|

市場調查報告書

商品編碼

1344514

電池材料回收市場:各材料類型,各最終用途:全球機會分析與產業預測,2023-2032年Battery Materials Recycling Market By Material Type, By End-Use: Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

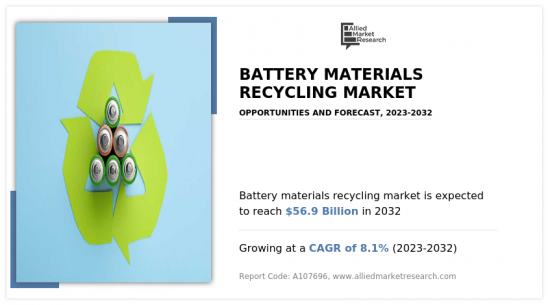

2022年電池材料回收市場價值為263億美元,預計2023年至2032年複合年增長率為8.1%,到2032年達到569億美元。

電池回收是從廢棄電池中提取有價值的材料並重新利用的過程。涉及收集、整理、拆解、提煉等幾個過程。收集到的電池根據化學成分、尺寸和類型進行分類,以促進回收過程。拆卸涉及分離電池的各種組件,包括外殼、電極、電解質和其他材料。這些部件採用機械、火法冶金和濕式冶金製程等各種技術來提取鋰、鈷、鎳和鉛等有價值的金屬。回收的金屬可用於製造新電池和其他工業用途。

電池回收在包括家電在內的各個領域中發揮著重要作用。隨著智慧型手機、筆記型電腦和平板電腦等電子設備使用的增加,對電池的需求不斷增加。透過回收這些設備中的電池,可以回收有價值的材料並減少處置對環境的影響。還確保對電池中的有害物質(例如鉛和汞)進行適當控制,這些物質可能對人類健康和環境產生負面影響。

太陽能和風能等再生能源系統依靠電池來儲存多餘的能量以供以後使用。這些電池被稱為儲能係統,在穩定電網和實現間歇性再生能源的順利併網方面發揮關鍵作用。回收能源儲存系統中使用的電池有助於回收有價值的材料並減少與其生產和處置相關的環境影響。還透過閉環和最大限度地減少資源消耗來促進再生能源的永續發展。

目錄

第1章 簡介

第2章 摘要整理

第3章 市場概要

- 市場定義和範圍

- 主要調查結果

- 影響要素

- 主要的投資機會

- 波特的五力分析

- 市場動態

- 促進因素

- 電動車對再生電池材料的需求不斷增加

- 電子廢棄物管理與循環供應鏈

- 抑制因素

- 電池材料的回收過程複雜且成本高昂。

- 機會

- 環境保護的實施

- 促進因素

- COVID-19對市場的影響分析

- 價值鏈分析

- 主要法規分析

第4章 電池材料回收市場:各材料類型

- 概要

- 鋰

- 鈷

- 鐵

- 錳

- 鎳

- 鉛

- 其他

第5章 電池材料回收市場:各最終用途

- 概要

- 汽車

- 建築·建設

- 航太·防衛

- 纖維

- 其他

第6章 電池材料回收市場:各地區

- 概要

- 北美

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 其他歐洲

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太地區

- 南美·中東·非洲

- 巴西

- 沙烏地阿拉伯

- 南非

- 其他地區

第7章 競爭情形

- 簡介

- 主要成功策略

- 主要十大公司的產品製圖

- 競爭儀表板

- 競爭熱圖

- 主要企業的定位,2022年

第8章 企業簡介

- Eco-Bat Technologies

- GEM Co., Ltd.

- Li-Cycle

- Gravita India Limited

- RecycLiCo Battery Materials Inc.

- Redux GmbH

- Gopher Resource

- Umicore N.V.

- Redwood Materials Inc.

- Cirba Solutions

According to a new report published by Allied Market Research, titled, "Battery Materials Recycling Market," The battery materials recycling market was valued at $26.3 billion in 2022, and is estimated to reach $56.9 billion by 2032, growing at a CAGR of 8.1% from 2023 to 2032.

