|

市場調查報告書

商品編碼

1344319

細胞冷凍保存市場:按類型、應用和最終用戶分類:2023-2032 年全球機會分析和產業預測Cell Cryopreservation Market By Type, By Application, By End User : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

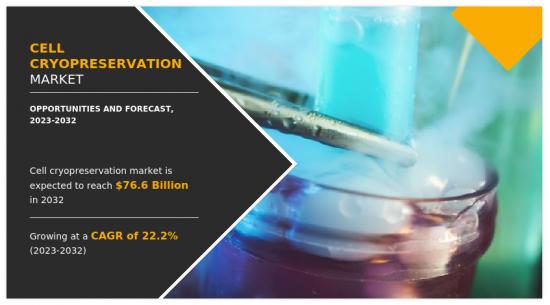

根據Allied Market Research發布的研究報告《細胞冷凍保存市場》,2022年細胞冷凍保存市場價值為103億美元,2023年至2032年將以22.2%的複合年增長率增長。預計到 2032 年將增長至 766 億美元。

細胞冷凍保存是在超低溫下冷凍保存細胞的過程,以長期保持其活力和功能。 該技術允許儲存細胞並隨後解凍以用於研究、醫學和其他用途。 這項研究針對幹細胞、卵母細胞、精子細胞和其他應用。 此外,主要最終用戶包括製藥公司、生技公司、研究機構等。

全球細胞冷凍保存市場的成長主要是由女性不孕症的增加以及卵子冷凍週期數量的增加所推動的。 輔助生殖技術協會報告稱,從 2020 年到 2021 年,美國的卵子冷凍週期增加了 31%。 此外,生物樣本庫的不斷增加預計將推動細胞冷凍保存市場的成長。 生物樣本庫因其在促進生物醫學研究、藥物發現和個人化醫療方面的關鍵作用而受到關注。 根據生物樣本庫資源中心統計,截至2023年,共有340個註冊生物樣本庫,其中包括加拿大和國際生物樣本庫。

此外,根據《生物保存與生物銀行雜誌》報道,2022 年將有來自 17 個國家的 641 個生物樣本庫在 BBMRI 目錄中註冊(截至 2021 年 2 月 12 日)。 隨著生物樣本庫技術的進步以及更大、更全面的生物樣本庫的建立,對高效、可靠的細胞冷凍保存方法的需求顯著增加。 此外,製藥和生物技術行業研發活動的增加、政府對研發活動的支持增加以及癌症和帕金森氏症等慢性病盛行率的增加正在推動市場成長。

據衛生資源和服務管理局稱,到 2023 年,美國捐贈者登記冊中將包括超過 900 萬潛在捐贈者。 此外,根據美國國家醫學圖書館的數據,到2022年,胚胎幹細胞將完成各種臨床前研究,用於治療多種疾病,包括視網膜疾病、帕金森氏症、亨廷頓舞蹈症、脊髓損傷、心肌病變等。梗塞和第 1 型糖尿病。據報導正在進行活動。 此外,印度政府透過印度醫學研究委員會 (ICMR)、生物技術部 (DBT) 和科學技術部 (DST) 等國家資助機構,不僅支持基礎研究,還支持各種研究計畫還包括臨床研究。幹細胞研究是透過各部會和機構進行的。

根據監管事務專業協會的數據,2021 年約有 2,754 家診所提供幹細胞治療。 因此,對幹細胞治療的需求不斷增長是細胞冷凍保存市場的關鍵驅動力。 此外,個人化醫療需求的激增預計將成為細胞冷凍保存市場的關鍵驅動力。 基於細胞的療法,例如基於免疫細胞的免疫療法和工程細胞療法,正在研究作為個人化治療的方法。 冷凍保存可長期保存患者特異性細胞,包括免疫細胞,並可用於開發個人化治療。

透過保存這些細胞,冷凍保存可確保它們在患者特定治療需要時可用。 隨著人們對個人化醫療的興趣增加,對細胞冷凍保存方法和儲存設施的需求也隨之增加,推動了全球市場的成長。 此外,不孕率上升也對市場成長做出了重大貢獻。 然而,替代細胞冷凍保存療法的可用性和維持保存程序的高成本阻礙了市場成長。

