|

市場調查報告書

商品編碼

2035059

資料中心刀鋒伺服器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Data Center Blade Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

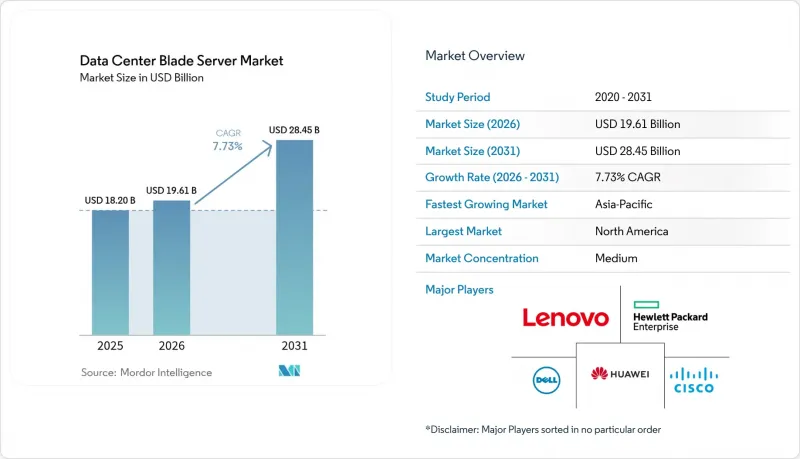

預計到 2026 年,資料中心刀鋒伺服器市場規模將達到 196.1 億美元,高於 2025 年的 182 億美元,預計到 2031 年將達到 284.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.73%。

人工智慧和機器學習工作負載的日益普及正在重新定義運算密度需求,促使供應商轉向可組合和解耦的刀片伺服器設計,將運算、儲存和網路資源分開。這種架構轉變能夠提高資源利用率並加快工作負載重新分配速度。直接液冷、矽光電背板和先進的底盤管理軟體使營運商能夠有效管理目前超過 30kW 的機架電力消耗量。北美在規模方面仍然主導,但亞太地區正在經歷更快的成長,這主要得益於印度、中國和新加坡的大規模新建設。託管資料中心仍然是最大的客戶群,但超大規模資料中心業者正在明確其技術發展方向,轉向專為提高機架級效率而設計的專用人工智慧刀片系統。

全球資料中心刀鋒伺服器市場趨勢及洞察。

機架級功率密度的提升可以應對人工智慧/機器學習工作負載。

人工智慧推理和訓練叢集正將機架功率密度從傳統的 10-15 kW 推高至 30-50 kW。開放運算專案 (OCP) 的 OSAI 規範針對 250 kW 至 1 MW 的機架架構,鼓勵刀鋒伺服器供應商整合高效電壓調節器和直接液冷技術。戴爾的 PowerEdge XE9680L 證明,底盤級氣流、冷板迴路和專用於人工智慧的加速器可以共存,而不會出現過熱降頻。國際能源總署 (IEA) 預測,到 2030 年,專用於人工智慧的資料中心可能消耗 945 TWh 的電量,因此,高效節能的刀片伺服器設計將成為營運商策略的核心。

邊緣運算和雲端運算技術的融合正在加速微模組化資料中心的普及。

5G 和超低延遲服務的部署正將運算重心轉移到網路邊緣,從而催生了對預裝線和冷卻系統的微型模組化資料中心的需求。谷歌的模組化邊緣設施專利凸顯了整合電源和散熱功能的安全多租戶機架組件的重要性。通訊業者正將 6000 億美元資本支出計劃中的相當一部分分配給這些邊緣站點,這為刀片伺服器供應商提供了機會,使其能夠提供針對有限安裝空間最佳化的四分之一高度節點。

矽光電帶來的資本投資激增以及向 800 GbE 背板的過渡

向光子積體電路和 800 GbE 架構的過渡將帶來延遲和頻寬的提升,但這需要新的底盤、中板連接器和重定時器卡。儘管各國監管機構都認可效率的提升,但他們也警告說,初始部署將產生巨大的資本成本,尤其對中型企業而言。關於透過 CXL 實現記憶體解耦的研究表明,投資回報需要數年時間,這將迫使營運商逐步完成升級。

