|

市場調查報告書

商品編碼

2035057

電信塔:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Telecom Towers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

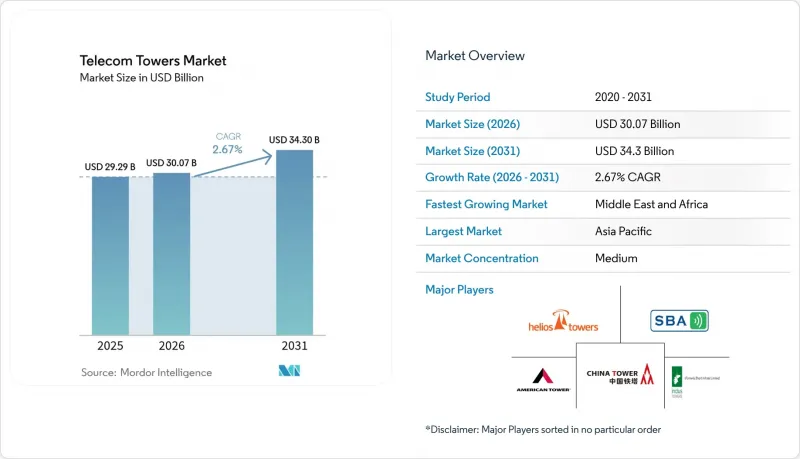

2025 年通訊塔市場價值 292.9 億美元,預計到 2031 年將達到 343 億美元,而 2026 年為 300.7 億美元,預測期(2026-2031 年)複合年成長率為 2.67%。

這種穩定成長的趨勢反映出行動網路營運商(MNO)正從快速部署新設施轉向基礎設施共用和節能升級,以在資本密集型環境中保障獲利能力。由於5G的持續密集化、政府主導的區域覆蓋計劃以及混合可再生能源系統的加速部署,市場需求依然強勁,但由於託管費用和頻寬成本的上漲給運營商的預算帶來壓力,整體成長速度仍然較為溫和。從區域來看,亞太地區憑藉中國鐵塔204萬個基地台的資產組合和印度161億美元的區域互聯互通計劃,正引領成長。同時,北美和歐洲則在區域規劃的阻力下,專注於最佳化現有資產。交易趨勢凸顯了該產業的成熟度。通訊業者正在出售其鐵塔資產組合,並將所得資金再投資於頻段和核心網路升級,凸顯了其向輕資產營運模式的策略轉變。

全球電信鐵塔市場趨勢及洞察

5G網路的部署正在推動基礎設施整合。

為了實現5G的低延遲目標,通訊業者需要將基地台密度提高到4G的三到五倍,尤其是在高頻寬的毫米波頻譜。光是在拉丁美洲,預計到2030年5G連線用戶將達到4.25億,因此,除了傳統的宏基地台外,部署更多的小型基地台至關重要。監管機構正在積極應對這項需求。加拿大廣播通訊委員會(CRTC)簡化了安裝法規,允許通訊業者在現有設施中添加5G無線電設備,而無需冗長的許可程序。這些政策轉變正在縮短引進週期,並穩定增加主要都會區對新建和升級基地台的需求。

行動數據使用量的增加給網路容量帶來了壓力。

2024年,影片串流、雲端遊戲的興起以及企業行動辦公室的普及,導致美國無線數據消耗量增加了36%。這通訊業者提高都市區的基地台安裝密度,並擴大農村地區的覆蓋範圍。隨著價格親民的智慧型手機日益普及,新興市場也出現了類似的成長。儘管載波聚合和大規模MIMO等技術可以更有效地利用頻寬,但實體基礎設施仍然是瓶頸。因此,電信鐵塔市場仍在緩慢但穩定地擴張,通訊業者正依靠鐵塔公司來加速解決容量短缺問題。

共用基地台的飽和限制了成熟市場的成長潛力。

在北美和西歐,每座鐵塔的利用率仍維持在約2.7個租戶,限制了租賃收入成長的潛力。結構上的限制使得升級到更重的5G設備變得複雜,需要耗費大量資金進行加固,進而對收入造成壓力。雖然新興市場的新租戶儲備依然強勁,但成熟地區的市場飽和正在阻礙成長,全球電信鐵塔市場正朝著更平衡的擴張模式轉變。