目錄

第1章簡介

第 2 章執行摘要

第3章市場概述

- 市場定義和範圍

- 主要發現

- 影響因素

- 主要投資機會

- 波特五力分析

- 市場動態

- 促進因素

- 增加卵子冷凍週期

- 增加幹細胞研究和開發活動

- 生物樣本庫數量增加,個人化醫療需求快速成長

- 抑制因素

- 細胞冷凍保存替代療法的可用性

- 機會

- 政府加大對研發活動的支持

- 越來越多的製造商致力於開發新產品來保存各種細胞

- 促進因素

- 新冠肺炎 (COVID-19) 造成的市場影響分析

- 專利情況

第 4 章細胞冷凍保存市場:依類型

- 冷凍保存介質

- 細胞冷凍保存市場:依代理商劃分

- 設備

- 細胞冷凍保存市場:依類型

第 5 章細胞冷凍保存市場:依應用分類

- 幹細胞

- 卵母細胞

- 精子細胞

- 其他

第 6 章細胞冷凍保存市場:依最終使用者劃分

- 製藥和生技公司

- 研究院

- 其他

第 7 章細胞冷凍保存市場:依地區

- 北美

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 日本

- 中國

- 印度

- 澳大利亞

- 韓國

- 馬來西亞

- 其他亞太地區

- 拉丁美洲/中東/非洲

- 巴西

- 南非

- 沙烏地阿拉伯

- 其他領域

第8章競爭態勢

- 簡介

- 關鍵成功策略

- 10家主要公司的產品圖譜

- 競爭對手儀表板

- 競爭熱圖

- 2022 年主要公司的定位

第9章公司簡介

- Creative Biolabs

- Eppendorf Corporate

- Lonza

- PromoCell GmbH

- Sartorius AG

- BioLife Solutions, Inc.

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- HiMedia Laboratories

- Merck Group KGaA

According to a new report published by Allied Market Research, titled, "Cell Cryopreservation Market," The cell cryopreservation market was valued at $10.3 billion in 2022, and is estimated to reach $76.6 billion by 2032, growing at a CAGR of 22.2% from 2023 to 2032. Cell cryopreservation is the process of freezing and storing cells at ultra-low temperatures to preserve their viability and functionality for extended periods. This technique allows cells to be stored and later thawed for use in research, medical treatments, or other applications. The applications covered in t study include stem cells, oocytes cells, sperm cells, and others. In addition, pharmaceutical & biotechnology company, research institute, and others are the major end users detailed in the report.

The growth of the global cell cryopreservation market is majorly driven by increase in infertility among women coupled with rise in number of egg freezing cycles. According to The Society for Assisted Reproductive Technology, it was reported that the egg freezing cycle increased by 31% from 2020 to 2021 in the U.S. In addition, rise in presence of biobanks is anticipated to drive the growth of the cell cryopreservation market. Biobanking has gained prominence due to its crucial role in facilitating biomedical research, drug discovery, and personalized medicine. According to the Biobank Resource Center, as of 2023, there are 340 registered biobanks, including both Canadian and international biobanks.

Moreover, according to the Journal of Biopreservation and Biobanking, in 2022, it was reported that the BBMRI directory listed 641 biobanks from 17 countries (as of February 12, 2021). With the advancement of biobanking technologies and the establishment of larger and more comprehensive biobanks, the demand for efficient and reliable cell cryopreservation methods has grown significantly. Furthermore, increase in R&D activities in pharmaceutical and biotechnology industries, rise in government support for R&D activities, and increase in prevalence of chronic diseases such as cancer and Parkinson's propel the growth of the market.

According to Health Resource and Service Administration, in 2023, it was reported that the donor registry contains more than 9 million potential donors in the U.S. Furthermore, as per the National Library of Medicine, in 2022, it was reported that various preclinical research activities are conducted in embryonic stem cells for the treatment of wide range of disease such as retinal diseases, Parkinson's disease, Huntington's disease, spinal cord injury, myocardial infarction, and type 1 diabetes. In addition, the Government of India conducted stem cell research through various departments and institutions by supporting basic as well as clinical research through national funding agencies such as the Indian Council of Medical Research (ICMR), Department of Biotechnology (DBT), and Department of Science and Technology (DST).