細分市場分析

到2025年,三級資料中心將佔資料中心刀片伺服器市場的42.05%,其N+1冗餘配置符合主流企業服務等級協定(SLA)。四級資料中心雖然數量較少,但由於人工智慧訓練叢集對容錯能力的需求,預計將以11.63%的複合年成長率成長。這一成長動能正使四級資料中心成為全水冷底盤和矽光電技術的試驗場。

通常情況下,負責邊緣聚合和分支機構工作負載的一級和二級資料中心營運商正在採用標準化刀片伺服器,以在控制成本的同時實現更高的自動化程度。根據 Infrastructure Masons 的一份報告,目前 90% 的電力需求成長歸因於人工智慧模型訓練,而這種負載現在正蔓延到小規模的資料中心,這些資料中心必須適應更高的電力消耗和機架密度。因此,供應商正在提供用於維修低階機房的套件,包括封閉式通道和後門熱交換器,這維持了資料中心刀片伺服器市場的整體成長動能。

預計到 2025 年,半高刀鋒伺服器將佔總銷售量的 48.02%,其配備雙路 CPU、充足的 DIMM 插槽以及 PCIe 擴充功能,足以支援大多數虛擬化和資料庫任務。這些產品仍是企業級託管機架的旗艦產品。全高型號則繼續支援四路 CPU 和記憶體密集型工作負載,例如記憶體內分析。

四分之一高度和微型刀片節點,每個 10U 機架可容納 16 至 32 個運算線程,非常適合空間有限的邊緣安裝環境,並且是成長最快的細分市場,複合年成長率高達 13.39%。供應商目前正在將 GPU 加速器整合到這些緊湊型執行緒中,從而實現行動電話的即時推理。與 Open Rack v3 規範的兼容性允許在同一機櫃內進行混合部署,從而支援資料中心刀鋒伺服器市場邊緣部署的趨勢。

資料中心刀鋒伺服器市場報告按類型(Tier 1、Tier 2 等)、外形規格(半高刀片、全高刀片等)、最終用戶產業(銀行、金融服務和保險、製造業等)、資料中心類型(超大規模資料中心業者資料中心/雲端服務供應商等)和地區(亞太地區、歐洲等)對產業進行細分。市場預測以美元價值 (USD) 表示。

區域分析

到2025年,北美將佔據資料中心刀鋒伺服器市場41.88%的佔有率,這主要得益於維吉尼亞北部、德克薩斯州和矽谷的超大規模資料中心園區的發展。根據勞倫斯柏克萊國家實驗室估計,2023年美國資料中心的電力消耗量將達到176太瓦時(TWh),因此迫切需要水冷刀片伺服器來降低設施的PUE(電源使用效率)。此外,隨著區域主權雲端和災害復原區的建設,加拿大和墨西哥的需求也不斷成長。

亞太地區是成長最快的市場,預計2026年至2031年複合年成長率將達到11.92%。中國正在部署大規模人工智慧雲端叢集,而印度需要在2030年將裝置容量從1.35吉瓦擴展到5吉瓦,以實現其數位經濟目標。新加坡的政策框架優先考慮採用高密度葉片和熱回收冷卻器的設計方案的容量許可。日本和澳洲正在海底電纜登陸站沿線擴展其邊緣基礎設施,並部署四分之一高度的葉片用於內容快取。在嚴格的效率和數據主權法規下,歐洲市場保持穩定成長。生態設計指令2019/424的修訂建議採用支援35°C以上熱水冷卻的葉片底盤,以方便與區域供熱迴路整合。中東和非洲正在加大對金融科技和遊戲產業客戶雲端存取的投資。在南美洲,部署主要集中在巴西的網路交換中心附近,業者使用可組合刀鋒伺服器來應對季節性流量高峰。這些區域趨勢凸顯了資料中心刀鋒伺服器市場在全球的重要性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 機架級功率密度的大幅提升將使人工智慧/機器學習工作負載得以滿足。

- 邊緣運算和雲端運算技術的融合正在加速微模組化資料中心的普及。

- 伺服器整合率越高,營運費用(OPEX)和房地產成本就越低。

- 水冷底盤可獲得監管誘因(歐盟、新加坡)

- 超大規模資料中心業者。

- 市場限制因素

- 由於向矽光電和800 GbE背板過渡,資本投資激增

- 專有底盤系中的供應商集中度

- 管理多架構解耦架構的技能差距

- ORAN 和 5G 的商業化進程延遲將延長通訊業者資料中心的投資回報期。

- 供應鏈分析

- 監理情勢與永續發展趨勢

- 技術趨勢(PCIe 6.0、CXL 3.0、矽光電)