Battery recycling is the process of extracting and reusing valuable materials from used batteries. It involves several steps, including collection, sorting, dismantling, and refining. The collected batteries are sorted based on their chemistry, size, and type to facilitate the recycling process. Dismantling is carried out to separate different components of the battery, such as the casing, electrodes, electrolytes, and other materials. These components are then subjected to various techniques, such as mechanical processes, pyrometallurgical processes, and hydrometallurgical processes, to extract valuable metals such as lithium, cobalt, nickel, and lead. The recovered metals may be used to manufacture new batteries or for other industrial applications.

Battery recycling plays a crucial role in various domains, starting with consumer electronics. There is an increase in demand for batteries with the increase in use of electronic devices such as smartphones, laptops, and tablets. Recycling batteries from these devices helps in recovering valuable materials, thus reducing the environmental impact of their disposal. It also ensures proper management of hazardous substances present in batteries, such as lead and mercury, which may have detrimental effects on human health and the environment.

Renewable energy systems, such as solar and wind power, rely on batteries to store excess energy for later use. These batteries, often called energy storage systems, play a vital role in stabilizing the grid and enabling the smooth integration of intermittent renewable energy sources. Recycling the batteries used in energy storage systems helps recover valuable materials and reduces the environmental impact associated with their production and disposal. It also promotes the sustainable development of renewable energy by closing the loop and minimizing resource depletion.

The battery materials recycling market is segmented into material type, end-use industry, and regions. On the basis of material type, the market is categorized into lithium, cobalt, iron, manganese, nickel, lead, and others. On the basis of end-use industry, the market is divided into automotive, building and construction, aerospace & defense, textile, and others. Region-wise the market is studied across North America, Europe, Asia-Pacific, and LAMEA.

By material type, manganese is the fastest-growing segment of the battery materials recycling market in 2022. Manganese, a transition metal, possesses outstanding electrochemical properties, making it a highly sought-after option for the production of batteries. In rechargeable batteries, manganese is commonly utilized in the form of manganese oxide (MnO) or manganese dioxide (MnO2) as a cathode material. The implementation of manganese-based cathodes presents numerous benefits such as high energy density, reliable cycling stability, and cost-effectiveness in comparison to alternative cathode materials.

- To facilitate the sustainable use of manganese, recycling plays a crucial role. The recycling process entails the collection, disassembly, and treatment of batteries that have reached their end-of-life stage, with the aim of extracting valuable metals, including manganese. The recovered manganese can then undergo reprocessing and be reintroduced into the battery manufacturing supply chain, contributing to resource conservation and reducing the need for new manganese extraction.

By end-use industry, textile segment is the fastest growing segment of the battery materials recycling market in 2022. Battery recycling is a multi-step process that aims to recover valuable materials, one of which is polypropylene (PP). The initial stage involves the collection of batteries from different sources, such as electronic waste recycling centers and battery collection programs. By incorporating recycled polypropylene fibers into textile production, industry can make a significant contribution to resource conservation. This is achieved by reducing the need for new polypropylene, which is derived from fossil fuels. Through the utilization of recycled polypropylene, the textile industry actively participates in the circular economy, minimizing its dependence on non-renewable resources.

- On the basis of region, Asia-Pacific is the fastest growing region of the battery materials recycling market in 2022. The Asia-Pacific region has emerged as a prominent center for electric vehicle production and adoption, with countries like China, India, and Australia leading the way. These nations are actively investing in renewable energy sources like solar and wind power to support their growing electric vehicle industries. However, the development of renewable energy systems often relies on energy storage solutions, particularly lithium-ion batteries. Due to limited reserves of critical battery materials such as lithium and cobalt within the Asia-Pacific region, recycling has become a crucial strategy to ensure resource security and reduce dependence on imports.

- Recognizing the significance of sustainable battery management, China has taken significant strides in battery materials recycling. The country has implemented regulations that hold manufacturers accountable for recycling a certain percentage of the batteries they produce. Consequently, several recycling facilities have been established, specifically focusing on the extraction and recovery of valuable metals like lithium, cobalt, and nickel from spent batteries.