細分市場分析

2025年,非再生能源來源仍將主導電信鐵塔市場,佔市場佔有率的72.88%,主要促進因素是大型基地台站的電網供電和柴油發電機。然而,隨著通訊業者轉向太陽能-電池混合系統,大幅降低偏遠地區的營運成本,預計可再生能源將以5.22%的複合年成長率實現最高成長。在電力供應不穩定且柴油燃料物流成本高的地區,可再生能源的採用尤其顯著。德國電信(Telefónica Germany)的能源自給自足型5G鐵塔證明了其在溫帶氣候下的可行性。混合系統還能減少碳排放,使基礎設施供應商能夠滿足日益嚴格的ESG(環境、社會和治理)要求,並吸引綠色金融資本進入電信鐵塔市場。

領先的鐵塔公司目前正將能源即服務 (EaaS) 合約打包出售,使行動通訊業者(MNO) 能夠將站點管理和電力管理外包。隨著智慧控制器和人工智慧驅動的電池分析技術最佳化能耗曲線,通訊鐵塔產業正從能源消費者轉變為本地能源生產商。這種轉變正在擴大利潤空間,實現收入來源多元化,並增強該行業在永續連接方面的作用。

2025年,格子形杆塔憑藉其組裝鋼結構,能夠以經濟的成本支撐重型多頻段設備,維持了55.62%的市佔率。它們仍然是亞太地區和非洲廣闊農村地區廣域覆蓋的基礎。同時,單柱塔在都市區以4.12%的複合年成長率呈現最高成長。其單柱結構減少了土地徵用負擔,避免了對景觀的影響,從而加快了審核流程。 2024年推出的碳纖維單柱塔,重量是鋼製塔的12倍,抗張強度也是鋼製塔的12倍,不僅降低了運輸和基礎建設成本,也延長了設備的使用壽命。

隱形塔和拉線塔完善了產品線。隱形塔符合歷史街區的規劃法規,而拉線塔則適用於擁有足夠土地的高層建築專案。這種多樣化的設計方案使通訊塔市場能夠在不影響經濟效益的前提下,實現都市區密度提升和區域擴張的目標。

區域分析

亞太地區持續引領全球成長,這得益於中國204萬個基地台的龐大規模以及印度雄心勃勃的5G目標——到2030年新增數十萬用戶。政府政策也提供了有力支持,例如在頻率競標中優先考慮網路覆蓋,並透過地方補貼縮小商業可行性差距。在日本和韓國,將小型基地台疊加在宏網路上的超高密度架構日益成熟;而在東南亞,塔台共用模式正被積極探索,以加速部署並降低成本。這些趨勢鞏固了亞太地區作為通訊塔市場規模最大、成長最快的地區的地位。

北美地區基礎設施成熟,技術先進。廣泛的資源共享限制了新建設,而5G升級和邊緣資料中心計畫則支撐了租賃需求。諸如「農村5G基金」等聯邦計畫正在應對人口稀少地區的經濟挑戰,並促進服務不足社區的逐步發展。地方政府層級存在監管阻力,分區規劃的惰性和景觀方面的反對意見可能會延緩計畫進度,但聯邦政府的優先發展正在縮小地方政府否決的空間。

歐洲的兩極化趨勢十分明顯。西歐市場面臨飽和和嚴格的環境法規,迫使鐵塔公司在可再生能源基地台和符合環保法規的隱藏式設計方面進行創新。相較之下,東歐和巴爾幹半島的5G部署仍處於早期階段。頻率競標和歐盟互聯互通基金正在支持待開發區項目,推動全部區域的發展勢頭。同時,中東地區的整合也穩步推進,鐵塔公司佔據了超過44%的市場佔有率,這得益於STC的TAWAL和Zain的TASC等平台的支援。拉丁美洲受惠於美洲移動在巴西77億美元的投資以及不斷擴大的5G頻率競標。另一方面,非洲的長期潛力取決於政府的數位化計劃,這些計劃應結合衛星回程傳輸、農村補貼和普遍服務義務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G網路部署