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭強度

- 評估宏觀經濟趨勢對市場的影響

第5章 市場規模與成長預測

- 資料中心層級

- 一級和二級

- 三級

- 第四級

- 按外形規格

- 半高刀片

- 全高刀片

- 四分之一高度/微刀片

- 按應用和工作負載

- 虛擬化和私有雲端

- 高效能運算(HPC)

- 人工智慧/機器學習和數據分析

- 以儲存為中心

- 邊緣/物聯網閘道器

- 依資料中心類型

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 託管設施

- 企業和邊緣運算

- 按最終用途行業分類

- BFSI

- IT/通訊/CSP

- 醫療保健和生命科學

- 製造業和工業4.0

- 能源與公共產業

- 政府/國防

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 新加坡

- 澳洲

- 馬來西亞

- 亞太其他地區

- 南美洲

- 巴西

- 智利

- 阿根廷

- 南美洲其他地區

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- Strategic Initiatives

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Dell Technologies

- Hewlett Packard Enterprise

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Fujitsu Ltd.

- Lenovo Group Ltd.

- NEC Corporation

- Oracle Corporation

- Super Micro Computer Inc.

- Inspur Group

- Quanta Cloud Technology

- Gigabyte Technology

- Hitachi Ltd.

- AMD(Pensando)

- Nvidia Corp.(Grace Superchip platforms)

- Marvell Technology(DPU-centric blades)

- Broadcom Inc.(Switch-on-Blade)

- Advantech Co. Ltd.

- Silicom Ltd.

- ZTE Corporation

第7章 市場機會與未來展望

Data Center Blade Server market size in 2026 is estimated at USD 19.61 billion, growing from 2025 value of USD 18.2 billion with 2031 projections showing USD 28.45 billion, growing at 7.73% CAGR over 2026-2031.

Rising deployment of AI and machine-learning workloads is reshaping compute density requirements, pushing vendors toward composable, disaggregated blade designs that separate compute, storage and networking resources. This architectural shift enables higher utilization and rapid workload re-allocation, while direct liquid cooling, silicon-photonics backplanes and advanced chassis management software help operators manage rack power envelopes that now exceed 30 kW. North America retains scale leadership, yet Asia-Pacific is growing faster on the back of large greenfield builds in India, China and Singapore. Colocation facilities remain the largest customer group, but hyperscalers are setting the technical agenda as they move to purpose-built AI blade systems that deliver higher rack-level efficiency.

Global Data Center Blade Server Market Trends and Insights

Surging Rack-Level Power Density Accommodates AI/ML Workloads

AI inference and training clusters now push rack envelopes from 10-15 kW toward 30-50 kW. The Open Compute Project's OSAI specification targets 250 kW to 1 MW rack architectures, encouraging blade vendors to integrate high-efficiency voltage regulators and direct liquid cooling. Dell's PowerEdge XE9680L demonstrates how chassis-level airflow, cold-plate loops, and AI-specific accelerators can coexist without thermal throttling. The International Energy Agency projects that AI-focused data centers could consume 945 TWh by 2030, which keeps power-efficient blade design at the center of operator strategies

Edge-Cloud Convergence Accelerating Deployment in Micro-Modular DCs

5G rollouts and ultra-low-latency services push compute to the network edge, spawning demand for micro-modular data centers that can ship pre-wired and pre-cooled. Google's patent for modular edge facilities confirms the importance of secure, multitenant rack assemblies with integrated power and heat exchange. Telecom operators are allocating a sizeable share of their USD 600 billion CAPEX plan to such edge sites, giving blade vendors an opening to supply quarter-height nodes tailored for constrained footprints

CapEx Spike from Silicon-Photonics and 800 GbE Backplane Migration

Switching to photonic integrated circuits and 800 GbE fabrics unlocks latency and bandwidth gains but demands new chassis, mid-plane connectors and retimer cards. National agencies acknowledge the efficiency upside yet caution that early deployments bear heavy capital costs, particularly for mid-sized enterprises. Research into memory disaggregation over CXL suggests a multi-year payback, forcing operators to stagger upgrades

Other drivers and restraints analyzed in the detailed report include:

- High Server Consolidation Ratios Lower OPEX and Real-Estate Cost

- Liquid-Cooling Ready Chassis Gaining Regulatory Incentives

- Supplier Concentration in Proprietary Chassis Ecosystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 3 facilities owned 42.05% of the Data Center Blade Server market in 2025, as their N+1 redundancy profile aligns with mainstream enterprise SLAs. Tier 4 sites, though smaller in count, are forecast to grow at 11.63% CAGR thanks to fault-tolerance demands from AI training clusters. This momentum positions Tier 4 as the proving ground for 100% liquid-cooled chassis and silicon-photonics interconnects.

