. Some military forces are now deploying smart vests equipped with vital signs monitors, GPS locators, and communication modules that interface directly with command systems. These wearable tech systems allow for real-time health tracking and situational awareness, improving response time in casualty evacuation and medical triage. Thermal regulation technologies are also making their way into vest design. Innovations such as phase-change materials and passive ventilation systems help dissipate heat buildup, which is critical in hot operational environments. Similarly, ergonomic enhancements, such as load-bearing exoskeleton interfaces and modular weight balancing, are enabling longer wear time and improved comfort.

Another transformative area is the advent of adaptive and scalable armor systems. Vests can now be configured with detachable panels or upgraded plates based on mission risk assessments-allowing for dynamic threat adaptation. Some designs even incorporate liquid armor technologies, where shear-thickening fluids harden instantly upon impact, offering a flexible solution that conforms to the user's movements while maintaining protection.

Key Drivers in Bullet Proof Vests Market:

Multiple strategic, operational, and geopolitical factors are driving the increasing demand and evolution of military bulletproof vests globally.

Rising global conflicts and urban warfare have made personal protection indispensable. From Eastern Europe to the Middle East and parts of Africa, the resurgence of conventional warfare and insurgency has placed frontline troops in high-risk environments where small arms and explosive threats are prevalent. Military planners are thus prioritizing the widespread distribution of high-performance body armor. Modernization and soldier lethality programs are another key driver. Nations across the globe are investing in next-gen infantry programs-such as the U.S. Army's Soldier Protection System (SPS), France's FELIN, and India's F-INSAS-where bulletproof vests are central to modular combat loadouts. These programs aim to equip soldiers with integrated, high-mobility armor systems that also support technology enhancements and mission customizability.

Evolving threat profiles-including the use of armor-piercing ammunition by both state and non-state actors-are pushing militaries to upgrade protection standards. Conventional soft armor is no longer sufficient in many operational contexts, prompting the adoption of hybrid vest systems that combine both soft and hard armor components. Troop deployments and peacekeeping operations have also created demand for lightweight, scalable vests. Forces operating in foreign theaters, often in humanitarian or stabilization missions, require gear that provides sufficient protection without the heavy burden of full combat kits. This has led to growing procurement of adaptable vests with modular protection zones.

In addition, heightened emphasis on soldier survivability-not only from ballistic threats but also from secondary injuries like blunt trauma, blast overpressure, and heat stress-has driven R&D investment in ergonomic and physiological protection features. Finally, industrial innovation and defense collaboration are influencing supply chain dynamics. Partnerships between military organizations and advanced material science firms are accelerating the pace of vest development, while cross-border collaborations are facilitating technology transfer and joint manufacturing.

Regional Trends in Bullet Proof Vests Market:

The United States remains a global leader in military body armor development and deployment. Its large-scale modernization programs, such as the U.S. Army's Integrated Visual Augmentation System (IVAS) and the Enhanced Small Arms Protective Insert (ESAPI), reflect a continued push for lighter, modular, and mission-adaptable vests. Additionally, the U.S. is exploring "invisible armor" solutions-concealable yet highly protective vests for special operations and intelligence units. Canada, too, is focused on improving troop survivability with body armor optimized for cold-weather and Arctic European militaries are investing in advanced body armor as part of NATO interoperability goals and national defense upgrades. Germany, France, and the UK are deploying scalable systems with enhanced trauma protection, while Eastern European nations like Poland and the Baltic states are rapidly upgrading their infantry gear in response to regional tensions. Europe's defense industry is also developing sustainable and recyclable ballistic materials in line with EU environmental mandates.