Furthermore, according to Regulatory Affairs Professionals Society, in 2021, there were around 2,754 clinics engaged in providing stem cell therapies. Consequently, the growing demand for stem cell therapies acts as a significant driver of the cell cryopreservation market. In addition, surge in demand for personalized medicines is expected to act as a significant driver of the cell cryopreservation market. Cell-based therapies, such as immune cell-based immunotherapies and engineered cell therapies, are being explored as personalized treatment approaches. Cryopreservation enables long-term storage of patient-specific cells, including immune cells, which can be used in the development of personalized therapies.

By preserving these cells, cryopreservation ensures their availability when needed for patient-specific treatments. As the interest in personalized medicine continues to grow, the demand for cell cryopreservation methods and storage facilities increases simultaneously, thereby augmenting the growth of the global market. Furthermore, rise in infertility rates notably contributes toward the growth of the market. However, availability of alternative therapies for cell cryopreservation and high maintenance cost in storage procedure hinder the growth of the market.

- The global cell cryopreservation market is segmented into type, application, end user, and region. On the basis of type, the market is bifurcated into cryopreservation media and equipment. The cryopreservation media segment is further sub segmented into ethylene glycol, dimethyl sulfoxide, glycerol, and others.. The equipment segment is subsegmented into freezers, liquid nitrogen supply tanks, and others.

- Depending on application, the market is classified into stem cells, oocytes cells, sperm cells, and others. By end user, it is segregated into pharmaceutical & biotechnology company, research institute, and others. Region wise, it is studied across North America (the U.S., Canada, and Mexico), Europe (Germany, France, UK, Italy, Spain, and rest of Europe), Asia-Pacific (China, Japan, Australia, India, and rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, and rest of LAMEA). The major companies profiled in the report include: Merck Group KGaA, HiMedia Laboratories, Thermo Fisher Scientific Inc. , Eppendorf Corporate, BioLife Solutions, Inc., Lonza, Sartorius AG, Creative Biolabs, Sartorius AG, and PromoCell GmbH.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the cell cryopreservation market analysis from 2021 to 2031 to identify the prevailing cell cryopreservation market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the cell cryopreservation market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global cell cryopreservation market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Type

- Cryopreservation media

- Agent

- Ethylene glycol

- Dimethyl sulfoxide

- Glycerol

- Others

- Equipment

- Type

- Freezers

- Liquid nitrogen supply tanks

- Others

By Application

- Stem cells

- Oocytes cells

- Sperm cells

- Others

By End User

- Pharmaceutical and biotechnology company

- Research institute

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Malaysia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa,

- Saudi Arabia

- Rest of LAMEA

Key Market Players:

- BioLife Solutions, Inc.

- Creative Biolabs

- Danaher Corporation

- Eppendorf Corporate

- HiMedia Laboratories

- Lonza

- Merck Group KGaA

- PromoCell GmbH

- Sartorius AG

- Thermo Fisher Scientific Inc.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Low bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Low bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Increase in number of egg freezing cycles

- 3.4.1.2. Increase in research and development activities for stem cells

- 3.4.1.3. Rise in number of biobanks and surge in demand for personalized medicines

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. Availability of alternative therapies for cell cryopreservation

- 3.4.3. Opportunities

- 3.4.3.1. Increase in government support for research and development activities

- 3.4.3.2. Rise in focus of manufacturers on developing novel products for preserving various cells

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Patent Landscape

CHAPTER 4: CELL CRYOPRESERVATION MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Cryopreservation media

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.2.4. Cryopreservation media Cell Cryopreservation Market by Agent

- 4.3. Equipment

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.3.4. Equipment Cell Cryopreservation Market by Type

CHAPTER 5: CELL CRYOPRESERVATION MARKET, BY APPLICATION

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Stem cells

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Oocytes cells

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Sperm cells

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Others

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

CHAPTER 6: CELL CRYOPRESERVATION MARKET, BY END USER

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Pharmaceutical and biotechnology company

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Research institute

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Others

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: CELL CRYOPRESERVATION MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key trends and opportunities

- 7.2.2. Market size and forecast, by Type

- 7.2.3. Market size and forecast, by Application

- 7.2.4. Market size and forecast, by End User

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Key market trends, growth factors and opportunities

