|

市場調查報告書

商品編碼

1706588

軍事通訊的全球市場:2025年~2035年Global Military Communication Market 2025-2035 |

||||||

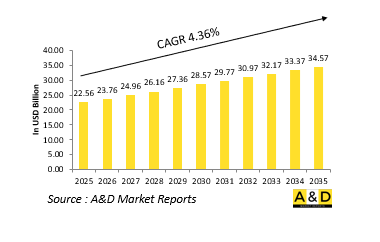

到 2025 年,全球軍事通訊市場價值估計將達到 225.6 億美元。預計到 2035 年,該市場將成長到 345.7 億美元,複合年增長率為 4.36%。

軍事通訊市場簡介:

軍事通訊系統是現代戰場指揮與控制(C2)的命脈。這些系統能夠在陸地、海洋、空中、太空和網路空間等多個領域的部隊之間安全、快速、可靠地交換資料、語音、視訊和影像。從衛星上行鏈路和戰術無線電到安全的網路協定和戰場訊息平台,軍事通訊是將決策者、戰鬥人員和支援部隊聯繫成一支有凝聚力的戰鬥力量的紐帶。從歷史上看,軍事通訊已經從旗幟訊號和有線電報發展到高度加密的網路和數位傳輸系統。當今的策略環境強調跨多個平台和聯盟夥伴的互通性、彈性和即時連接性。無論是協調空襲、導航無人系統或監控網路防禦,通訊能力現在都與武器系統本身一樣決定著作戰的有效性。隨著威脅變得更加分散和多維,對手的範圍從近乎對等到不對稱,軍隊越來越需要維護能夠在整個電磁頻譜和網路漏洞區域運作的強大、適應性強的通訊網路。網路中心戰、聯合部隊理論和多領域作戰的日益普及,正在將軍事通訊從戰術支援功能提升為國防戰略的核心支柱。

科技對軍事通訊市場的影響:

最近的技術進步已將軍事通訊轉變為一個高度靈活、智慧、以數據為中心的領域。最具顛覆性的變化之一是向軟體定義無線電(SDR)的轉變。這些無線電用可以動態切換頻率、調製類型和加密協定的靈活軟體取代了依賴硬體的通訊系統。即使使用不同的系統或在頻段限制下操作,SDR 也能使各單位實現互連,從而增強任務適應性。

5G 和邊緣運算正在成為實現低延遲、高頻寬資料交換的關鍵技術。這些技術能夠在密集環境中實現即時數據融合和傳輸,為從無人機即時饋送到擴增實境 (AR) 戰鬥覆蓋和支援物聯網的物流追蹤的一切提供支援。 5G與邊緣處理的結合將減少對集中指揮中心的依賴,使前線部隊能夠獨立處理資料和行動。另一項突破性進展是低地球軌道 (LEO) 衛星星座的整合,這將重新定義安全的全球覆蓋和冗餘。與傳統的地球靜止衛星不同,Starlink 和 OneWeb 部署的低地球軌道 (LEO) 網路具有更低的延遲、更快的資料吞吐量以及更好的極地和偏遠地區覆蓋範圍。各國軍隊正在快速探索低地球軌道 (LEO) 集成,以在點對點衝突場景中實現不間斷的 C2。

人工智慧 (AI) 對軍事通訊的影響怎麼強調也不為過。現在,人工智慧系統正被用於優化頻寬使用、偵測通訊模式中的異常,甚至跨語言和加密方法自動進行訊息翻譯。智慧通訊路由確保資料以最快、最安全的路徑傳輸,最大限度地減少漏洞。此外,量子通訊和後量子密碼學正在探索不受傳統網路竊聽影響的超安全通訊管道。雖然這些尖端技術仍處於早期階段,但國防官員正在投入巨資,為即將到來的量子運算威脅做好準備。同時,網路安全技術正直接融入通訊架構中。端對端加密、零信任框架和動態存取控制對於維護操作安全至關重要。隨著軍事網路面臨來自國家和非國家行為者日益嚴重的網路威脅,安全通訊管道已成為關鍵技術領域。