- 行動資料通訊和智慧型手機使用量的增加

- 遍遠地區的通訊連接項目

- 將行動網路營運商的鐵塔資產貨幣化

- 對邊緣資料中心的託管需求

- 混合可再生能源系統的引入

- 市場限制因素

- 塔式共用飽和度

- 環境和分區法規

- 高強度鋼和複合材料的供應限制

- 低地球軌道衛星局部區域覆蓋的替代方案

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按燃料類型

- 可再生能源

- 不可可再生

- 塔式

- 格子形杆塔

- 分支塔

- 單極塔

- 隱形塔

- 透過安裝

- 屋頂

- 地面以上

- 所有權

- 通訊業者

- 合資

- 私人

- MNO子公司

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞洲地區

- 中東

- 以色列

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- American Tower Corporation

- Cellnex Telecom SA

- China Tower Corporation Limited

- SBA Communications Corporation

- Indus Towers Limited

- Helios Towers PLC

- IHS Holding Limited

- Vantage Towers AG

- Deutsche Funkturm GmbH

- TAWAL Company Ltd.

- Telxius Telecom SA

- Telesites SAB de CV

- AT&T Inc.

- T-Mobile US, Inc.

- GTL Infrastructure Limited

- Orange SA

- Telenor ASA

- PT Dayamitra Telekomunikasi Tbk(Mitratel)

- Ooredoo QPSC

- Zong Pakistan(CMPak Limited)

第7章 市場機會與未來展望

The Telecom Towers Market size was valued at USD 29.29 billion in 2025 and estimated to grow from USD 30.07 billion in 2026 to reach USD 34.3 billion by 2031, at a CAGR of 2.67% during the forecast period (2026-2031).

This steady trajectory reflects how mobile network operators (MNOs) are shifting from rapid green-field rollouts toward infrastructure sharing and energy-efficient upgrades that protect margins in a capital-intensive environment. Continued 5G densification, government-backed rural coverage programs, and accelerating adoption of hybrid renewable power systems keep demand resilient, yet the overall pace remains measured as co-location ratios climb, and spectrum costs weigh on operator budgets. Regionally, Asia-Pacific leads growth thanks to China Tower's 2.04 million-site portfolio and India's USD 16.1 billion rural connectivity plan, while North America and Europe focus on optimizing existing assets amid zoning headwinds. Transaction activity highlights the sector's maturation: operators are monetizing tower portfolios and redeploying proceeds into spectrum and core-network upgrades, underscoring a strategic pivot toward asset-light operating models.

Global Telecom Towers Market Trends and Insights

5G Network Rollouts Drive Infrastructure Densification

Operators must increase site density by three to five times compared with 4G to deliver 5G's low-latency targets, especially in high-band millimetre-wave spectrum. Latin America alone is expected to reach 425 million 5G connections by 2030, necessitating both traditional macro towers and growing layers of small cells. Regulatory bodies are responding: the Canadian Radio-television and Telecommunications Commission (CRTC) streamlined attachment rules so carriers can add 5G radios on existing structures without lengthy permissions. These policy shifts shorten deployment cycles and support consistent upward demand for new and upgraded tower sites across major urban corridors.

Rising Mobile Data Usage Pressures Network Capacity

U.S. wireless data consumption climbed 36% during 2024 as video streaming, cloud gaming, and enterprise mobility took hold, forcing carriers such as Crown Castle's tenants to densify urban footprints and expand rural coverage. Emerging markets mirror this surge as affordable smartphones proliferate. Techniques like carrier aggregation and massive-MIMO can stretch the spectrum, yet physical infrastructure remains the gating factor. As a result, the telecom towers market continues to exhibit incremental but durable expansion, with operators relying on tower companies to accelerate capacity meets.

Tower-Sharing Saturation Limits Mature-Market Upside

Co-location ratios in North America and Western Europe hover around 2.7 tenants per tower, leaving limited headroom for incremental leasing revenue. Structural limits complicate upgrades for heavier 5G equipment, prompting costly reinforcements that erode returns. While new tenancy pipelines remain healthy in emerging economies, saturation tempers growth in established regions, nudging the global telecom towers market toward a more balanced expansion profile.