- 7.2.5.1.2. Market size and forecast, by Type

- 7.2.5.1.3. Market size and forecast, by Application

- 7.2.5.1.4. Market size and forecast, by End User

- 7.2.5.2. Canada

- 7.2.5.2.1. Key market trends, growth factors and opportunities

- 7.2.5.2.2. Market size and forecast, by Type

- 7.2.5.2.3. Market size and forecast, by Application

- 7.2.5.2.4. Market size and forecast, by End User

- 7.2.5.3. Mexico

- 7.2.5.3.1. Key market trends, growth factors and opportunities

- 7.2.5.3.2. Market size and forecast, by Type

- 7.2.5.3.3. Market size and forecast, by Application

- 7.2.5.3.4. Market size and forecast, by End User

- 7.3. Europe

- 7.3.1. Key trends and opportunities

- 7.3.2. Market size and forecast, by Type

- 7.3.3. Market size and forecast, by Application

- 7.3.4. Market size and forecast, by End User

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Key market trends, growth factors and opportunities

- 7.3.5.1.2. Market size and forecast, by Type

- 7.3.5.1.3. Market size and forecast, by Application

- 7.3.5.1.4. Market size and forecast, by End User

- 7.3.5.2. France

- 7.3.5.2.1. Key market trends, growth factors and opportunities

- 7.3.5.2.2. Market size and forecast, by Type

- 7.3.5.2.3. Market size and forecast, by Application

- 7.3.5.2.4. Market size and forecast, by End User

- 7.3.5.3. UK

- 7.3.5.3.1. Key market trends, growth factors and opportunities

- 7.3.5.3.2. Market size and forecast, by Type

- 7.3.5.3.3. Market size and forecast, by Application

- 7.3.5.3.4. Market size and forecast, by End User

- 7.3.5.4. Italy

- 7.3.5.4.1. Key market trends, growth factors and opportunities

- 7.3.5.4.2. Market size and forecast, by Type

- 7.3.5.4.3. Market size and forecast, by Application

- 7.3.5.4.4. Market size and forecast, by End User

- 7.3.5.5. Spain

- 7.3.5.5.1. Key market trends, growth factors and opportunities

- 7.3.5.5.2. Market size and forecast, by Type

- 7.3.5.5.3. Market size and forecast, by Application

- 7.3.5.5.4. Market size and forecast, by End User

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Key market trends, growth factors and opportunities