軍事通訊市場的關鍵推動因素:

多種戰略和營運因素正在推動全球軍事通訊系統的發展和擴張。其中最主要的是需要無縫多域操作。現代戰爭需要陸、海、空、天和網路部隊之間的協調,通常是即時的。通訊網路必須支援這些領域的同步努力,以確保任務成功。聯合作戰和合成作戰的興起也是一個主要推動因素。大多數現代軍事行動都涉及多國部隊,並需要跨越不同系統和理論的互通性。為此,北約的聯邦任務網絡(FMN)等標準化協議已經開發出來,以支援盟軍之間的資料共享和安全通訊。

另一個重要因素是戰場資產日益複雜。無人系統、感測器和武器平台會產生大量數據,從而推動對能夠在戰術邊緣移動、處理和解釋資訊的快速、安全的數據管道的需求。這也推動了人們對網狀網路和智慧頻寬管理的興趣。態勢感知和快速決策的需求變得越來越大。指揮官現在需要來自多個感測器、部隊追蹤器和 ISR 平台的即時資訊來做出明智的決策。這迫使通訊系統優先考慮資料融合、即時分析和壓力下的復原能力。

此外,電子戰 (EW) 和網路攻擊的威脅日益增加也影響著通訊策略。目前,對手利用幹擾、欺騙和駭客技術來破壞或削弱軍事網路的通訊。這就是為什麼對抗干擾技術、頻率捷變和網路強化傳輸協議的投資不斷增加的原因。預算考慮也起著一定作用。許多國家都在平衡對尖端通訊系統的需求與降低生命週期成本和減少對專有平台的依賴的壓力。這推動了開放標準、模組化升級和可用於軍事加固的商用現貨 (COTS) 組件的採用。

軍事通訊市場的區域趨勢:

全球軍事通訊格局由地區防禦優先事項、威脅認知和技術能力決定。

在北美,尤其是美國,人們非常重視透過統一、有彈性的通訊架構來實現全領域優勢。聯合全局指揮與控制(JADC2)等項目旨在透過人工智慧資料共享和安全通訊整合跨領域的力量。美國軍方正大力投資低地球軌道衛星網路、頻譜管理和人工智慧驅動的網路安全,以確保相對於當代競爭對手的戰略優勢。加拿大也在升級其通訊基礎設施,以提高與美國和北約部隊的互通性,特別是在北極和海上領域。歐洲致力於提高北約成員國之間的互通性並對遺留系統進行現代化改造。歐洲安全軟體定義無線電(ESSOR)項目和泛歐軍事衛星通訊能力的發展等措施反映了這一趨勢。法國、德國和英國在戰術通訊、戰場網路和主權衛星能力的投資方面處於領先地位。此外,烏克蘭衝突促使許多國家加速部署安全通訊系統,為電子戰做好準備。在亞太地區,地區緊張局勢和軍事現代化計劃正在刺激通訊技術的快速發展。為了確保作戰的連續性,中國正在推行自己的網路彈性通訊系統,該系統整合了衛星、地面和高頻(HF)頻道。作為其現代化計畫的一部分,印度正在投資網路中心戰和基於衛星的指揮與控制系統,其中包括國防太空總署的努力。日本和韓國正在加強戰場通訊基礎設施,以遏制地區威脅並支持美國主導的聯合行動。

主要軍事通信項目:

2025 年 2 月 20 日,國防部與班加羅爾的印度電子有限公司 (BEL) 簽署合同,為印度海岸防衛隊採購 149 台軟體定義無線電 (SDR)。價格為 12,212 千萬盧比,屬於採購(印度-IDDM)類別。這些先進的軟體無線電旨在提供安全、高速的數據和語音通信,以增強資訊共享、營運協調和態勢感知。這些整合將使印度海岸防衛隊顯著增強其在海上執法、搜救、漁業保護和海洋環境保護等關鍵任務領域的能力。該無線電也將增強聯合行動期間與印度海軍的互通性。該舉措是提高海岸防衛隊作戰準備的戰略舉措,同時也透過加強海上安全來支持印度政府的藍色經濟目標。依照 "自力更生印度" 的願景,該計畫也將促進本土軍用級通訊技術能力的發展,促進本土製造業,創造就業機會,促進國防部門的技能發展。