Other drivers and restraints analyzed in the detailed report include:

- Rural Connectivity Programs Unlock New Market Opportunities

- MNO Tower-Asset Monetization Accelerates Industry Restructuring

- Environmental and Zoning Restrictions Complicate Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-renewable sources dominated with 72.88% telecom towers market share in 2025, anchored by grid electricity and diesel generators for macro-cell sites. However, renewables deliver the fastest growth at a 5.22% CAGR as operators pivot to solar-battery hybrids that slash operating expense in remote areas. Renewable adoption is most pronounced in regions with erratic grid supply and high diesel logistics costs; Telefonica Germany's energy self-sufficient 5G tower demonstrates viability in temperate climates. Hybrid systems also curb carbon output, aligning infrastructure providers with tightening ESG mandates and drawing green-finance capital toward the telecom towers market.

Progressive tower companies now bundle energy-as-a-service contracts, allowing MNOs to outsource both site and power management. As smart controllers and AI-driven battery analytics optimize consumption curves, the telecom towers industry is transitioning from energy consumer to localized producer. That evolution widens margin opportunity, diversifies revenue, and reinforces the sector's role in sustainable connectivity.

Lattice towers retained a 55.62% share in 2025 because their triangulated-steel design supports heavy multi-band payloads at economical cost. They remain the backbone for wide-area coverage across rural expanses of Asia-Pacific and Africa. Monopoles, though, exhibit the highest growth at 4.12% CAGR in urban corridors. Their single-column form factors reduce right-of-way and skirt aesthetic objections, enabling faster permitting cycles. Carbon-fiber monopoles introduced in 2024 weigh one-twelfth of steel yet deliver twelve times the tensile strength, curbing transport and foundation expense while extending asset life.

Stealth and guyed variants round out the portfolio: stealth solutions satisfy zoning mandates in heritage districts, while guyed towers address ultra-tall applications where land is abundant. Collectively, diversified designs help the telecom towers market serve both densification and rural outreach targets without compromising economics.

The Telecom Towers Market Report is Segmented by Fuel Type (Renewable, Non-Renewable), Type of Tower (Lattice Tower, Guyed Tower, Monopole Tower, Stealth Tower), Installation (Rooftop, Ground-Based), Ownership (Operator-Owned, Joint Venture, Private-Owned, MNO Captive), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the engine of global growth, backed by China's 2.04 million-site footprint and India's aggressive 5G targets that will add hundreds of thousands of new tenancies by 2030. Government policy is supportive: spectrum auctions prioritize coverage, and rural subsidies narrow viability gaps. Japan and South Korea refine ultra-dense architectures that layer small cells onto macro grids, while Southeast Asian markets pursue tower-sharing frameworks to accelerate rollout and contain costs. These dynamics solidify Asia-Pacific's status as both the largest and fastest-growing slice of the telecom towers market.

North America presents a mature but technologically advanced landscape. Extensive co-location has tempered new-build volumes, yet 5G upgrades and edge-data-center initiatives sustain leasing demand. Federal programs such as the Rural 5G Fund bridge the economics of sparsely populated territories, steering incremental growth toward underserved communities. Regulatory headwinds arise at the municipal level, where zoning inertia and aesthetic opposition can extend project timelines, but federal pre-emption measures are narrowing the window for local vetoes.

Europe shows a two-speed pattern. Western markets face saturation and stringent environmental scrutiny, prompting tower companies to innovate with renewable-powered sites and stealth designs that satisfy eco-centric regulations. Eastern Europe and the Balkans, in contrast, are earlier in the 5G curve; spectrum auctions and EU connectivity funds support green-field construction that lifts overall regional momentum. Meanwhile, the Middle East advances consolidation, with TowerCo share surpassing 44% on the back of STC's TAWAL and Zain's TASC platforms. Latin America benefits from America Movil's USD 7.7 billion Brazil commitment and expanding 5G auctions, while Africa's long-term potential rests on government digitization plans that combine satellite backhaul, rural subsidies, and universal-service mandates.

- American Tower Corporation

- Cellnex Telecom S.A.

- China Tower Corporation Limited

- SBA Communications Corporation

- Indus Towers Limited

- Helios Towers PLC

- IHS Holding Limited

- Vantage Towers AG

- Deutsche Funkturm GmbH

- TAWAL Company Ltd.

- Telxius Telecom S.A.

- Telesites S.A.B. de C.V.

- AT&T Inc.

- T-Mobile US, Inc.

- GTL Infrastructure Limited

- Orange S.A.