- 7.3.5.6.2. Market size and forecast, by Type

- 7.3.5.6.3. Market size and forecast, by Application

- 7.3.5.6.4. Market size and forecast, by End User

- 7.4. Asia-Pacific

- 7.4.1. Key trends and opportunities

- 7.4.2. Market size and forecast, by Type

- 7.4.3. Market size and forecast, by Application

- 7.4.4. Market size and forecast, by End User

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. Japan

- 7.4.5.1.1. Key market trends, growth factors and opportunities

- 7.4.5.1.2. Market size and forecast, by Type

- 7.4.5.1.3. Market size and forecast, by Application

- 7.4.5.1.4. Market size and forecast, by End User

- 7.4.5.2. China

- 7.4.5.2.1. Key market trends, growth factors and opportunities

- 7.4.5.2.2. Market size and forecast, by Type

- 7.4.5.2.3. Market size and forecast, by Application

- 7.4.5.2.4. Market size and forecast, by End User

- 7.4.5.3. India

- 7.4.5.3.1. Key market trends, growth factors and opportunities

- 7.4.5.3.2. Market size and forecast, by Type

- 7.4.5.3.3. Market size and forecast, by Application

- 7.4.5.3.4. Market size and forecast, by End User

- 7.4.5.4. Australia

- 7.4.5.4.1. Key market trends, growth factors and opportunities

- 7.4.5.4.2. Market size and forecast, by Type

- 7.4.5.4.3. Market size and forecast, by Application

- 7.4.5.4.4. Market size and forecast, by End User

- 7.4.5.5. South Korea

- 7.4.5.5.1. Key market trends, growth factors and opportunities

- 7.4.5.5.2. Market size and forecast, by Type

- 7.4.5.5.3. Market size and forecast, by Application

- 7.4.5.5.4. Market size and forecast, by End User

- 7.4.5.6. Malaysia

- 7.4.5.6.1. Key market trends, growth factors and opportunities

- 7.4.5.6.2. Market size and forecast, by Type

- 7.4.5.6.3. Market size and forecast, by Application

- 7.4.5.6.4. Market size and forecast, by End User

- 7.4.5.7. Rest of Asia-Pacific

- 7.4.5.7.1. Key market trends, growth factors and opportunities

- 7.4.5.7.2. Market size and forecast, by Type

- 7.4.5.7.3. Market size and forecast, by Application

- 7.4.5.7.4. Market size and forecast, by End User

- 7.5. LAMEA

- 7.5.1. Key trends and opportunities

- 7.5.2. Market size and forecast, by Type

- 7.5.3. Market size and forecast, by Application

- 7.5.4. Market size and forecast, by End User

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Key market trends, growth factors and opportunities

- 7.5.5.1.2. Market size and forecast, by Type

- 7.5.5.1.3. Market size and forecast, by Application

- 7.5.5.1.4. Market size and forecast, by End User

- 7.5.5.2. South Africa,

- 7.5.5.2.1. Key market trends, growth factors and opportunities

- 7.5.5.2.2. Market size and forecast, by Type

- 7.5.5.2.3. Market size and forecast, by Application

- 7.5.5.2.4. Market size and forecast, by End User

- 7.5.5.3. Saudi Arabia

- 7.5.5.3.1. Key market trends, growth factors and opportunities

- 7.5.5.3.2. Market size and forecast, by Type

- 7.5.5.3.3. Market size and forecast, by Application

- 7.5.5.3.4. Market size and forecast, by End User

- 7.5.5.4. Rest of LAMEA

- 7.5.5.4.1. Key market trends, growth factors and opportunities

- 7.5.5.4.2. Market size and forecast, by Type

- 7.5.5.4.3. Market size and forecast, by Application

- 7.5.5.4.4. Market size and forecast, by End User

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product Mapping of Top 10 Player

- 8.4. Competitive Dashboard

- 8.5. Competitive Heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Creative Biolabs

- 9.1.1. Company overview

- 9.1.2. Key Executives

- 9.1.3. Company snapshot

- 9.1.4. Operating business segments

- 9.1.5. Product portfolio

- 9.2. Eppendorf Corporate

- 9.2.1. Company overview

- 9.2.2. Key Executives

- 9.2.3. Company snapshot

- 9.2.4. Operating business segments

- 9.2.5. Product portfolio

- 9.2.6. Business performance

- 9.2.7. Key strategic moves and developments

- 9.3. Lonza

- 9.3.1. Company overview

- 9.3.2. Key Executives

- 9.3.3. Company snapshot

- 9.3.4. Operating business segments

- 9.3.5. Product portfolio

- 9.3.6. Business performance

- 9.4. PromoCell GmbH

- 9.4.1. Company overview

- 9.4.2. Key Executives

- 9.4.3. Company snapshot

- 9.4.4. Operating business segments

- 9.4.5. Product portfolio

- 9.5. Sartorius AG

- 9.5.1. Company overview

- 9.5.2. Key Executives

- 9.5.3. Company snapshot

- 9.5.4. Operating business segments

- 9.5.5. Product portfolio

- 9.5.6. Business performance

- 9.6. BioLife Solutions, Inc.

- 9.6.1. Company overview

- 9.6.2. Key Executives

- 9.6.3. Company snapshot

- 9.6.4. Operating business segments

- 9.6.5. Product portfolio

- 9.6.6. Business performance

- 9.6.7. Key strategic moves and developments

- 9.7. Danaher Corporation

- 9.7.1. Company overview

- 9.7.2. Key Executives

- 9.7.3. Company snapshot

- 9.7.4. Operating business segments

- 9.7.5. Product portfolio

- 9.7.6. Business performance

- 9.7.7. Key strategic moves and developments

- 9.8. Thermo Fisher Scientific Inc.