- The major players operating in the global battery materials recycling market include Cirba Solutions, Eco-Bat Technologies, GEM Co., Ltd., Gopher Resource, GRAVITA INDIA LIMITED, Li-Cycle, RecycLiCo Battery Materials Inc., Redux GmbH, Redwood Materials Inc., and Umicore N.V.

Key findings of the study:

- The report outlines the current battery materials recycling market trends and future scenario of the market from 2023 to 2032 to understand the prevailing opportunities and potential investment pockets.

- The battery materials recycling market size is provided in terms of revenue.

- By materials type, the lead segment was the highest revenue contributor in the global battery materials recycling market share in 2022.

- By end-use industry, the automotive sector emerged as the leading revenue generator in the market, in 2022.

- By region, Europe was the highest revenue contributor, accounting in 2022, with a CAGR of 7.8%.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the battery materials recycling market analysis from 2022 to 2032 to identify the prevailing battery materials recycling market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the battery materials recycling market growth which assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global battery materials recycling market forecast, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Material Type

- Nickle

- Lead

- Others

- Lithium

- Cobalt

- Iron

- Manganese

By End-Use

- Automotive

- Building and Construction

- Aerospace and Defense

- Textile

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- Cirba Solutions

- Eco-Bat Technologies

- GEM Co., Ltd.

- Gopher Resource

- Gravita India Limited

- Li-Cycle

- RecycLiCo Battery Materials Inc.

- Redux GmbH

- Redwood Materials Inc.

- Umicore N.V.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. High bargaining power of suppliers

- 3.3.2. High threat of new entrants

- 3.3.3. Moderate threat of substitutes

- 3.3.4. High intensity of rivalry

- 3.3.5. Moderate bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Increase in demand for recycled battery materials in electric vehicles

- 3.4.1.2. E-waste management and circular supply chains

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. Complex and costly process of recycling battery materials

- 3.4.3. Opportunities

- 3.4.3.1. Implementation of environmental protection

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Value Chain Analysis

- 3.7. Key Regulation Analysis

CHAPTER 4: BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Lithium

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Cobalt

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Iron

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Manganese

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

- 4.6. Nickle

- 4.6.1. Key market trends, growth factors and opportunities

- 4.6.2. Market size and forecast, by region

- 4.6.3. Market share analysis by country

- 4.7. Lead

- 4.7.1. Key market trends, growth factors and opportunities

- 4.7.2. Market size and forecast, by region

- 4.7.3. Market share analysis by country

- 4.8. Others

- 4.8.1. Key market trends, growth factors and opportunities

- 4.8.2. Market size and forecast, by region

- 4.8.3. Market share analysis by country

CHAPTER 5: BATTERY MATERIALS RECYCLING MARKET, BY END-USE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Automotive

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Building and Construction

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Aerospace and Defense

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Textile

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Others

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

CHAPTER 6: BATTERY MATERIALS RECYCLING MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key trends and opportunities

- 6.2.2. Market size and forecast, by Material Type

- 6.2.3. Market size and forecast, by End-Use

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Key market trends, growth factors and opportunities