- Telenor ASA

- PT Dayamitra Telekomunikasi Tbk (Mitratel)

- Ooredoo Q.P.S.C.

- Zong Pakistan (CMPak Limited)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G network roll-outs

- 4.2.2 Rising mobile data and smartphone usage

- 4.2.3 Rural connectivity programmes

- 4.2.4 MNO tower-asset monetisation

- 4.2.5 Edge data-centre co-location demand

- 4.2.6 Hybrid renewable power systems adoption

- 4.3 Market Restraints

- 4.3.1 Tower-sharing saturation

- 4.3.2 Environmental and zoning restrictions

- 4.3.3 High-strength steel and composite supply constraints

- 4.3.4 LEO-satellite rural coverage substitution

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Fuel Type

- 5.1.1 Renewable

- 5.1.2 Non-Renewable

- 5.2 By Type of Tower

- 5.2.1 Lattice Tower

- 5.2.2 Guyed Tower

- 5.2.3 Monopole Tower

- 5.2.4 Stealth Tower

- 5.3 By Installation

- 5.3.1 Rooftop

- 5.3.2 Ground-based

- 5.4 By Ownership

- 5.4.1 Operator-owned

- 5.4.2 Joint Venture

- 5.4.3 Private-owned

- 5.4.4 MNO Captive

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 American Tower Corporation

- 6.4.2 Cellnex Telecom S.A.

- 6.4.3 China Tower Corporation Limited

- 6.4.4 SBA Communications Corporation

- 6.4.5 Indus Towers Limited

- 6.4.6 Helios Towers PLC

- 6.4.7 IHS Holding Limited

- 6.4.8 Vantage Towers AG

- 6.4.9 Deutsche Funkturm GmbH

- 6.4.10 TAWAL Company Ltd.

- 6.4.11 Telxius Telecom S.A.

- 6.4.12 Telesites S.A.B. de C.V.

- 6.4.13 AT&T Inc.

- 6.4.14 T-Mobile US, Inc.

- 6.4.15 GTL Infrastructure Limited

- 6.4.16 Orange S.A.

- 6.4.17 Telenor ASA

- 6.4.18 PT Dayamitra Telekomunikasi Tbk (Mitratel)

- 6.4.19 Ooredoo Q.P.S.C.

- 6.4.20 Zong Pakistan (CMPak Limited)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

通訊塔市場規模、佔有率、趨勢和預測:按塔型、燃料類型、安裝方式、所有權方式和地區分類,2026-2034 年

通訊塔市場規模、佔有率、趨勢和預測:按塔型、燃料類型、安裝方式、所有權方式和地區分類,2026-2034 年 隱蔽通訊塔市場規模、佔有率和成長分析:按偽裝設計/類型、塔架結構、頻率/頻段相容性、安裝位置和地區分類-2026-2033年產業預測

隱蔽通訊塔市場規模、佔有率和成長分析:按偽裝設計/類型、塔架結構、頻率/頻段相容性、安裝位置和地區分類-2026-2033年產業預測 行動電話基地台管理市場:依接取技術、塔型、安裝方式、服務類型、高度等級、組件類型及最終用戶產業分類-2026-2032年全球市場預測

行動電話基地台管理市場:依接取技術、塔型、安裝方式、服務類型、高度等級、組件類型及最終用戶產業分類-2026-2032年全球市場預測 2026年全球數位雙胞胎市場報告

2026年全球數位雙胞胎市場報告 2026-2030年全球電信塔市場2026年全球通訊塔市場報告

2026-2030年全球電信塔市場2026年全球通訊塔市場報告 美國電信鐵塔:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲電信塔及相關產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

美國電信鐵塔:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非洲電信塔及相關產業:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 塔架管理軟體市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署類型、塔架類型、功能、最終用戶、地區和競爭格局分類,2021-2031 年)電信塔供電系統市場-全球產業規模、佔有率、趨勢、機會與預測:電源、電網、組件、區域和競爭格局,2021-2031年

塔架管理軟體市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署類型、塔架類型、功能、最終用戶、地區和競爭格局分類,2021-2031 年)電信塔供電系統市場-全球產業規模、佔有率、趨勢、機會與預測:電源、電網、組件、區域和競爭格局,2021-2031年