- 9.8.1. Company overview

- 9.8.2. Key Executives

- 9.8.3. Company snapshot

- 9.8.4. Operating business segments

- 9.8.5. Product portfolio

- 9.8.6. Business performance

- 9.8.7. Key strategic moves and developments

- 9.9. HiMedia Laboratories

- 9.9.1. Company overview

- 9.9.2. Key Executives

- 9.9.3. Company snapshot

- 9.9.4. Operating business segments

- 9.9.5. Product portfolio

- 9.10. Merck Group KGaA

- 9.10.1. Company overview

- 9.10.2. Key Executives

- 9.10.3. Company snapshot

- 9.10.4. Operating business segments

- 9.10.5. Product portfolio

- 9.10.6. Business performance

LIST OF TABLES

- TABLE 01. GLOBAL CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. CELL CRYOPRESERVATION MARKET FOR CRYOPRESERVATION MEDIA, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. GLOBAL CRYOPRESERVATION MEDIA CELL CRYOPRESERVATION MARKET, BY AGENT, 2022-2032 ($MILLION)

- TABLE 04. CELL CRYOPRESERVATION MARKET FOR EQUIPMENT, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. GLOBAL EQUIPMENT CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 06. GLOBAL CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 07. CELL CRYOPRESERVATION MARKET FOR STEM CELLS, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. CELL CRYOPRESERVATION MARKET FOR OOCYTES CELLS, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. CELL CRYOPRESERVATION MARKET FOR SPERM CELLS, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. CELL CRYOPRESERVATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. GLOBAL CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 12. CELL CRYOPRESERVATION MARKET FOR PHARMACEUTICAL AND BIOTECHNOLOGY COMPANY, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. CELL CRYOPRESERVATION MARKET FOR RESEARCH INSTITUTE, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. CELL CRYOPRESERVATION MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. CELL CRYOPRESERVATION MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 19. NORTH AMERICA CELL CRYOPRESERVATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 20. U.S. CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 21. U.S. CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 22. U.S. CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 23. CANADA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 24. CANADA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 25. CANADA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 26. MEXICO CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 27. MEXICO CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 28. MEXICO CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 29. EUROPE CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 30. EUROPE CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 31. EUROPE CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 32. EUROPE CELL CRYOPRESERVATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 33. GERMANY CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 34. GERMANY CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 35. GERMANY CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 36. FRANCE CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 37. FRANCE CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 38. FRANCE CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 39. UK CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 40. UK CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 41. UK CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 42. ITALY CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 43. ITALY CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 44. ITALY CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 45. SPAIN CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 46. SPAIN CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 47. SPAIN CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 48. REST OF EUROPE CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 49. REST OF EUROPE CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 50. REST OF EUROPE CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 51. ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 52. ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 53. ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 54. ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 55. JAPAN CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 56. JAPAN CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 57. JAPAN CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 58. CHINA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 59. CHINA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 60. CHINA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 61. INDIA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 62. INDIA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 63. INDIA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 64. AUSTRALIA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 66. AUSTRALIA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 67. SOUTH KOREA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 68. SOUTH KOREA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 69. SOUTH KOREA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 70. MALAYSIA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 71. MALAYSIA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 72. MALAYSIA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 73. REST OF ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 74. REST OF ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 75. REST OF ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 76. LAMEA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 77. LAMEA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 78. LAMEA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 79. LAMEA CELL CRYOPRESERVATION MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 80. BRAZIL CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 81. BRAZIL CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 82. BRAZIL CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 83. SOUTH AFRICA, CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 84. SOUTH AFRICA, CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 85. SOUTH AFRICA, CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 86. SAUDI ARABIA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 87. SAUDI ARABIA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 88. SAUDI ARABIA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 89. REST OF LAMEA CELL CRYOPRESERVATION MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 90. REST OF LAMEA CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 91. REST OF LAMEA CELL CRYOPRESERVATION MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 92. CREATIVE BIOLABS: KEY EXECUTIVES