全球領先的衛星網路技術和服務供應商吉拉特衛星網路有限公司宣布,其國防部門贏得了一份價值 600 萬美元的訂單,為亞太地區的軍事組織提供 SkyEdge II-c 平台。這種先進的衛星通訊解決方案將支援固定和移動操作,為關鍵的國防任務提供安全可靠的連接,同時增強空中介面層級的網路保護。

本報告提供全球軍事通訊市場相關調查,彙整10年的各分類市場預測,技術趨勢,機會分析,企業簡介,各國資料等資訊。

目錄

軍事通訊市場報告定義

軍事通訊市場區隔

各地區

各零件

各終端用戶

未來 10 年軍事通訊市場分析

本章對十多年來軍事通訊市場的分析提供了軍事通訊市場成長、變化趨勢、技術採用概況和市場吸引力的詳細概述。

軍事通訊市場的市場技術

本部分涵蓋預計將影響該市場的十大技術以及這些技術可能對整個市場產生的影響。

全球軍事通訊市場預測

針對該市場未來 10 年的軍事通訊市場預測,已詳細列出上述各部分。

區域軍事通訊市場趨勢與預測

本部分涵蓋區域軍事通訊市場趨勢、推動因素、阻礙因素、課題以及政治、經濟、社會和技術方面。它還提供了詳細的區域市場預測和情境分析。區域分析包括主要公司概況、供應商格局和公司基準測試。目前市場規模是根據正常業務情境估算的。

北美

促進因素,阻礙因素,課題

PEST

市場預測與情勢分析

主要企業

供應商階層的形勢

企業基準

歐洲

中東

亞太地區

南美

軍事通訊市場國家分析

本章重點介紹該市場的主要防禦計劃,並介紹該市場的最新新聞和專利。它還提供國家級的 10 年市場預測和情境分析。

美國

防衛計劃

最新消息

專利

這個市場上目前技術成熟度

市場預測與情勢分析

加拿大

義大利

法國

德國

荷蘭

比利時

西班牙

瑞典

希臘

澳洲

南非

印度

中國

俄羅斯

韓國

日本

馬來西亞

新加坡

巴西

軍事通訊市場機會矩陣

軍事通訊市場報告相關專家的意見

結論

關於航空·國防市場報告

The Global Military Communication market is estimated at USD 22.56 billion in 2025, projected to grow to USD 34.57 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 4.36% over the forecast period 2025-2035.

Introduction to Military Communication Market:

Military communication systems are the lifelines of command and control (C2) on the modern battlefield. These systems enable the secure, rapid, and reliable exchange of data, voice, video, and imagery between forces across different domains-land, sea, air, space, and cyberspace. From satellite uplinks and tactical radios to secure internet protocols and battlefield messaging platforms, military communication is the connective tissue that links decision-makers, combat units, and support elements into a cohesive fighting force. Historically, military communication evolved from flag signals and wire-based telegraphy to sophisticated encrypted networks and digital transmission systems. In the current strategic environment, the emphasis is on interoperability, resilience, and real-time connectivity across multiple platforms and coalition partners. Whether coordinating airstrikes, navigating unmanned systems, or monitoring cyber defense, communication capabilities now determine operational effectiveness as much as weapon systems themselves. As threats become more dispersed and multidimensional-from near-peer adversaries to asymmetric actors-military forces are under increasing pressure to maintain robust, adaptive communication networks that function across contested electromagnetic spectrums and cyber-compromised zones. The growing adoption of network-centric warfare, joint-force doctrines, and multi-domain operations has elevated military communication from a tactical support function to a core pillar of defense strategy.