Asia-Pacific represents a rapidly expanding market for military bulletproof vests. China is aggressively developing next-generation armor for its expanding military forces, integrating smart textiles and anti-trauma designs into standard-issue gear. India is investing in indigenous manufacturing of lightweight vests suitable for high-altitude operations, particularly along its northern borders. Japan and South Korea are modernizing their personal protection equipment to support alliance operations and counter regional threats. Ongoing conflicts, asymmetric warfare, and border security concerns are driving adoption in the Middle East. Israel continues to lead in lightweight, high-performance armor solutions, while nations like Saudi Arabia and the UAE are procuring vests for conventional forces and internal security units alike. The region is also seeing increased private-sector participation in defense equipment production, with bulletproof vest manufacturing being localized to reduce dependency on imports.

In Africa, the focus is on equipping troops for counterinsurgency, border patrol, and peacekeeping roles. Budget limitations challenge widespread deployment of high-end vests, but nations like Nigeria, Egypt, and Kenya are investing in protective gear through international defense aid, UN programs, and bilateral military partnerships. Lightweight, climate-adapted vests that balance affordability and protection are gaining popularity across the continent. Latin American countries, particularly Brazil, Colombia, and Mexico, are using bulletproof vests in both military and paramilitary operations. These include anti-narcotics campaigns and domestic counter-terrorism. The emphasis is on low-profile, multi-role vests that can be worn across various terrains-from jungles to urban zones-while offering protection against both ballistic threats and edged weapons.

Key Bullet Proof Vests Program:

The Ministry of Defence has signed a ₹639 crore contract for the procurement of 1.86 lakh indigenously developed bulletproof jackets for the Indian Army. The agreement, finalized on with a domestic defense manufacturer, is expected to significantly boost the government's 'Make in India' initiative by promoting local defense production. These advanced bulletproof jackets will enhance the protection of army personnel while underscoring the nation's commitment to self-reliance in defense manufacturing.

Table of Contents

Global Bullet Proof Vest Market Report Definition

Global Bullet Proof Vest Market Segmentation

By Type

By Region

By End User

Global Bullet Proof Vest Market Analysis for next 10 Years

The 10-year Global Bullet Proof Vest Market analysis would give a detailed overview of (market name) growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Bullet Proof Vest Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Bullet Proof Vest Market Forecast

The 10-year Global Bullet Proof Vest Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Bullet Proof Vest Market Trends & Forecast

The regional Bullet Proof Vest Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Bullet Proof Vest Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Bullet Proof Vest Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Bullet Proof Vest Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By End User, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Bullet Proof Vests Market Forecast, 2025-2035

- Figure 2: Global Bullet Proof Vests Market Forecast, By Region, 2025-2035

- Figure 3: Global Bullet Proof Vests Market Forecast, By End User, 2025-2035

- Figure 4: Global Bullet Proof Vests Market Forecast, By Type, 2025-2035

- Figure 5: North America, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 6: Europe, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 8: APAC, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 9: South America, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 10: United States, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 11: United States, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 12: Canada, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 14: Italy, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 16: France, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 17: France, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 18: Germany, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 24: Spain, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 30: Australia, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 32: India, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 33: India, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 34: China, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 35: China, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 40: Japan, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Bullet Proof Vests Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Bullet Proof Vests Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Bullet Proof Vests Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Bullet Proof Vests Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Bullet Proof Vests Market, By End User (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Bullet Proof Vests Market, By End User (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Bullet Proof Vests Market, By Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Bullet Proof Vests Market, By Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Bullet Proof Vests Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Bullet Proof Vests Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Bullet Proof Vests Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Bullet Proof Vests Market, By Region, 2025-2035

- Figure 58: Scenario 1, Bullet Proof Vests Market, By End User, 2025-2035

- Figure 59: Scenario 1, Bullet Proof Vests Market, By Type, 2025-2035

- Figure 60: Scenario 2, Bullet Proof Vests Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Bullet Proof Vests Market, By Region, 2025-2035

- Figure 62: Scenario 2, Bullet Proof Vests Market, By End User, 2025-2035

- Figure 63: Scenario 2, Bullet Proof Vests Market, By Type, 2025-2035

- Figure 64: Company Benchmark, Bullet Proof Vests Market, 2025-2035