Operators of Tier 1 and Tier 2 facilities, typically serving edge aggregation or branch workloads, adopt standardized blades to maintain cost discipline while gaining better automation. The Infrastructure Masons report links 90% of current power growth to AI model training, a load now propagating into even modest sites that must accommodate higher power draw and rack density. As a result, vendors are packaging kits that retrofit lower-tier rooms with containment aisles and rear-door heat exchangers, preserving momentum for the wider Data Center Blade Server market.

Half-height blades delivered 48.02% revenue in 2025, supporting dual-socket CPUs, ample DIMM slots and PCIe expansion for most virtualization and database tasks. They remain the workhorse of enterprise colocation racks. Full-height models continue to serve quad-socket, memory-bound workloads such as in-memory analytics.

Quarter-height and micro-blade nodes are the fastest-growing slice at 13.39% CAGR because they fit 16-32 compute sleds per 10U shelf, ideal for limited edge footprints. Vendors now integrate GPU accelerators into these compact sleds, enabling real-time inference at cell-tower sites. Compatibility with Open Rack v3 specifications allows mixed deployment inside the same cabinet, sustaining the Data Center Blade Server market's edge expansion narrative.

Data Center Blade Server Market Report Segments the Industry Into Type (Tier 1, Tier 2, and More), Form Factor(Half-Height Blades, Full-Height Blades, and More), End-User Verticals (BFSI, Manufacturing, and More), Data Center Type(Hyperscalers/Cloud Service Provider, and More) and Geography (Asia-Pacific, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 41.88% of the Data Center Blade Server market in 2025, fueled by hyperscale campuses in Northern Virginia, Texas and Silicon Valley. The Lawrence Berkeley National Laboratory calculated 176 TWh of US data-center electricity use in 2023, raising urgency for liquid-cooled blades that cut facility PUEs. Canada and Mexico add incremental demand through regional sovereign-cloud and disaster-recovery zones.

Asia-Pacific is the fastest-growing theater at 11.92% CAGR from 2026-2031. China deploys massive AI cloud clusters, while India needs to expand installed capacity from 1.35 GW to 5 GW by 2030 to keep pace with digital-economy targets. Policy frameworks in Singapore award capacity licenses preferentially to designs that include high-density blades and heat-recovery chillers. Japan and Australia extend the edge footprint along subsea cable landing stations, embedding quarter-height blades for content caching. Europe shows steady expansion under strict efficiency and data-sovereignty rules. Ecodesign 2019/424 revisions encourage blade chassis that support warm-water cooling above 35 °C, easing integration with district-heat loops. The Middle East and Africa attract investment for cloud on-ramps serving fintech and gaming customers. South America's installations cluster around Brazil's internet exchange hubs, where operators deploy composable blades to meet seasonal traffic peaks. These regional dynamics reinforce the global relevance of the Data Center Blade Server market.

- Cisco Systems Inc.

- Dell Technologies

- Hewlett Packard Enterprise

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Fujitsu Ltd.

- Lenovo Group Ltd.

- NEC Corporation

- Oracle Corporation

- Super Micro Computer Inc.

- Inspur Group

- Quanta Cloud Technology

- Gigabyte Technology

- Hitachi Ltd.

- AMD (Pensando)

- Nvidia Corp. (Grace Superchip platforms)

- Marvell Technology (DPU-centric blades)

- Broadcom Inc. (Switch-on-Blade)

- Advantech Co. Ltd.

- Silicom Ltd.