Technology Impact in Military Communication Market:

Recent technological advancements have transformed military communication into a highly agile, intelligent, and data-centric domain. One of the most disruptive changes is the shift toward Software-Defined Radios (SDRs). These radios replace hardware-dependent communication systems with flexible software that can dynamically switch frequencies, modulation types, and encryption protocols. SDRs allow units to interconnect even when using different systems or operating under spectrum constraints, boosting mission adaptability.

5G and edge computing are emerging as significant enablers of low-latency, high-bandwidth data exchange. These technologies allow for real-time data fusion and transmission in dense environments, enabling everything from live drone feeds to augmented reality (AR) combat overlays and IoT-enabled logistics tracking. The combination of 5G and edge processing reduces reliance on centralized command centers and allows frontline units to process and act on data independently. Another game-changing development is the integration of Low Earth Orbit (LEO) satellite constellations, which are redefining secure global coverage and redundancy. Unlike traditional geostationary satellites, LEO networks-such as those deployed by Starlink and OneWeb-offer lower latency, faster data throughput, and improved coverage in polar and remote regions. Militaries are rapidly exploring LEO integration for uninterrupted C2 during peer conflict scenarios.

The impact of Artificial Intelligence (AI) in military communication cannot be overstated. AI-powered systems are now used to optimize bandwidth usage, detect anomalies in communication patterns, and even automate message translation across languages and encryption schemes. Intelligent communication routing ensures that data takes the fastest, most secure path, minimizing vulnerabilities. Additionally, Quantum communication and post-quantum encryption are being explored for ultra-secure channels immune to conventional cyber interception. These cutting-edge technologies are still in their nascent stages but are attracting significant investment as defense establishments prepare for the advent of quantum computing threats. Meanwhile, cybersecurity technologies are being built directly into communication architectures. End-to-end encryption, zero-trust frameworks, and dynamic access controls are vital for maintaining operational security. As military networks face increasing cyber threats from state and non-state actors, secure communication channels have become a critical area of technological focus.

Key Drivers in Military Communication Market:

Several strategic and operational factors are propelling the evolution and expansion of global military communication systems. Chief among them is the need for seamless multi-domain operations. Modern warfare demands coordination between land, sea, air, space, and cyber forces-often in real time. Communication networks must support synchronized efforts across these domains to ensure mission success. The rise of joint and coalition operations is another major driver. Most modern military engagements involve multi-national forces, requiring interoperability across disparate systems and doctrines. This has led to the development of standardized protocols like NATO's Federated Mission Networking (FMN), which supports data sharing and secure communications among allied forces.

Another important factor is the increasing complexity of battlefield assets. With unmanned systems, sensors, and weapon platforms generating vast amounts of data, there is a growing demand for high-speed, secure data pipelines that can move, process, and interpret information at the tactical edge. This has also driven interest in mesh networking and intelligent bandwidth management. Situational awareness and rapid decision-making are further amplifying demand. Commanders now require live feeds from multiple sensors, troop trackers, and ISR platforms to make informed decisions. This pushes communication systems to prioritize data fusion, real-time analytics, and resilience under pressure.

Moreover, the growing threat from electronic warfare (EW) and cyber-attacks is influencing communication strategies. Adversaries now target military networks with jamming, spoofing, and hacking techniques to disrupt or degrade communications. This has led to increased investment in anti-jamming technologies, frequency agility, and cyber-hardened transmission protocols. Budgetary considerations also play a role. Many nations are balancing the need for cutting-edge communication systems with pressure to reduce lifecycle costs and minimize dependence on proprietary platforms. This drives the adoption of open standards, modular upgrades, and commercial off-the-shelf (COTS) components that can be ruggedized for military use.

Regional Trends in Military Communication Market:

The global military communication landscape is shaped by regional defense priorities, threat perceptions, and technological capabilities.