- 6.2.4.1.2. Market size and forecast, by Material Type

- 6.2.4.1.3. Market size and forecast, by End-Use

- 6.2.4.2. Canada

- 6.2.4.2.1. Key market trends, growth factors and opportunities

- 6.2.4.2.2. Market size and forecast, by Material Type

- 6.2.4.2.3. Market size and forecast, by End-Use

- 6.2.4.3. Mexico

- 6.2.4.3.1. Key market trends, growth factors and opportunities

- 6.2.4.3.2. Market size and forecast, by Material Type

- 6.2.4.3.3. Market size and forecast, by End-Use

- 6.3. Europe

- 6.3.1. Key trends and opportunities

- 6.3.2. Market size and forecast, by Material Type

- 6.3.3. Market size and forecast, by End-Use

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. Germany

- 6.3.4.1.1. Key market trends, growth factors and opportunities

- 6.3.4.1.2. Market size and forecast, by Material Type

- 6.3.4.1.3. Market size and forecast, by End-Use

- 6.3.4.2. France

- 6.3.4.2.1. Key market trends, growth factors and opportunities

- 6.3.4.2.2. Market size and forecast, by Material Type

- 6.3.4.2.3. Market size and forecast, by End-Use

- 6.3.4.3. Italy

- 6.3.4.3.1. Key market trends, growth factors and opportunities

- 6.3.4.3.2. Market size and forecast, by Material Type

- 6.3.4.3.3. Market size and forecast, by End-Use

- 6.3.4.4. Spain

- 6.3.4.4.1. Key market trends, growth factors and opportunities

- 6.3.4.4.2. Market size and forecast, by Material Type

- 6.3.4.4.3. Market size and forecast, by End-Use

- 6.3.4.5. UK

- 6.3.4.5.1. Key market trends, growth factors and opportunities

- 6.3.4.5.2. Market size and forecast, by Material Type

- 6.3.4.5.3. Market size and forecast, by End-Use

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Key market trends, growth factors and opportunities

- 6.3.4.6.2. Market size and forecast, by Material Type

- 6.3.4.6.3. Market size and forecast, by End-Use

- 6.4. Asia-Pacific

- 6.4.1. Key trends and opportunities

- 6.4.2. Market size and forecast, by Material Type

- 6.4.3. Market size and forecast, by End-Use

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Key market trends, growth factors and opportunities

- 6.4.4.1.2. Market size and forecast, by Material Type

- 6.4.4.1.3. Market size and forecast, by End-Use

- 6.4.4.2. Japan

- 6.4.4.2.1. Key market trends, growth factors and opportunities

- 6.4.4.2.2. Market size and forecast, by Material Type

- 6.4.4.2.3. Market size and forecast, by End-Use

- 6.4.4.3. India

- 6.4.4.3.1. Key market trends, growth factors and opportunities

- 6.4.4.3.2. Market size and forecast, by Material Type

- 6.4.4.3.3. Market size and forecast, by End-Use

- 6.4.4.4. South Korea

- 6.4.4.4.1. Key market trends, growth factors and opportunities

- 6.4.4.4.2. Market size and forecast, by Material Type

- 6.4.4.4.3. Market size and forecast, by End-Use

- 6.4.4.5. Australia

- 6.4.4.5.1. Key market trends, growth factors and opportunities

- 6.4.4.5.2. Market size and forecast, by Material Type

- 6.4.4.5.3. Market size and forecast, by End-Use

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Key market trends, growth factors and opportunities

- 6.4.4.6.2. Market size and forecast, by Material Type

- 6.4.4.6.3. Market size and forecast, by End-Use

- 6.5. LAMEA

- 6.5.1. Key trends and opportunities

- 6.5.2. Market size and forecast, by Material Type

- 6.5.3. Market size and forecast, by End-Use

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Key market trends, growth factors and opportunities

- 6.5.4.1.2. Market size and forecast, by Material Type

- 6.5.4.1.3. Market size and forecast, by End-Use

- 6.5.4.2. Saudi Arabia

- 6.5.4.2.1. Key market trends, growth factors and opportunities

- 6.5.4.2.2. Market size and forecast, by Material Type

- 6.5.4.2.3. Market size and forecast, by End-Use

- 6.5.4.3. South Africa

- 6.5.4.3.1. Key market trends, growth factors and opportunities

- 6.5.4.3.2. Market size and forecast, by Material Type

- 6.5.4.3.3. Market size and forecast, by End-Use

- 6.5.4.4. Rest of LAMEA

- 6.5.4.4.1. Key market trends, growth factors and opportunities

- 6.5.4.4.2. Market size and forecast, by Material Type

- 6.5.4.4.3. Market size and forecast, by End-Use

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product Mapping of Top 10 Player

- 7.4. Competitive Dashboard

- 7.5. Competitive Heatmap

- 7.6. Top player positioning, 2022

CHAPTER 8: COMPANY PROFILES

- 8.1. Eco-Bat Technologies

- 8.1.1. Company overview

- 8.1.2. Key Executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.1.6. Key strategic moves and developments

- 8.2. GEM Co., Ltd.