- ZTE Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging rack-level power density accommodates AI/ML workloads

- 4.2.2 Edge-cloud convergence accelerating deployment in micro-modular DCs

- 4.2.3 High server consolidation ratios lower OPEX and real-estate cost

- 4.2.4 Liquid-cooling ready chassis gaining regulatory incentives (EU, Singapore)

- 4.2.5 Growing hyperscaler preference for composable disaggregated blades

- 4.3 Market Restraints

- 4.3.1 CapEx spike from silicon photonics and 800 Gb E backplane migration

- 4.3.2 Supplier concentration in proprietary chassis ecosystems

- 4.3.3 Skill-gap in managing multi-fabric, disaggregated architectures

- 4.3.4 Delayed ORAN/5G monetisation lengthening ROI for telco DCs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory and Sustainability Landscape

- 4.6 Technological Outlook (PCIe 6.0, CXL 3.0, silicon photonics)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Assessment of the Impact on Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Data-Center Tier

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Form Factor

- 5.2.1 Half-height Blades

- 5.2.2 Full-height Blades

- 5.2.3 Quarter-height / Micro-blades

- 5.3 By Application / Workload

- 5.3.1 Virtualisation and Private Cloud

- 5.3.2 High-Performance Computing (HPC)

- 5.3.3 Artificial Intelligence/Machine Learning and Data Analytics

- 5.3.4 Storage-centric

- 5.3.5 Edge / IoT Gateways

- 5.4 By Data Center Type

- 5.4.1 Hyperscalers/Cloud Service Provider

- 5.4.2 Colocation Facilities

- 5.4.3 Enterprise and Edge

- 5.5 By End-use Industry

- 5.5.1 BFSI

- 5.5.2 IT and Telecom / CSPs

- 5.5.3 Healthcare and Life-Sciences

- 5.5.4 Manufacturing and Industry 4.0

- 5.5.5 Energy and Utilities

- 5.5.6 Government and Defence

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Singapore

- 5.6.3.5 Australia

- 5.6.3.6 Malaysia

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Chile

- 5.6.4.3 Argentina

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirate

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Dell Technologies

- 6.4.3 Hewlett Packard Enterprise

- 6.4.4 Huawei Technologies Co. Ltd.

- 6.4.5 IBM Corporation

- 6.4.6 Fujitsu Ltd.

- 6.4.7 Lenovo Group Ltd.

- 6.4.8 NEC Corporation

- 6.4.9 Oracle Corporation

- 6.4.10 Super Micro Computer Inc.

- 6.4.11 Inspur Group

- 6.4.12 Quanta Cloud Technology

- 6.4.13 Gigabyte Technology

- 6.4.14 Hitachi Ltd.

- 6.4.15 AMD (Pensando)

- 6.4.16 Nvidia Corp. (Grace Superchip platforms)

- 6.4.17 Marvell Technology (DPU-centric blades)

- 6.4.18 Broadcom Inc. (Switch-on-Blade)

- 6.4.19 Advantech Co. Ltd.

- 6.4.20 Silicom Ltd.

- 6.4.21 ZTE Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

ATCA CPU刀片市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

ATCA CPU刀片市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 全球刀鋒伺服器市場規模、佔有率、趨勢和成長分析報告(資料中心,2026-2034年)

全球刀鋒伺服器市場規模、佔有率、趨勢和成長分析報告(資料中心,2026-2034年) 資料中心刀鋒伺服器市場:按處理器類型、刀片高度、應用、最終用戶和部署模式分類 - 2026-2032 年全球預測

資料中心刀鋒伺服器市場:按處理器類型、刀片高度、應用、最終用戶和部署模式分類 - 2026-2032 年全球預測 2026年全球資料中心刀鋒伺服器市場報告

2026年全球資料中心刀鋒伺服器市場報告 刀鋒伺服器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按資料中心類型、服務、最終用戶、產業垂直領域、地區和競爭格局分類,2021-2031 年)

刀鋒伺服器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按資料中心類型、服務、最終用戶、產業垂直領域、地區和競爭格局分類,2021-2031 年) 2026-2030年全球資料中心刀鋒伺服器市場

2026-2030年全球資料中心刀鋒伺服器市場 資料中心刀鋒伺服器市場規模、佔有率、趨勢分析報告:按外形規格、通路、最終用途、地區和細分市場預測,2025 年至 2030 年資料中心刀鋒伺服器市場 - 2024 年至 2029 年預測

資料中心刀鋒伺服器市場規模、佔有率、趨勢分析報告:按外形規格、通路、最終用途、地區和細分市場預測,2025 年至 2030 年資料中心刀鋒伺服器市場 - 2024 年至 2029 年預測