- TABLE 93. CREATIVE BIOLABS: COMPANY SNAPSHOT

- TABLE 94. CREATIVE BIOLABS: PRODUCT SEGMENTS

- TABLE 95. CREATIVE BIOLABS: SERVICE SEGMENTS

- TABLE 96. CREATIVE BIOLABS: PRODUCT PORTFOLIO

- TABLE 97. EPPENDORF CORPORATE: KEY EXECUTIVES

- TABLE 98. EPPENDORF CORPORATE: COMPANY SNAPSHOT

- TABLE 99. EPPENDORF CORPORATE: PRODUCT SEGMENTS

- TABLE 100. EPPENDORF CORPORATE: PRODUCT PORTFOLIO

- TABLE 101. EPPENDORF CORPORATE: KEY STRATERGIES

- TABLE 102. LONZA: KEY EXECUTIVES

- TABLE 103. LONZA: COMPANY SNAPSHOT

- TABLE 104. LONZA: PRODUCT SEGMENTS

- TABLE 105. LONZA: SERVICE SEGMENTS

- TABLE 106. LONZA: PRODUCT PORTFOLIO

- TABLE 107. PROMOCELL GMBH: KEY EXECUTIVES

- TABLE 108. PROMOCELL GMBH: COMPANY SNAPSHOT

- TABLE 109. PROMOCELL GMBH: PRODUCT SEGMENTS

- TABLE 110. PROMOCELL GMBH: PRODUCT PORTFOLIO

- TABLE 111. SARTORIUS AG: KEY EXECUTIVES

- TABLE 112. SARTORIUS AG: COMPANY SNAPSHOT

- TABLE 113. SARTORIUS AG: PRODUCT SEGMENTS

- TABLE 114. SARTORIUS AG: PRODUCT PORTFOLIO

- TABLE 115. BIOLIFE SOLUTIONS, INC.: KEY EXECUTIVES

- TABLE 116. BIOLIFE SOLUTIONS, INC.: COMPANY SNAPSHOT

- TABLE 117. BIOLIFE SOLUTIONS, INC.: PRODUCT SEGMENTS

- TABLE 118. BIOLIFE SOLUTIONS, INC.: SERVICE SEGMENTS

- TABLE 119. BIOLIFE SOLUTIONS, INC.: PRODUCT PORTFOLIO

- TABLE 120. BIOLIFE SOLUTIONS, INC.: KEY STRATERGIES

- TABLE 121. DANAHER CORPORATION: KEY EXECUTIVES

- TABLE 122. DANAHER CORPORATION: COMPANY SNAPSHOT

- TABLE 123. DANAHER CORPORATION: PRODUCT SEGMENTS

- TABLE 124. DANAHER CORPORATION: PRODUCT PORTFOLIO

- TABLE 125. DANAHER CORPORATION: KEY STRATERGIES

- TABLE 126. THERMO FISHER SCIENTIFIC INC. : KEY EXECUTIVES

- TABLE 127. THERMO FISHER SCIENTIFIC INC. : COMPANY SNAPSHOT

- TABLE 128. THERMO FISHER SCIENTIFIC INC. : PRODUCT SEGMENTS

- TABLE 129. THERMO FISHER SCIENTIFIC INC. : SERVICE SEGMENTS

- TABLE 130. THERMO FISHER SCIENTIFIC INC. : PRODUCT PORTFOLIO

- TABLE 131. THERMO FISHER SCIENTIFIC INC. : KEY STRATERGIES

- TABLE 132. HIMEDIA LABORATORIES: KEY EXECUTIVES

- TABLE 133. HIMEDIA LABORATORIES: COMPANY SNAPSHOT

- TABLE 134. HIMEDIA LABORATORIES: PRODUCT SEGMENTS

- TABLE 135. HIMEDIA LABORATORIES: PRODUCT PORTFOLIO

- TABLE 136. MERCK GROUP KGAA: KEY EXECUTIVES

- TABLE 137. MERCK GROUP KGAA: COMPANY SNAPSHOT

- TABLE 138. MERCK GROUP KGAA: PRODUCT SEGMENTS

- TABLE 139. MERCK GROUP KGAA: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. CELL CRYOPRESERVATION MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF CELL CRYOPRESERVATION MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN CELL CRYOPRESERVATION MARKET (2023-2032)

- FIGURE 04. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 05. LOW THREAT OF NEW ENTRANTS

- FIGURE 06. LOW THREAT OF SUBSTITUTES

- FIGURE 07. LOW INTENSITY OF RIVALRY

- FIGURE 08. LOW BARGAINING POWER OF BUYERS

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALCELL CRYOPRESERVATION MARKET