- 8.2.1. Company overview

- 8.2.2. Key Executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.2.6. Business performance

- 8.2.7. Key strategic moves and developments

- 8.3. Li-Cycle

- 8.3.1. Company overview

- 8.3.2. Key Executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.3.6. Key strategic moves and developments

- 8.4. Gravita India Limited

- 8.4.1. Company overview

- 8.4.2. Key Executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.5. RecycLiCo Battery Materials Inc.

- 8.5.1. Company overview

- 8.5.2. Key Executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Key strategic moves and developments

- 8.6. Redux GmbH

- 8.6.1. Company overview

- 8.6.2. Key Executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.7. Gopher Resource

- 8.7.1. Company overview

- 8.7.2. Key Executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.8. Umicore N.V.

- 8.8.1. Company overview

- 8.8.2. Key Executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.8.6. Business performance

- 8.8.7. Key strategic moves and developments

- 8.9. Redwood Materials Inc.

- 8.9.1. Company overview

- 8.9.2. Key Executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.10. Cirba Solutions

- 8.10.1. Company overview

- 8.10.2. Key Executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

- 8.10.6. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 02. BATTERY MATERIALS RECYCLING MARKET FOR LITHIUM, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. BATTERY MATERIALS RECYCLING MARKET FOR COBALT, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. BATTERY MATERIALS RECYCLING MARKET FOR IRON, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. BATTERY MATERIALS RECYCLING MARKET FOR MANGANESE, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. BATTERY MATERIALS RECYCLING MARKET FOR NICKLE, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. BATTERY MATERIALS RECYCLING MARKET FOR LEAD, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. BATTERY MATERIALS RECYCLING MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. GLOBAL BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 10. BATTERY MATERIALS RECYCLING MARKET FOR AUTOMOTIVE, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. BATTERY MATERIALS RECYCLING MARKET FOR BUILDING AND CONSTRUCTION, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. BATTERY MATERIALS RECYCLING MARKET FOR AEROSPACE AND DEFENSE, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. BATTERY MATERIALS RECYCLING MARKET FOR TEXTILE, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. BATTERY MATERIALS RECYCLING MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. BATTERY MATERIALS RECYCLING MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA BATTERY MATERIALS RECYCLING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 19. U.S. BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 20. U.S. BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 21. CANADA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 22. CANADA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 23. MEXICO BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 24. MEXICO BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 25. EUROPE BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 26. EUROPE BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 27. EUROPE BATTERY MATERIALS RECYCLING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 28. GERMANY BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 29. GERMANY BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 30. FRANCE BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 31. FRANCE BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 32. ITALY BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 33. ITALY BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 34. SPAIN BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 35. SPAIN BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 36. UK BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 37. UK BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 38. REST OF EUROPE BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 39. REST OF EUROPE BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 40. ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 41. ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 42. ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 43. CHINA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 44. CHINA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 45. JAPAN BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 46. JAPAN BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 47. INDIA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 48. INDIA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 49. SOUTH KOREA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 50. SOUTH KOREA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 51. AUSTRALIA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 52. AUSTRALIA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 53. REST OF ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 54. REST OF ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 55. LAMEA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 56. LAMEA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 57. LAMEA BATTERY MATERIALS RECYCLING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 58. BRAZIL BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 59. BRAZIL BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 60. SAUDI ARABIA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 61. SAUDI ARABIA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 62. SOUTH AFRICA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 63. SOUTH AFRICA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 64. REST OF LAMEA BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022-2032 ($MILLION)

- TABLE 65. REST OF LAMEA BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022-2032 ($MILLION)