In North America, particularly the United States, the focus is on achieving full-spectrum dominance through resilient and unified communication architectures. Programs like the Joint All-Domain Command and Control (JADC2) aim to integrate forces across domains via AI-powered data sharing and secure communications. The U.S. military is heavily investing in LEO satellite networks, spectrum management, and AI-driven cybersecurity to ensure strategic edge over peer rivals. Canada is similarly upgrading its communication infrastructure for interoperability with U.S. and NATO forces, especially in Arctic and maritime domains. Europe is concentrating on enhancing interoperability among NATO members and modernizing legacy systems. Initiatives like the European Secure Software Defined Radio (ESSOR) project and the development of pan-European military satcom capabilities reflect this trend. France, Germany, and the UK are leading the charge with investments in tactical communications, battlefield networking, and sovereign satellite capabilities. The war in Ukraine has also prompted many countries to accelerate secure communication deployments to guard against electronic warfare. In Asia-Pacific, regional tensions and military modernization programs are fueling rapid advances in communication technologies. China is pursuing indigenous, cyber-resilient communication systems with integrated satellite, terrestrial, and HF (high frequency) channels to ensure operational continuity. India is investing in network-centric warfare and satellite-based C2 systems as part of its modernization initiatives, including the Defense Space Agency's efforts. Japan and South Korea are enhancing their battlefield communication infrastructure to deter regional threats and support U.S.-led joint operations.

Key Military Communication Program:

On February 20, 2025, the Ministry of Defence signed a contract with Bharat Electronics Limited (BEL), Bengaluru, for the procurement of 149 Software Defined Radios (SDRs) for the Indian Coast Guard. Valued at ₹1,220.12 crore, the acquisition falls under the Buy (Indian-IDDM) category. These advanced SDRs are designed to provide secure, high-speed data and voice communication, enhancing information sharing, operational coordination, and situational awareness. Their integration will significantly boost the Indian Coast Guard's capabilities in key mission areas such as maritime law enforcement, search and rescue, fisheries protection, and marine environmental safeguarding. The radios will also improve interoperability with the Indian Navy during joint operations. This initiative represents a strategic move to enhance the Coast Guard's operational readiness while supporting the Government of India's Blue Economy goals by strengthening maritime security. In line with the Atmanirbhar Bharat vision, the project will also contribute to the development of indigenous capabilities in military-grade communication technologies, promote local manufacturing, create employment opportunities, and foster skill development in the defense sector.

Gilat Satellite Networks Ltd, a global leader in satellite networking technologies and services, has announced that its Defense Division has secured a $6 million order to supply its SkyEdge II-c platform to a military organization in the Asia-Pacific region. The advanced satellite communications solution will support both stationary and mobile operations, delivering secure and reliable connectivity for critical defense missions, with enhanced cyber protection at the air interface level.

Table of Contents

Military Communication Market Report Definition

Military Communication Market Segmentation

By Region

By Component

By End-User

Military Communication Market Analysis for next 10 Years

The 10-year Military Communication Market analysis would give a detailed overview of Military Communication Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Military Communication Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Military Communication Market Forecast

The 10-year Military Communication Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Military Communication Market Trends & Forecast

The regional Military Communication Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Military Communication Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Military Communication Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Military Communication Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By End User, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Type, 2025-2035

List of Figures

- Figure 1: Global Military Communication Market Forecast, 2025-2035

- Figure 2: Global Military Communication Market Forecast, By Region, 2025-2035

- Figure 3: Global Military Communication Market Forecast, By End User, 2025-2035

- Figure 4: Global Military Communication Market Forecast, By Type, 2025-2035

- Figure 5: North America, Military Communication Market, Market Forecast, 2025-2035

- Figure 6: Europe, Military Communication Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Military Communication Market, Market Forecast, 2025-2035

- Figure 8: APAC, Military Communication Market, Market Forecast, 2025-2035

- Figure 9: South America, Military Communication Market, Market Forecast, 2025-2035

- Figure 10: United States, Military Communication Market, Technology Maturation, 2025-2035