- FIGURE 10. PATENT ANALYSIS BY COMPANY

- FIGURE 11. PATENT ANALYSIS BY COUNTRY

- FIGURE 11. CELL CRYOPRESERVATION MARKET, BY TYPE, 2022(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR CRYOPRESERVATION MEDIA, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR EQUIPMENT, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. CELL CRYOPRESERVATION MARKET, BY APPLICATION, 2022(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR STEM CELLS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR OOCYTES CELLS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR SPERM CELLS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. CELL CRYOPRESERVATION MARKET, BY END USER, 2022(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR PHARMACEUTICAL AND BIOTECHNOLOGY COMPANY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR RESEARCH INSTITUTE, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF CELL CRYOPRESERVATION MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. CELL CRYOPRESERVATION MARKET BY REGION, 2022

- FIGURE 24. U.S. CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 25. CANADA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 26. MEXICO CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 27. GERMANY CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 28. FRANCE CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 29. UK CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 30. ITALY CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 31. SPAIN CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 32. REST OF EUROPE CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 33. JAPAN CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 34. CHINA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 35. INDIA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 36. AUSTRALIA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 37. SOUTH KOREA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 38. MALAYSIA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF ASIA-PACIFIC CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 40. BRAZIL CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SOUTH AFRICA, CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 42. SAUDI ARABIA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 43. REST OF LAMEA CELL CRYOPRESERVATION MARKET, 2022-2032 ($MILLION)

- FIGURE 44. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 45. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 46. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 47. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 48. COMPETITIVE DASHBOARD

- FIGURE 49. COMPETITIVE HEATMAP: CELL CRYOPRESERVATION MARKET

- FIGURE 50. TOP PLAYER POSITIONING, 2022

- FIGURE 51. EPPENDORF CORPORATE: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 52. EPPENDORF CORPORATE: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 53. EPPENDORF CORPORATE: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 54. LONZA: NET SALES, 2020-2022 ($MILLION)

- FIGURE 55. LONZA: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 56. LONZA: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 57. SARTORIUS AG: NET SALES, 2020-2022 ($MILLION)

- FIGURE 58. SARTORIUS AG: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 59. SARTORIUS AG: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 60. BIOLIFE SOLUTIONS, INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 61. BIOLIFE SOLUTIONS, INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 62. DANAHER CORPORATION: NET SALES, 2020-2022 ($MILLION)

- FIGURE 63. DANAHER CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 64. DANAHER CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 65. THERMO FISHER SCIENTIFIC INC. : NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 66. THERMO FISHER SCIENTIFIC INC. : REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 67. THERMO FISHER SCIENTIFIC INC. : REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 68. MERCK GROUP KGAA: NET SALES, 2020-2022 ($MILLION)

- FIGURE 69. MERCK GROUP KGAA: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 70. MERCK GROUP KGAA: REVENUE SHARE BY REGION, 2022 (%)

全球無血清細胞冷凍保存介質市場:市場佔有率及排名、總銷售及需求預測(2025-2031)

全球無血清細胞冷凍保存介質市場:市場佔有率及排名、總銷售及需求預測(2025-2031) 2025年全球細胞冷凍保存市場報告

2025年全球細胞冷凍保存市場報告 全球細胞冷凍保存市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年

全球細胞冷凍保存市場研究報告 - 產業分析、規模、佔有率、成長、趨勢和預測 2025 年至 2033 年 細胞冷凍保存市場按產品類型、應用、最終用戶和地區分類細胞冷凍保存市場規模、佔有率和成長分析(按產品、應用、最終用途和地區)- 產業預測 2025-2032

細胞冷凍保存市場按產品類型、應用、最終用戶和地區分類細胞冷凍保存市場規模、佔有率和成長分析(按產品、應用、最終用途和地區)- 產業預測 2025-2032 細胞凍結保存的全球市場的評估:各產品,各用途,各終端用戶,各地區,機會,預測(2017年~2031年)

細胞凍結保存的全球市場的評估:各產品,各用途,各終端用戶,各地區,機會,預測(2017年~2031年) 全球冷凍保存設備市場細胞冷凍保存市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F生物保存市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F全球低溫保存設備市場:按設備、冷凍劑、應用、最終用戶、地區、機會、預測,2017-2031 年

全球冷凍保存設備市場細胞冷凍保存市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F生物保存市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、應用、地區和競爭細分,2019-2029F全球低溫保存設備市場:按設備、冷凍劑、應用、最終用戶、地區、機會、預測,2017-2031 年