- TABLE 66. ECO-BAT TECHNOLOGIES: KEY EXECUTIVES

- TABLE 67. ECO-BAT TECHNOLOGIES: COMPANY SNAPSHOT

- TABLE 68. ECO-BAT TECHNOLOGIES: PRODUCT SEGMENTS

- TABLE 69. ECO-BAT TECHNOLOGIES: PRODUCT PORTFOLIO

- TABLE 70. ECO-BAT TECHNOLOGIES: KEY STRATERGIES

- TABLE 71. GEM CO., LTD.: KEY EXECUTIVES

- TABLE 72. GEM CO., LTD.: COMPANY SNAPSHOT

- TABLE 73. GEM CO., LTD.: PRODUCT SEGMENTS

- TABLE 74. GEM CO., LTD.: PRODUCT PORTFOLIO

- TABLE 75. GEM CO., LTD.: KEY STRATERGIES

- TABLE 76. LI-CYCLE: KEY EXECUTIVES

- TABLE 77. LI-CYCLE: COMPANY SNAPSHOT

- TABLE 78. LI-CYCLE: SERVICE SEGMENTS

- TABLE 79. LI-CYCLE: PRODUCT PORTFOLIO

- TABLE 80. LI-CYCLE: KEY STRATERGIES

- TABLE 81. GRAVITA INDIA LIMITED: KEY EXECUTIVES

- TABLE 82. GRAVITA INDIA LIMITED: COMPANY SNAPSHOT

- TABLE 83. GRAVITA INDIA LIMITED: PRODUCT SEGMENTS

- TABLE 84. GRAVITA INDIA LIMITED: PRODUCT PORTFOLIO

- TABLE 85. RECYCLICO BATTERY MATERIALS INC.: KEY EXECUTIVES

- TABLE 86. RECYCLICO BATTERY MATERIALS INC.: COMPANY SNAPSHOT

- TABLE 87. RECYCLICO BATTERY MATERIALS INC.: PRODUCT SEGMENTS

- TABLE 88. RECYCLICO BATTERY MATERIALS INC.: PRODUCT PORTFOLIO

- TABLE 89. RECYCLICO BATTERY MATERIALS INC.: KEY STRATERGIES

- TABLE 90. REDUX GMBH: KEY EXECUTIVES

- TABLE 91. REDUX GMBH: COMPANY SNAPSHOT

- TABLE 92. REDUX GMBH: PRODUCT SEGMENTS

- TABLE 93. REDUX GMBH: PRODUCT PORTFOLIO

- TABLE 94. GOPHER RESOURCE: KEY EXECUTIVES

- TABLE 95. GOPHER RESOURCE: COMPANY SNAPSHOT

- TABLE 96. GOPHER RESOURCE: SERVICE SEGMENTS

- TABLE 97. GOPHER RESOURCE: PRODUCT PORTFOLIO

- TABLE 98. UMICORE N.V.: KEY EXECUTIVES

- TABLE 99. UMICORE N.V.: COMPANY SNAPSHOT

- TABLE 100. UMICORE N.V.: PRODUCT SEGMENTS

- TABLE 101. UMICORE N.V.: PRODUCT PORTFOLIO

- TABLE 102. UMICORE N.V.: KEY STRATERGIES

- TABLE 103. REDWOOD MATERIALS INC.: KEY EXECUTIVES

- TABLE 104. REDWOOD MATERIALS INC.: COMPANY SNAPSHOT

- TABLE 105. REDWOOD MATERIALS INC.: PRODUCT SEGMENTS

- TABLE 106. REDWOOD MATERIALS INC.: PRODUCT PORTFOLIO

- TABLE 107. CIRBA SOLUTIONS: KEY EXECUTIVES

- TABLE 108. CIRBA SOLUTIONS: COMPANY SNAPSHOT

- TABLE 109. CIRBA SOLUTIONS: PRODUCT SEGMENTS

- TABLE 110. CIRBA SOLUTIONS: PRODUCT PORTFOLIO

- TABLE 111. CIRBA SOLUTIONS: KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. BATTERY MATERIALS RECYCLING MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF BATTERY MATERIALS RECYCLING MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN BATTERY MATERIALS RECYCLING MARKET (2023-2032)