- Figure 11: United States, Military Communication Market, Market Forecast, 2025-2035

- Figure 12: Canada, Military Communication Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Military Communication Market, Market Forecast, 2025-2035

- Figure 14: Italy, Military Communication Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Military Communication Market, Market Forecast, 2025-2035

- Figure 16: France, Military Communication Market, Technology Maturation, 2025-2035

- Figure 17: France, Military Communication Market, Market Forecast, 2025-2035

- Figure 18: Germany, Military Communication Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Military Communication Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Military Communication Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Military Communication Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Military Communication Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Military Communication Market, Market Forecast, 2025-2035

- Figure 24: Spain, Military Communication Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Military Communication Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Military Communication Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Military Communication Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Military Communication Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Military Communication Market, Market Forecast, 2025-2035

- Figure 30: Australia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Military Communication Market, Market Forecast, 2025-2035

- Figure 32: India, Military Communication Market, Technology Maturation, 2025-2035

- Figure 33: India, Military Communication Market, Market Forecast, 2025-2035

- Figure 34: China, Military Communication Market, Technology Maturation, 2025-2035

- Figure 35: China, Military Communication Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Military Communication Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Military Communication Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Military Communication Market, Market Forecast, 2025-2035

- Figure 40: Japan, Military Communication Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Military Communication Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Military Communication Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Military Communication Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Military Communication Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Military Communication Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Military Communication Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Military Communication Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Military Communication Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Military Communication Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Military Communication Market, By End User (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Military Communication Market, By End User (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Military Communication Market, By Type (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Military Communication Market, By Type (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Military Communication Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Military Communication Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Military Communication Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Military Communication Market, By Region, 2025-2035

- Figure 58: Scenario 1, Military Communication Market, By End User, 2025-2035

- Figure 59: Scenario 1, Military Communication Market, By Type, 2025-2035

- Figure 60: Scenario 2, Military Communication Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Military Communication Market, By Region, 2025-2035

- Figure 62: Scenario 2, Military Communication Market, By End User, 2025-2035

- Figure 63: Scenario 2, Military Communication Market, By Type, 2025-2035

- Figure 64: Company Benchmark, Military Communication Market, 2025-2035

國防通訊系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類軍用飛機通訊航空電子設備市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署和最終用戶分類

國防通訊系統市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶、模組及功能分類軍用飛機通訊航空電子設備市場分析及預測(至2035年):按類型、產品、服務、技術、組件、應用、設備、部署和最終用戶分類 軍事通訊市場-全球產業規模、佔有率、趨勢、機會、預測:組件、技術、平台、應用、區域和競爭格局(2021-2031年)

軍事通訊市場-全球產業規模、佔有率、趨勢、機會、預測:組件、技術、平台、應用、區域和競爭格局(2021-2031年) 全球國防加固通訊市場(2026-2036)

全球國防加固通訊市場(2026-2036) 軍事通訊市場規模、佔有率和成長分析(按組件、通訊類型、應用、最終用戶和地區分類)-2026-2033年產業預測軍用飛機通訊航空電子設備市場-全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、組件、應用、地區和競爭格局分類,2020-2030年預測

軍事通訊市場規模、佔有率和成長分析(按組件、通訊類型、應用、最終用戶和地區分類)-2026-2033年產業預測軍用飛機通訊航空電子設備市場-全球產業規模、佔有率、趨勢、機會和預測,按飛機類型、組件、應用、地區和競爭格局分類,2020-2030年預測 軍事通訊市場(按產品類型、平台類型和應用)—2025-2032 年全球預測

軍事通訊市場(按產品類型、平台類型和應用)—2025-2032 年全球預測 軍事通訊市場(按通訊類型、組件和地區分類)

軍事通訊市場(按通訊類型、組件和地區分類) 軍事衛星通訊:基礎設施開發(2000年~2035年)

軍事衛星通訊:基礎設施開發(2000年~2035年) 2025-2029年全球軍事通訊市場

2025-2029年全球軍事通訊市場