- FIGURE 04. HIGH BARGAINING POWER OF SUPPLIERS

- FIGURE 05. HIGH THREAT OF NEW ENTRANTS

- FIGURE 06. MODERATE THREAT OF SUBSTITUTES

- FIGURE 07. HIGH INTENSITY OF RIVALRY

- FIGURE 08. MODERATE BARGAINING POWER OF BUYERS

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALBATTERY MATERIALS RECYCLING MARKET

- FIGURE 10. IMPACT OF KEY REGULATION: BATTERY MATERIALS RECYCLING MARKET

- FIGURE 10. BATTERY MATERIALS RECYCLING MARKET, BY MATERIAL TYPE, 2022(%)

- FIGURE 11. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR LITHIUM, BY COUNTRY 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR COBALT, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR IRON, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR MANGANESE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR NICKLE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR LEAD, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. BATTERY MATERIALS RECYCLING MARKET, BY END-USE, 2022(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR AUTOMOTIVE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR BUILDING AND CONSTRUCTION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR AEROSPACE AND DEFENSE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR TEXTILE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF BATTERY MATERIALS RECYCLING MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. BATTERY MATERIALS RECYCLING MARKET BY REGION, 2022

- FIGURE 25. U.S. BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 26. CANADA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 27. MEXICO BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 28. GERMANY BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 29. FRANCE BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 30. ITALY BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 31. SPAIN BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 32. UK BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 33. REST OF EUROPE BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 34. CHINA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 35. JAPAN BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 36. INDIA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 37. SOUTH KOREA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 38. AUSTRALIA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF ASIA-PACIFIC BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 40. BRAZIL BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SAUDI ARABIA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 42. SOUTH AFRICA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 43. REST OF LAMEA BATTERY MATERIALS RECYCLING MARKET, 2022-2032 ($MILLION)

- FIGURE 44. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 45. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 46. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 47. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 48. COMPETITIVE DASHBOARD

- FIGURE 49. COMPETITIVE HEATMAP: BATTERY MATERIALS RECYCLING MARKET

- FIGURE 50. TOP PLAYER POSITIONING, 2022

- FIGURE 51. GEM CO., LTD.: NET SALES, 2021-2022 ($MILLION)

- FIGURE 52. GEM CO., LTD.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 53. GRAVITA INDIA LIMITED: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 54. UMICORE: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 55. UMICORE: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 56. UMICORE: REVENUE SHARE BY REGION, 2021 (%)

電池回收市場(按電池類型、黑液來源、加工技術和垂直產業)—2025 年至 2030 年全球預測

電池回收市場(按電池類型、黑液來源、加工技術和垂直產業)—2025 年至 2030 年全球預測 2025-2029年全球電池回收

2025-2029年全球電池回收 2025-2029年二次電池回收市場

2025-2029年二次電池回收市場 全球電池材料回收市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年

全球電池材料回收市場研究報告-產業分析、規模、佔有率、成長、趨勢與預測 2025 年至 2033 年 電池材料回收市場規模、佔有率和成長分析(按材料類型、最終用戶和地區)- 產業預測 2025-2032電池回收市場規模、佔有率和成長分析(按化學成分、供應來源、材料、消費者細分、應用、最終用戶和地區)—2025-2032 年產業預測

電池材料回收市場規模、佔有率和成長分析(按材料類型、最終用戶和地區)- 產業預測 2025-2032電池回收市場規模、佔有率和成長分析(按化學成分、供應來源、材料、消費者細分、應用、最終用戶和地區)—2025-2032 年產業預測 2025 年電池回收全球市場報告

2025 年電池回收全球市場報告 印度的電池回收市場:各材料,各電池類型,各流程類型,各來源,各地區,機會,預測,2018年~2032年電池回收:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年)

印度的電池回收市場:各材料,各電池類型,各流程類型,各來源,各地區,機會,預測,2018年~2032年電池回收:市場佔有率分析、行業趨勢和統計、成長預測(2025-2030 年) 電池回收市場:成長、未來展望與競爭分析(2025-2033)

電池回收市場:成長、未來展望與競爭分析(2025-2033)